Minnesota Jury Instruction - 10.10.3 Employee vs. Self-Employed Independent Contractor

Description

How to fill out Jury Instruction - 10.10.3 Employee Vs. Self-Employed Independent Contractor?

If you need to full, acquire, or produce lawful document themes, use US Legal Forms, the biggest selection of lawful kinds, which can be found online. Make use of the site`s basic and convenient lookup to find the documents you require. Numerous themes for organization and specific functions are categorized by classes and claims, or search phrases. Use US Legal Forms to find the Minnesota Jury Instruction - 10.10.3 Employee vs. Self-Employed Independent Contractor in just a handful of mouse clicks.

When you are presently a US Legal Forms consumer, log in to the profile and then click the Down load key to get the Minnesota Jury Instruction - 10.10.3 Employee vs. Self-Employed Independent Contractor. You may also entry kinds you in the past downloaded inside the My Forms tab of the profile.

Should you use US Legal Forms for the first time, follow the instructions under:

- Step 1. Be sure you have chosen the form for that proper metropolis/region.

- Step 2. Utilize the Review solution to examine the form`s information. Don`t neglect to read the explanation.

- Step 3. When you are not satisfied with all the form, utilize the Lookup field towards the top of the monitor to get other variations of the lawful form web template.

- Step 4. Upon having found the form you require, click the Acquire now key. Opt for the prices strategy you favor and put your qualifications to sign up for an profile.

- Step 5. Process the financial transaction. You can utilize your charge card or PayPal profile to accomplish the financial transaction.

- Step 6. Select the file format of the lawful form and acquire it on your own system.

- Step 7. Comprehensive, revise and produce or sign the Minnesota Jury Instruction - 10.10.3 Employee vs. Self-Employed Independent Contractor.

Every lawful document web template you buy is your own property permanently. You have acces to each form you downloaded in your acccount. Click the My Forms area and choose a form to produce or acquire once again.

Compete and acquire, and produce the Minnesota Jury Instruction - 10.10.3 Employee vs. Self-Employed Independent Contractor with US Legal Forms. There are many expert and state-certain kinds you can use for your organization or specific requires.

Form popularity

FAQ

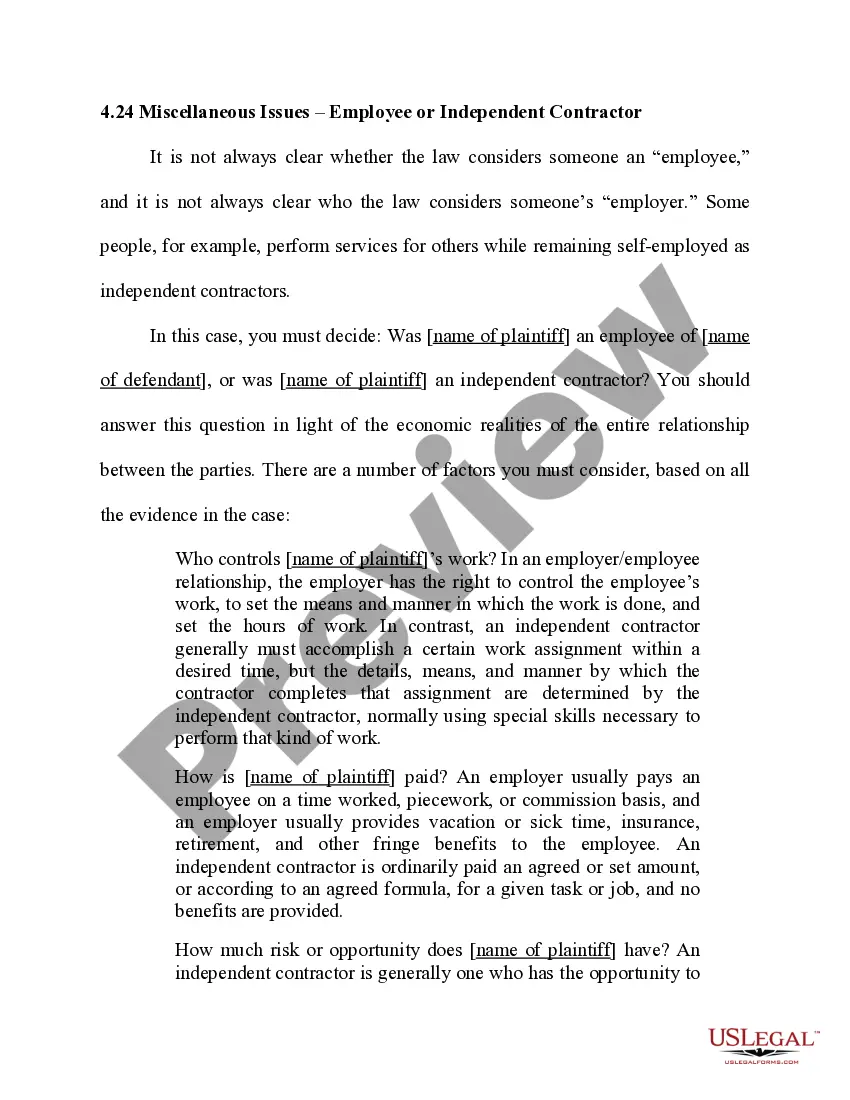

The law further states that independent contractor status is evidenced if the worker: (1) has a substantial investment in the business other than personal services, (2) purports to be in business for himself or herself, (3) receives compensation by project rather than by time, (4) has control over the time and place ...

Pay basis: If you pay a worker on an hourly, weekly, or monthly basis, the IRS will consider it a sign the worker is your employee. An independent is generally paid by the job, project, assignment, etc., or receives a commission or similar fee.

Who Is An Independent Contractor? Individuals who perform regular work for a company in the course of that company's business are employees. An independent contractor, on the other hand, is a worker who is not an employee and independently contracts with an individual or business to provide a good or perform a service.

Even though their pay can vary depending on the terms of their contracts, employees normally do not have the chance to profit from their work. Independent contactors may have the chance to profit or incur losses from their work. They can set their own prices and normally incur expenses to complete the work.

For the employee, the company withholds income tax, Social Security, and Medicare from wages paid. For the independent contractor, the company does not withhold taxes. Employment and labor laws also do not apply to independent contractors.

If the worker is an employee, you must generally withhold and deposit income taxes, Social Security Taxes, and Medicare taxes. In addition to these taxes, you must pay unemployment taxes and carry worker's compensation insurance. These requirements generally do not apply to independent contractors.

A worker is an independent contractor if you have the right to control or direct only the result of the work and not how to work is performed. Independent contractors pay self-employment tax on their earnings.

The total Minnesota self employment tax is 15.3%, divided into a Social Security amount of 12.4% and a Medicare amount of 2.9%.