Minnesota Petty Cash Journal

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Petty Cash Journal?

Selecting the correct official document template can be a challenge.

Clearly, there is a multitude of templates accessible online, but how do you locate the official form you require.

Utilize the US Legal Forms website.

If you are a new user of US Legal Forms, here are some simple steps you can follow: First, ensure you have selected the correct form for your city/county. You can view the form using the Review button and read the form details to confirm it is the right one for you.

- The service offers thousands of templates, including the Minnesota Petty Cash Journal, suitable for both business and personal needs.

- All forms are reviewed by experts and comply with state and federal regulations.

- If you are already registered, Log In to your account and click the Download button to retrieve the Minnesota Petty Cash Journal.

- Use your account to browse through the official forms you have previously ordered.

- Visit the My documents section of your account to download another version of the document you need.

Form popularity

FAQ

If there's a shortage or overage, a journal line entry is recorded to an over/short account. If the petty cash fund is over, a credit is entered to represent a gain. If the petty cash fund is short, a debit is entered to represent a loss. The over or short account is used to force-balance the fund upon reconciliation.

Petty cash provides convenience for small transactions for which issuing a check or a corporate credit card is unreasonable or unacceptable. The small amount of cash that a company considers petty will vary, with many companies keeping between $100 and $500 as a petty cash fund.

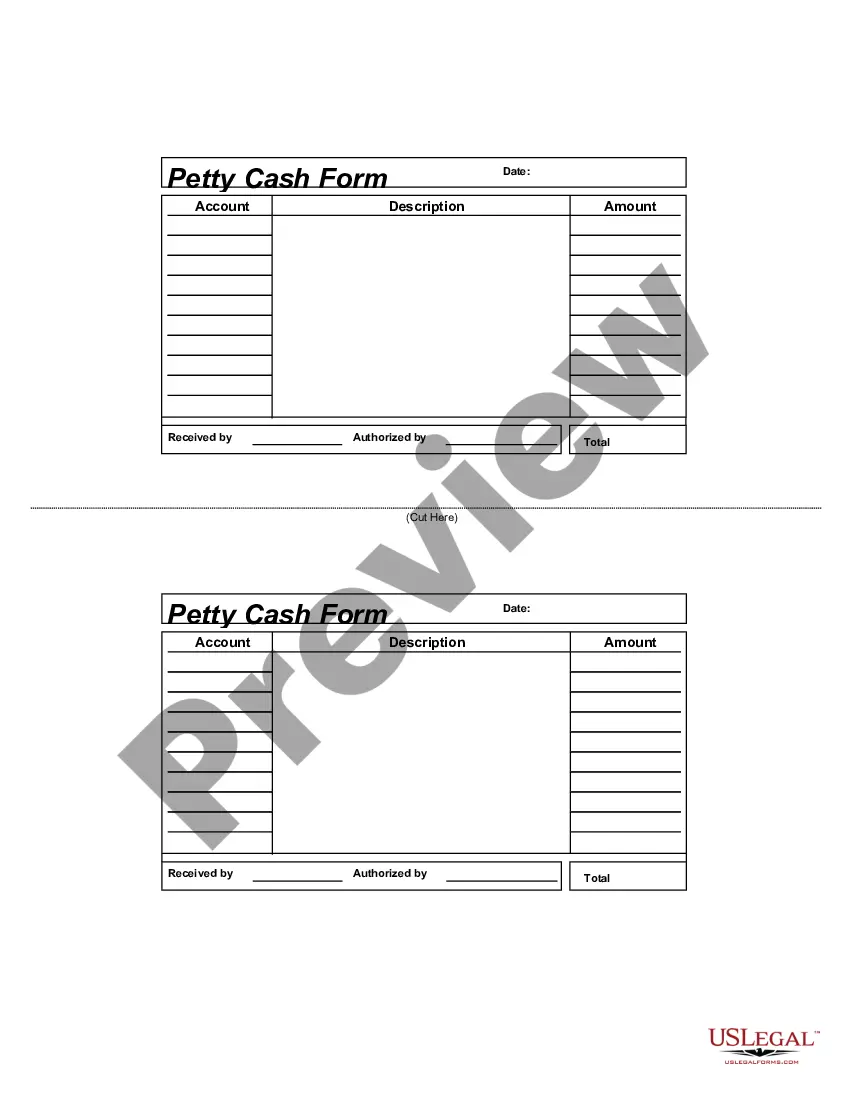

Petty cash is a small amount of cash that is kept on the company premises to pay for minor cash needs. Examples of these payments are office supplies, cards, flowers, and so forth. Petty cash is stored in a petty cash drawer or box near where it is most needed.

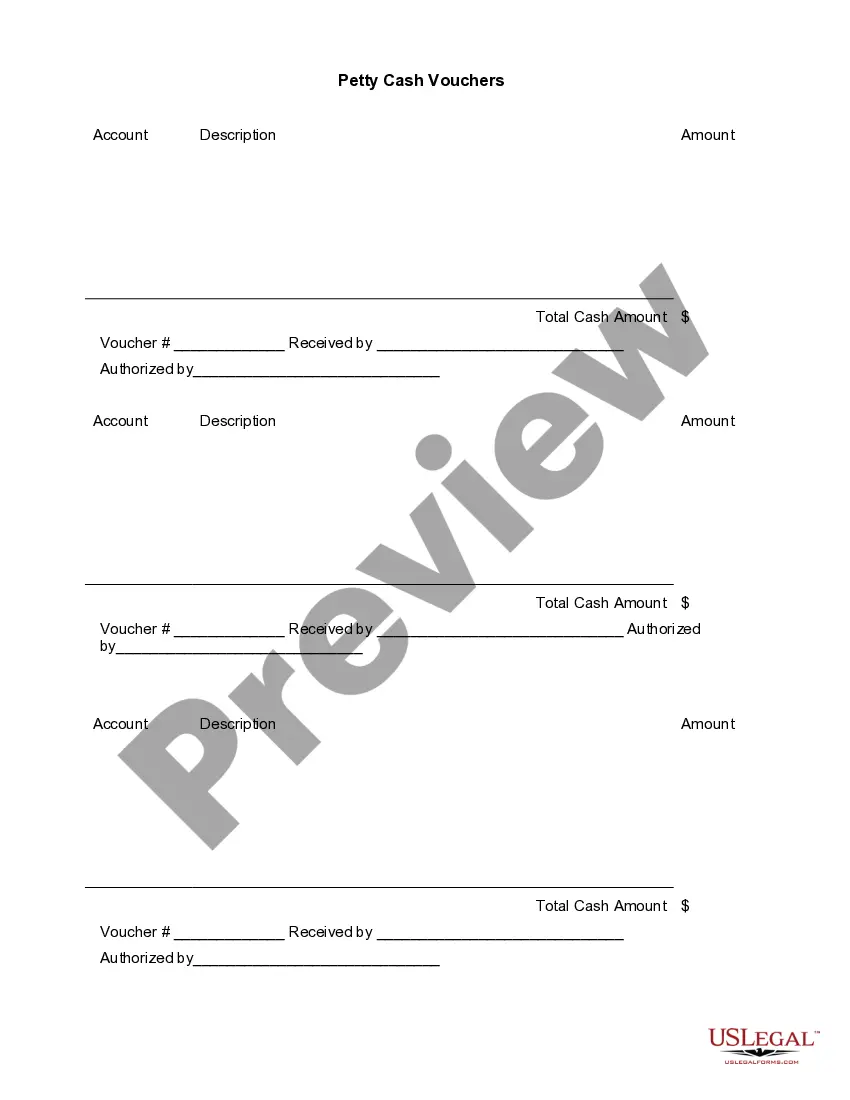

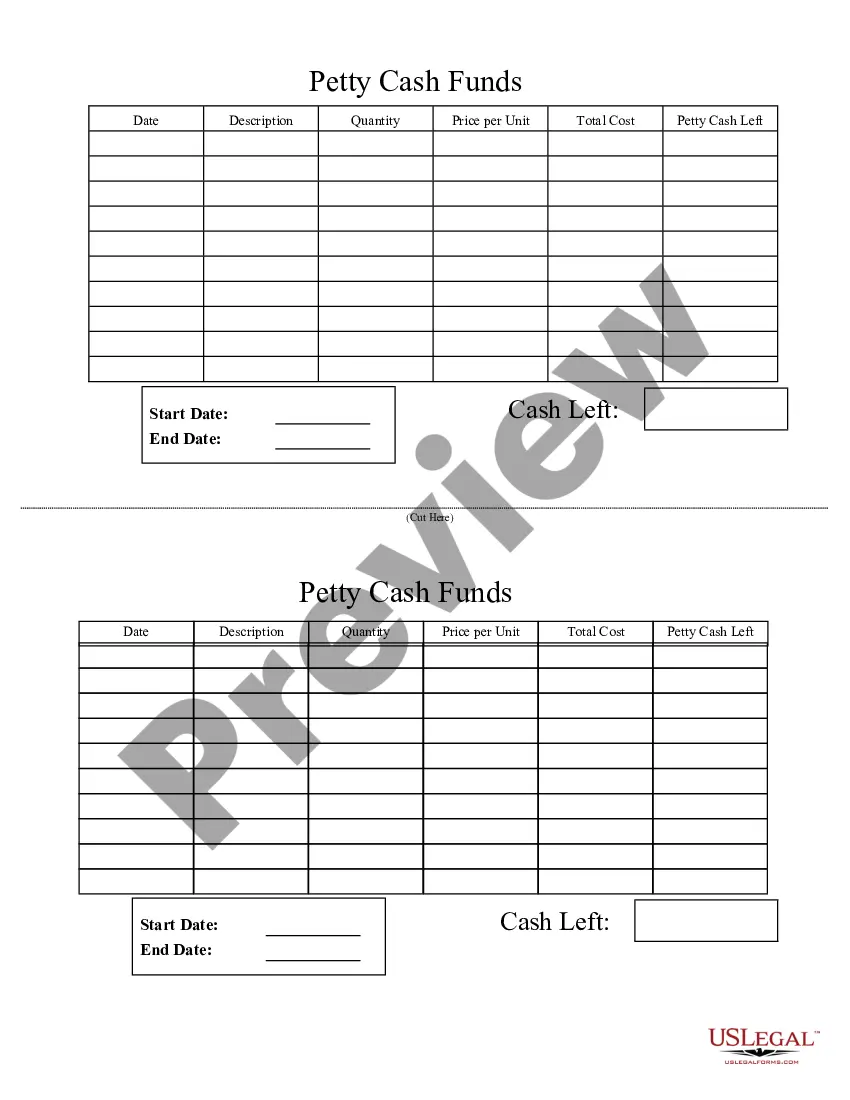

The procedure for petty cash funding is outlined below:Complete reconciliation form. Complete a petty cash reconciliation form, in which the petty cash custodian lists the remaining cash on hand, vouchers issued, and any overage or underage.Obtain cash.Add cash to petty cash fund.Record vouchers in general ledger.

Usually one individual, called the petty cash custodian or cashier, is responsible for the control of the petty cash fund and documenting the disbursements made from the fund. By assigning the responsibility for the fund to one individual, the company has internal control over the cash in the fund.

A simple petty cash book is just like the main cash book. Cash received by the petty cashier is recorded on the debit side, and all payments for petty expenses are recorded on the credit side in one column.

The petty cash journal entry is a debit to the petty cash account and a credit to the cash account. The petty cash custodian refills the petty cash drawer or box, which should now contain the original amount of cash that was designated for the fund.

Petty cash funds may not be deposited into personal bank accounts or commingled with other funds.Departments may not establish bank accounts for petty cash funds.Purchases of goods and services for more than $100 should not be made with petty cash.Petty cash funds may not be expended for:

Petty cash appears within the current assets section of the balance sheet. This is because line items in the balance sheet are sorted in their order of liquidity. Since petty cash is highly liquid, it appears near the top of the balance sheet.

Even though the expenses running through your petty cash funds are small, they will still need to be managed properly. Tracking all of your petty cash expenses as part of your bookkeeping system ensures that all tax-deductible expenses are captured.