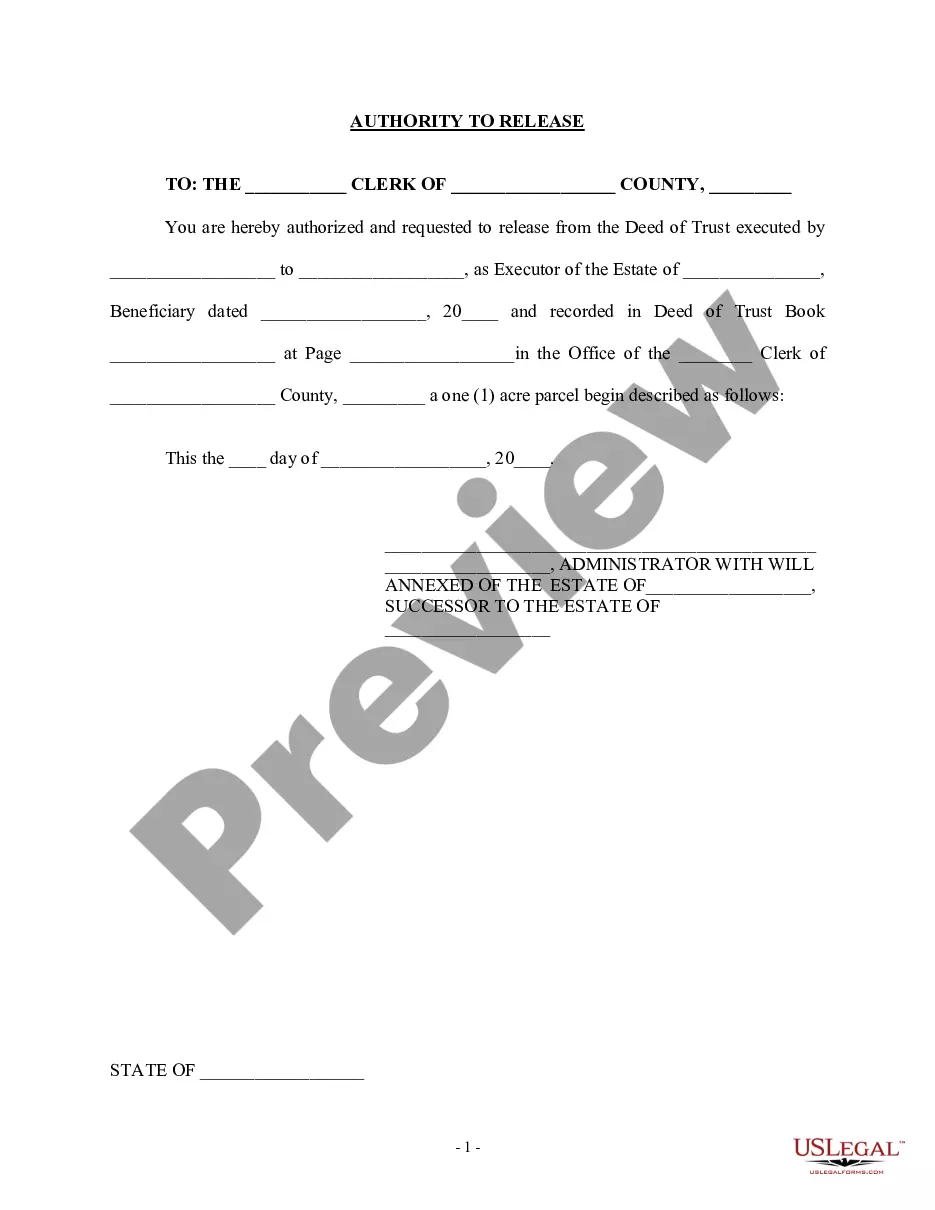

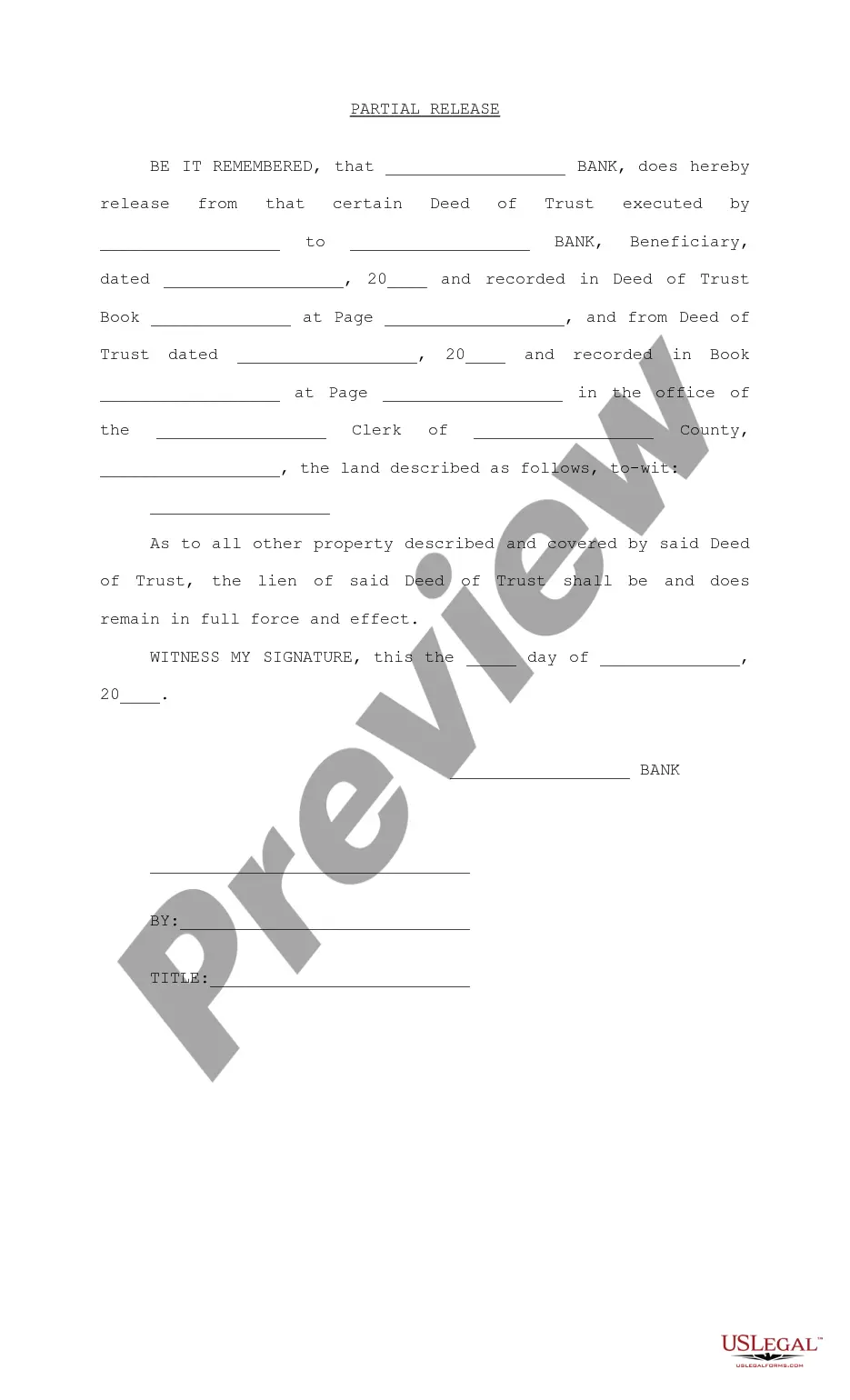

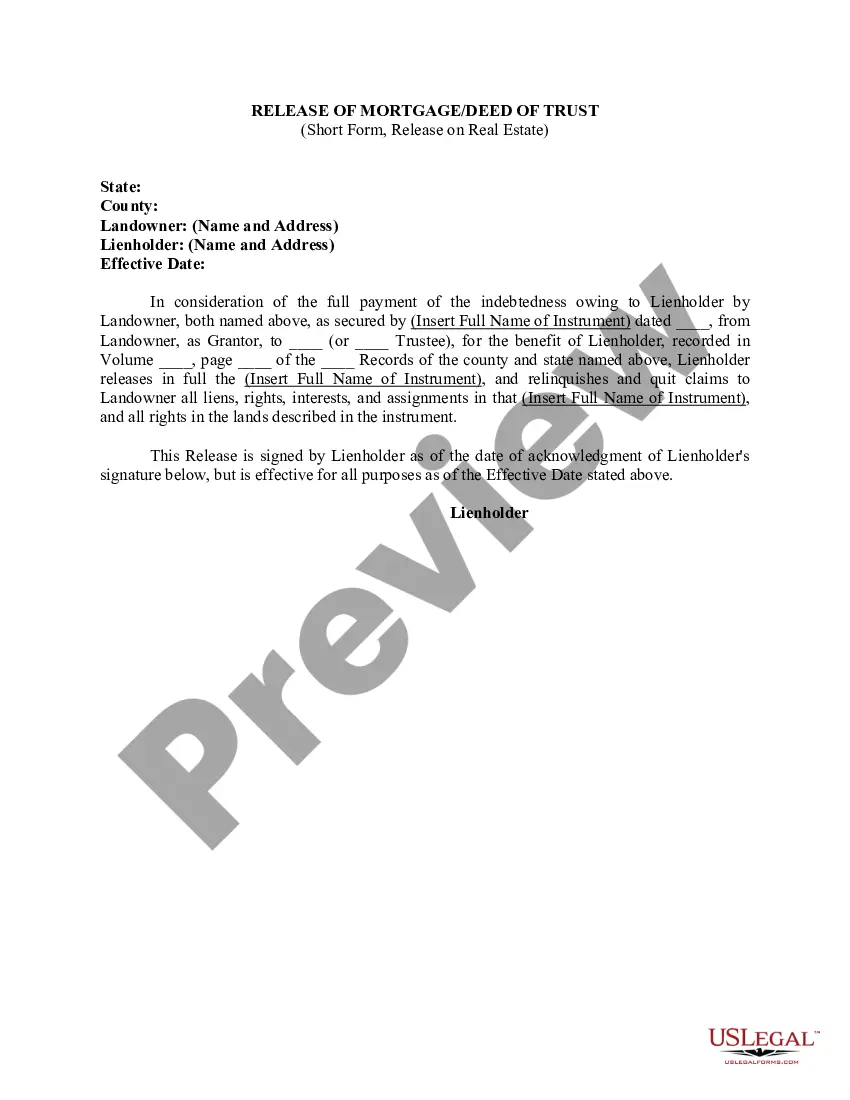

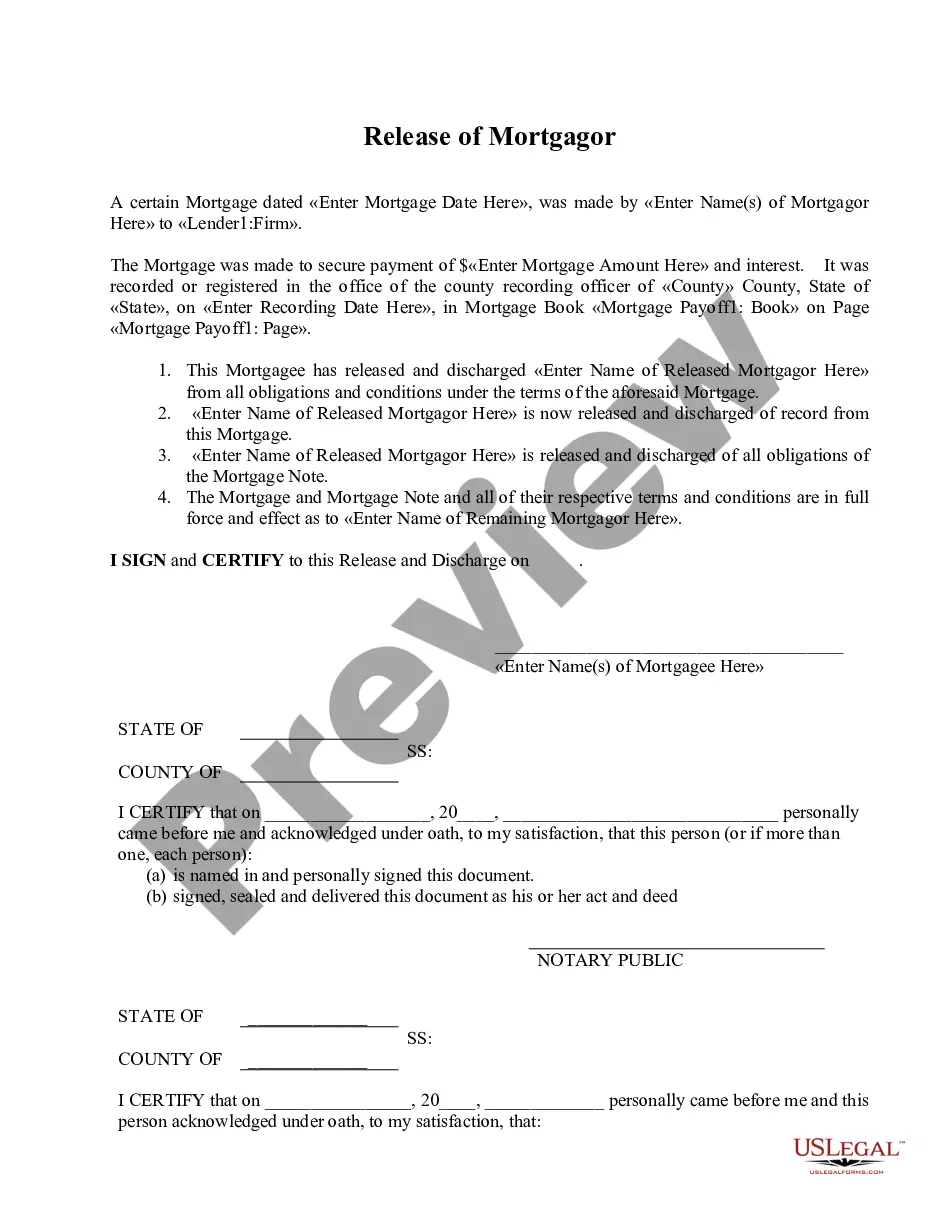

This form authorizes the chancery clerk or the recorder of deeds to release from the deed of trust or mortgage certain property described in the document.

Minnesota Deed of Trust - Release

State:

Multi-State

Control #:

US-00489

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Deed Of Trust - Release?

Have you been in a situation where you require documents for either business or personal reasons every day.

There are numerous legal document templates accessible online, but finding reliable versions isn't easy.

US Legal Forms offers a vast collection of form templates, including the Minnesota Deed of Trust - Release, designed to comply with state and federal regulations.

Select the pricing plan you want, provide the required information to create your account, and complete the order using your PayPal or Visa or Mastercard.

Choose a convenient paper format and download your copy. You can find all the document templates you have purchased in the My documents menu. You can obtain another copy of the Minnesota Deed of Trust - Release at any time if needed. Just click on the required form to download or print the document template. Utilize US Legal Forms, the most comprehensive selection of legal forms, to save time and avoid mistakes. The service provides professionally crafted legal document templates suitable for a variety of purposes. Create an account on US Legal Forms and begin simplifying your life.

- If you are already familiar with the US Legal Forms website and possess an account, simply Log In.

- Then, you can download the Minnesota Deed of Trust - Release template.

- If you do not have an account and wish to start using US Legal Forms, follow these instructions.

- Find the form you need and ensure it is for the correct region/area.

- Utilize the Review button to examine the form.

- Read the information to confirm you have selected the correct form.

- If the form isn't what you are looking for, use the Search field to find the form that meets your needs and criteria.

- Once you locate the appropriate form, click Purchase now.

Form popularity

FAQ

If your circumstances change any you are no longer able to make your payments, your Trust Deed may fail and you will still be liable for your debts or even forced into bankruptcy.

A Minnesota deed of trust is used to secure real estate financing by placing the borrower's property in trust until the lender has been paid back.

If you lose or misplace the original deed, you may obtain a certified copy from the County Recorder or Registrar of Titles in the county where the property is located. A certified copy of the deed may be recorded in any county with the same force and effect that the original deed would have if it were so recorded.

A deed of release is a legal document that removes a previous claim on an asset. It provides documentation of release from a binding agreement. A deed of release might be included when a lender transfers the title of real estate to the homeowner upon satisfaction of the mortgage.

Like a mortgage, a trust deed makes a piece of real property security (collateral) for a loan. If the loan is not repaid on time, the lender can foreclose on and sell the property and use the proceeds to pay off the loan. Note: A trust deed is not used to transfer property to a living trust (use a Grant Deed for that).

What Is A Deed Of Trust? A deed of trust is an agreement between a home buyer and a lender at the closing of a property. The agreement states that the home buyer will repay the home loan and the mortgage lender will hold the property's legal title until the loan is paid in full.

Minnesota Transfer on Death Deeds You must sign the deed and get your signature notarized, and then record (file) the deed with the county recorder's office or county registrar of titles (see "Recording Your Deed" below to determine which) before your death. ... The beneficiary's rights. ... The spouse's rights.

Through a deed of release of mortgage, also called a release of deed of trust, the lender agrees to remove the deed of trust, which is the document containing all of the mortgage's terms and conditions that is filed at the beginning of the mortgage process.