Maryland Owner Financing Contract for Moblie Home

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Owner Financing Contract For Moblie Home?

Selecting the appropriate legal document template can be a challenge. Clearly, there are numerous templates accessible online, but how will you find the legal form that you require.

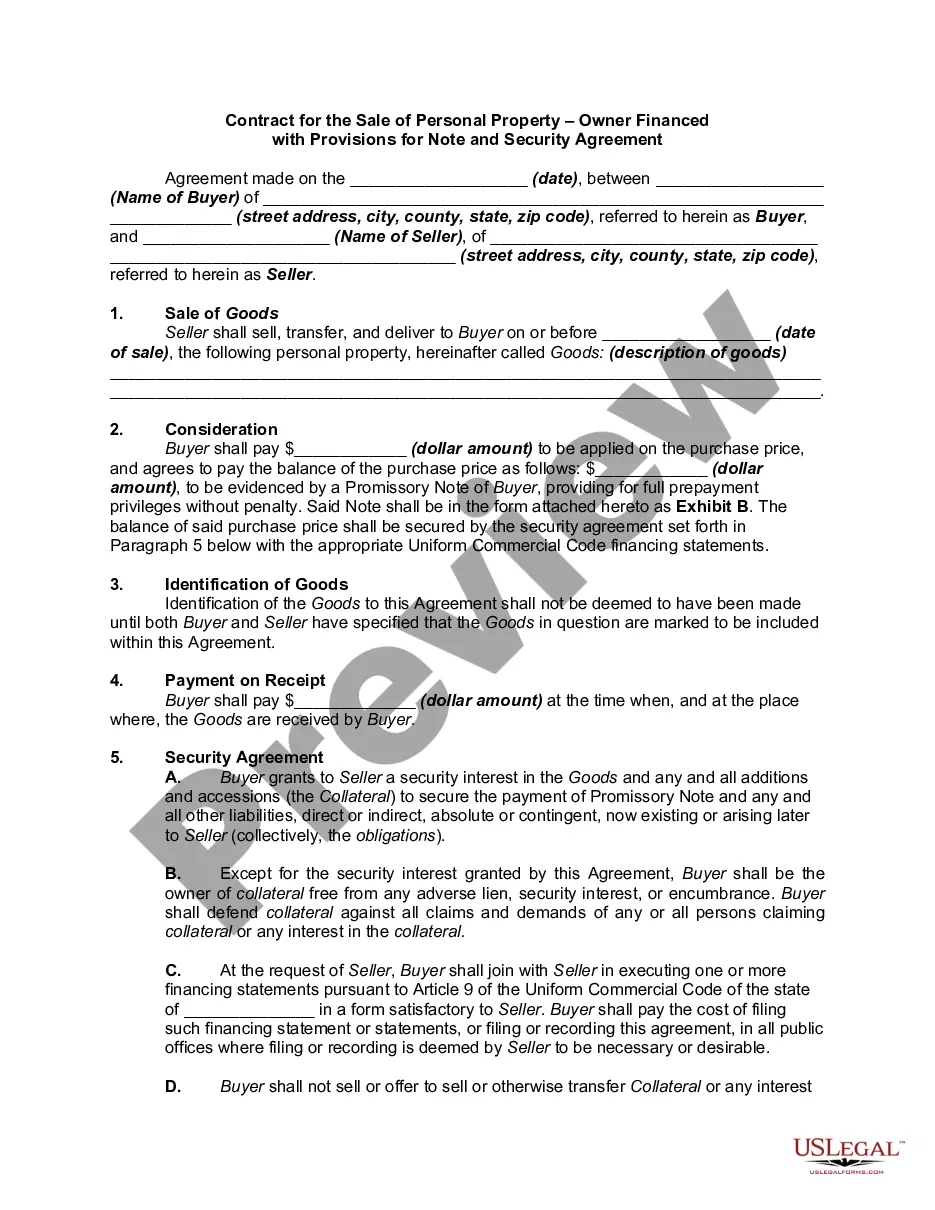

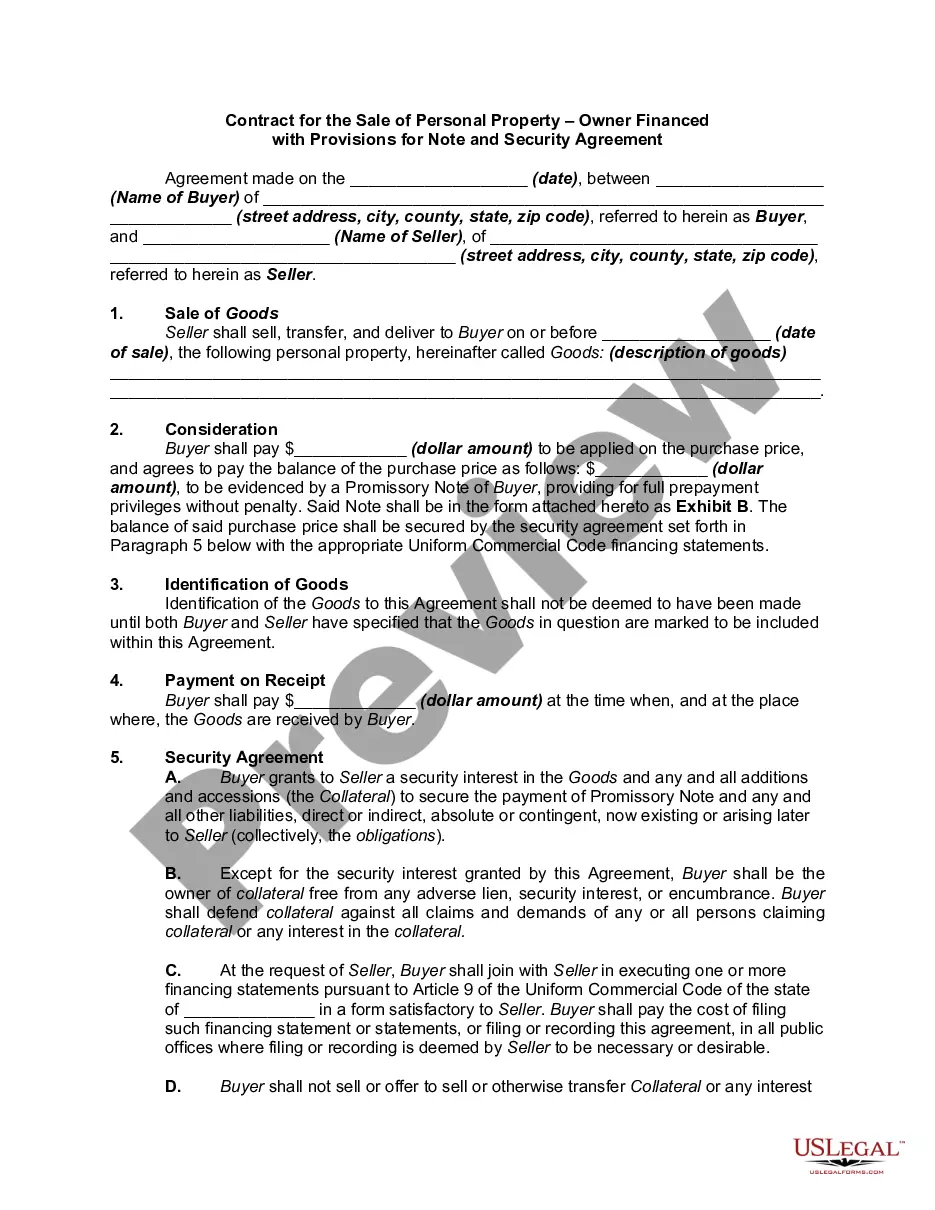

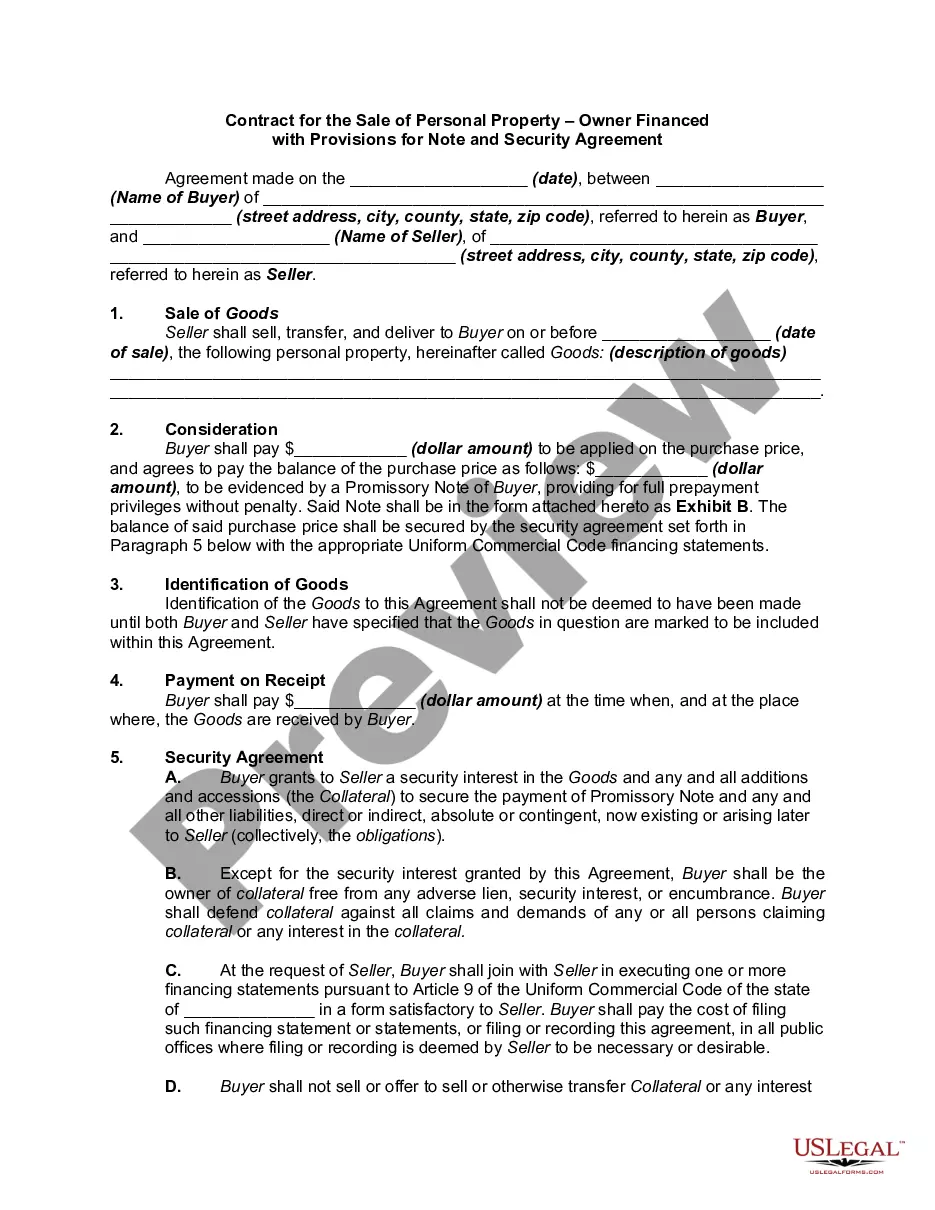

Utilize the US Legal Forms website. This service offers thousands of templates, such as the Maryland Owner Financing Agreement for Mobile Home, which you can use for both business and personal purposes. All of the documents are verified by professionals and comply with state and federal regulations.

If you are already registered, Log In to your account and click the Download button to locate the Maryland Owner Financing Agreement for Mobile Home. Use your account to search through the legal forms you have previously acquired. Visit the My documents section of your account to obtain another copy of the document you require.

Select the file format and download the legal document template to your device. Complete, edit, print, and sign the acquired Maryland Owner Financing Agreement for Mobile Home. US Legal Forms is the largest repository of legal forms where you can find a variety of document templates. Take advantage of this service to obtain professionally crafted documents that comply with state requirements.

- First, ensure you have selected the correct form for your area/region.

- You can preview the form using the Preview button and read the form description to confirm it is suitable for you.

- If the form does not satisfy your needs, utilize the Search field to locate the appropriate form.

- Once you are certain that the form is suitable, select the Get now button to retrieve the form.

- Choose the pricing plan you prefer and input the required information.

- Create your account and complete your purchase using your PayPal account or credit/debit card.

Form popularity

FAQ

In Maryland, a mobile home can be considered real property if it is permanently affixed to a foundation and the land it occupies is owned by the homeowner. If the mobile home is not permanently affixed, it may be classified as personal property instead. Understanding how these classifications affect a Maryland Owner Financing Contract for Mobile Home is crucial for both buyers and sellers.

The minimum credit score to buy a mobile home varies by lender, but generally, a score of at least 580 is preferred. If you're considering a Maryland Owner Financing Contract for Mobile Home, some lenders may offer more flexible terms. Stronger credit can lead to better interest rates and terms for your financing. It's a good idea to check your credit score and improve it if needed before applying.

In owner financing, the seller typically holds the deed until the buyer fulfills the financing terms outlined in the contract. This means that the buyer can live in and use the mobile home, but does not have legal title. This arrangement is defined and protected within a Maryland Owner Financing Contract for Mobile Home, providing clarity for both parties.

If a buyer defaults on an owner financing agreement, the seller has the right to reclaim the mobile home based on the contract terms. The specifics of this process are typically detailed in the Maryland Owner Financing Contract for Mobile Home. It's vital for sellers to understand these conditions before entering into an owner financing deal.

In most cases of owner financing, the seller acts as the lender and retains the deed until all payments are made. This means that unlike traditional lenders, the seller keeps ownership of the property title. This arrangement is essential in the Maryland Owner Financing Contract for Mobile Home, allowing the seller to maintain control while the buyer occupies the home.

Example of owner financing The buyer and seller agree to a purchase price of $175,000. The seller requires a down payment of 15 percent $26,250. The seller agrees to finance the outstanding $148,750 at an 8 percent fixed interest rate over a 30-year amortization, with a balloon payment due after five years.

Despite the advantages of seller financing, it can be risky for owners. For one, if the buyer defaults on the loan, the seller might have to face foreclosure. Because mortgages often come with clauses that require payment by a certain time, missing that date could be catastrophic.

Risk of Unfavorable Loan Terms From the Seller Sellers who are extending their own financing (also called "taking back a mortgage") often charge a higher interest rate than institutional lenders, because of the increased level of risk that the buyer will default (fail to pay, or otherwise violate the mortgage terms).

Key Takeaways. Owner financing can be a good option for buyers who don't qualify for a traditional mortgage. For sellers, owner financing provides a faster way to close because buyers can skip the lengthy mortgage process.

Interest rates for owner financed homes are generally higher than what would be offered by a traditional lender. The seller takes a risk when they provide financing, and they may increase their interest rates to offset this risk. Average interest rates tend to range between 4-10%.