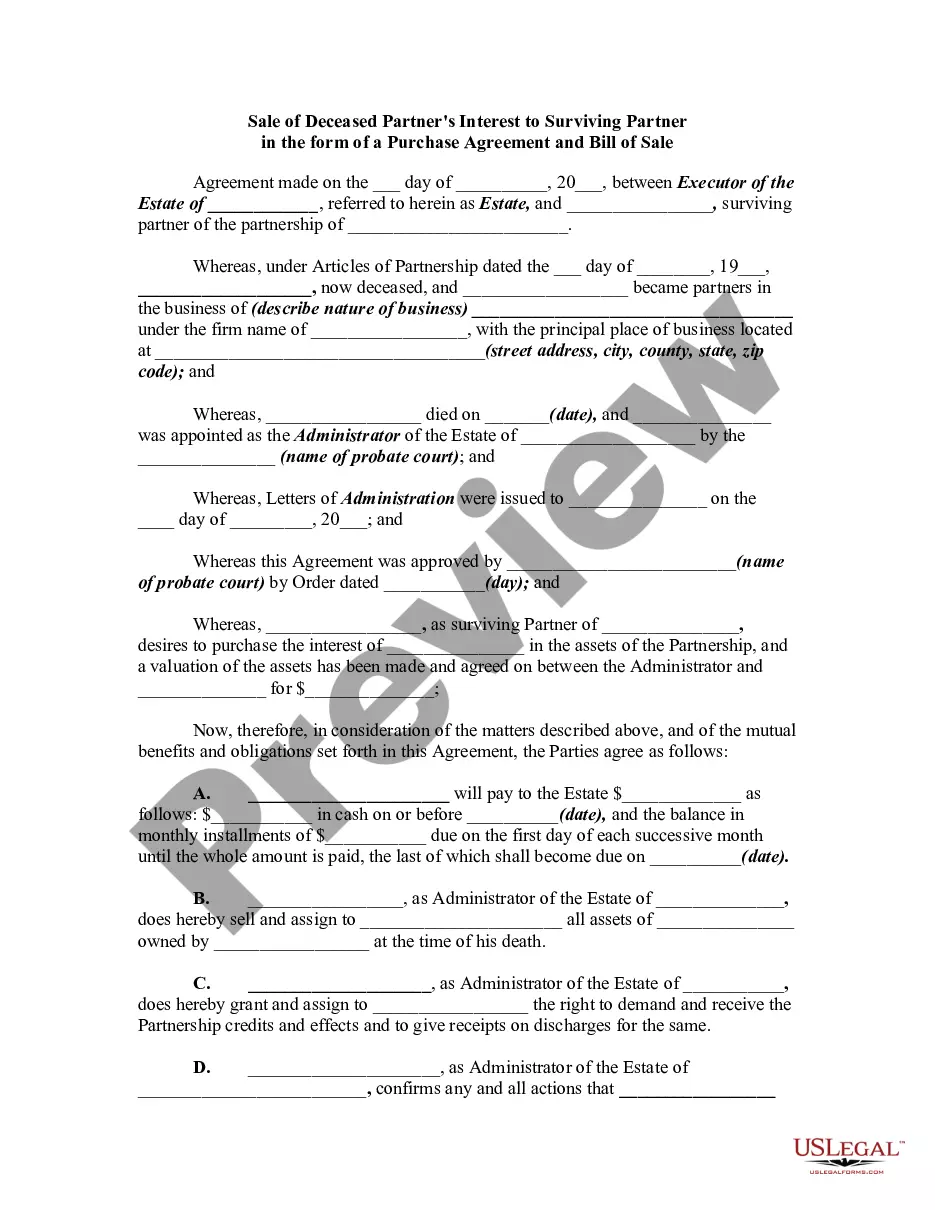

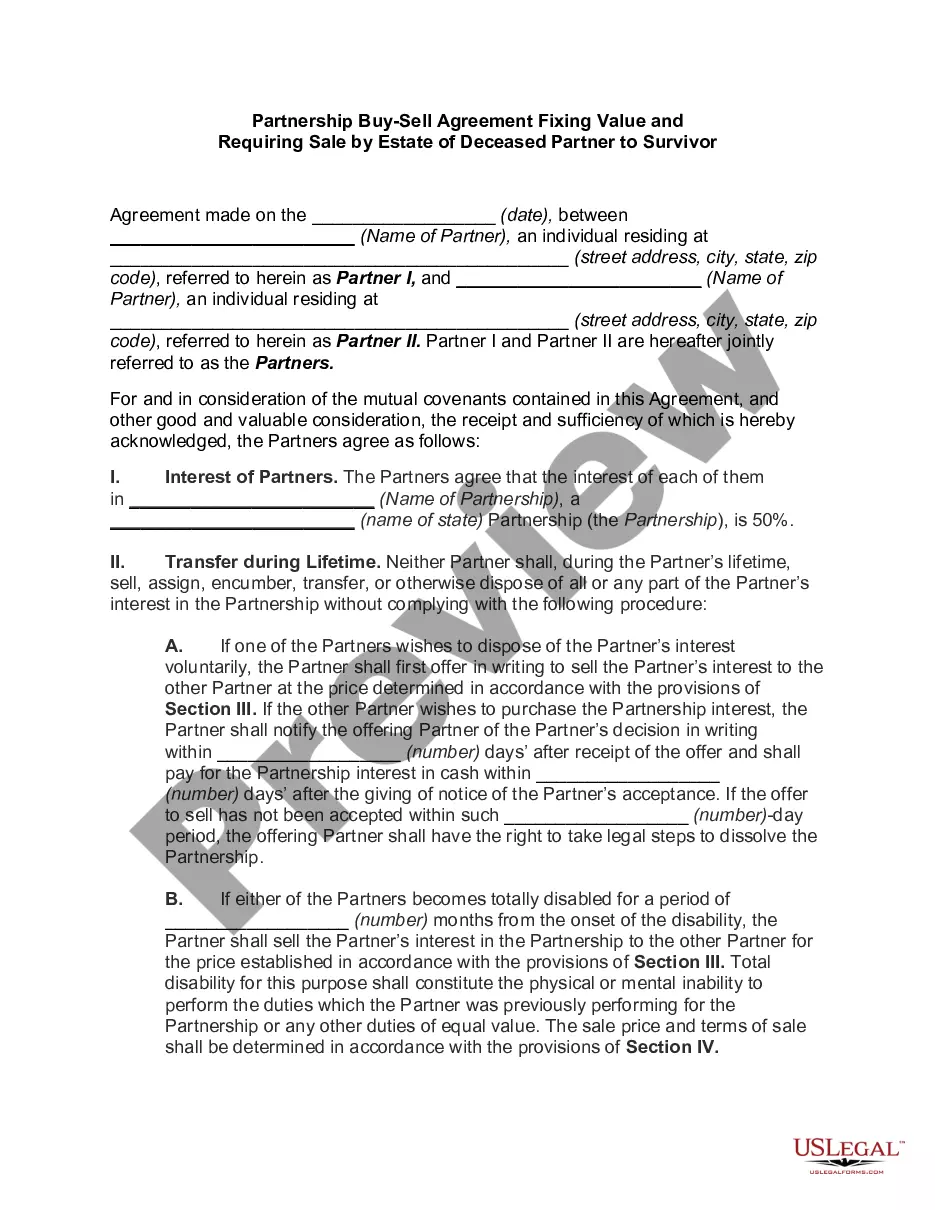

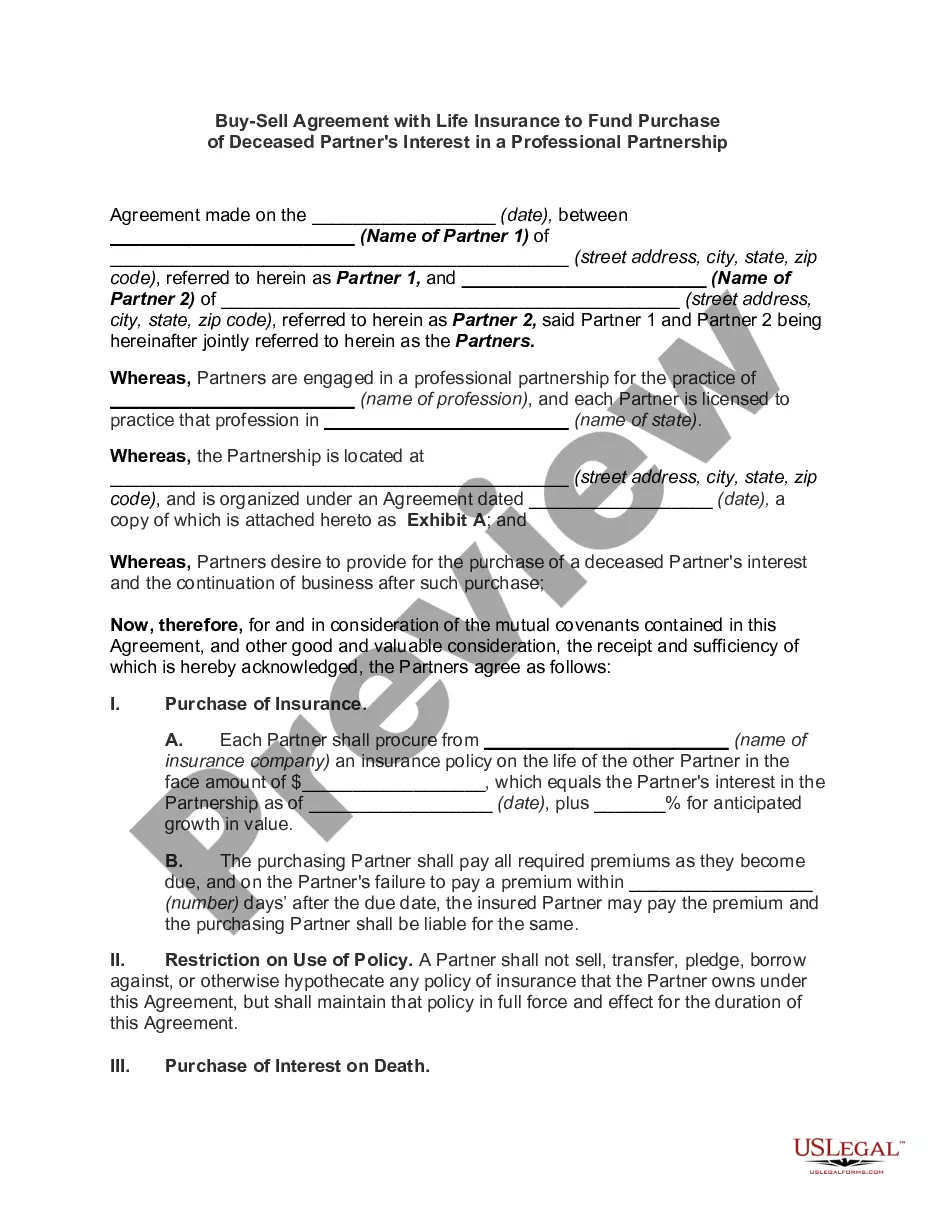

The purpose of this Agreement is to provide for the continuance of the partnership business on the death or retirement of a partner and the purchase of his or her interest in the partnership by the partnership.

Massachusetts Sale of Deceased Partner's Interest

Instant download

Description

Free preview

How to fill out Sale Of Deceased Partner's Interest?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a diverse selection of legal form templates that you can download or print.

By using the site, you can obtain thousands of forms for commercial and personal purposes, categorized by type, state, or keywords. You can access the most recent forms like the Massachusetts Sale of Deceased Partner's Interest in just a few minutes.

If you already have a monthly membership, Log In to download the Massachusetts Sale of Deceased Partner's Interest from the US Legal Forms library. The Download button will appear on every form you view. You can also find all previously downloaded forms in the My documents section of your account.

Each template you add to your account comes with no expiration date and is yours indefinitely. So, if you wish to download or print another copy, simply navigate to the My documents section and click on the form you need.

Access the Massachusetts Sale of Deceased Partner's Interest with US Legal Forms, the most comprehensive library of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal requirements and preferences.

- Ensure you have selected the appropriate form for your city/state. Click the Review button to check the information of the form. Go through the form summary to confirm that you have the right document.

- If the form doesn't meet your needs, utilize the Search section at the top of the screen to find a suitable one.

- If you are content with the form, confirm your selection by hitting the Get now button. Then, choose your preferred pricing plan and enter your details to register for an account.

- Process the transaction. Use your Visa, Mastercard, or PayPal account to complete the transaction.

- Select the file format and download the form onto your device.

- Make changes. Complete, modify, and print and sign the downloaded Massachusetts Sale of Deceased Partner's Interest.

Form popularity

FAQ

Inheritance tax and estate tax are two different things. Inheritance tax is what the beneficiary the person who inherited the wealth must pay when they receive it. Estate tax is the amount that's taken out of someone's estate upon their death. One, both or neither could be a factor when someone dies.

The applicantusually the executor or other fiduciary of an estatewould file Form 4422, Application for Certificate Discharging Property Subject to Estate Tax Lien, with the IRS.

While the Legislature included a throwout rule for sales sourced to a state where the taxpayer is not subject to taxation, Massachusetts has defined subject to taxation very broadly, and few, if any, taxpayers should end up throwing out receipts from sales of services or intangibles on the basis that the receipts

The standard method of obtaining a release of estate tax lien is to file an estate tax return with the Massachusetts Department of Revenue (DOR) and obtain from the DOR a Release of Estate Tax Lien, known as an M-792 certificate. This is the required method when dealing with estates that are worth $1,000,000 or more.

If you're a resident of Massachusetts and leave behind more than $1 million (for deaths occurring in 2022), your estate might have to pay Massachusetts estate tax. The Massachusetts tax is different from the federal estate tax, which is imposed only on estates worth more than $12.06 million (for deaths in 2022).

Massachusetts does not impose an inheritance tax. There is a state estate tax in Massachusetts, however. Estates valued at over $1 million must pay an estate tax.

Any person in actual or constructive possession of any property of the decedent, including probate and nonprobate property, such as jointly owned assets or life insurance. Probate Property.

Depending on the situation surrounding the individual's death, you may be afforded up to a three-year extension, though most given aren't for more than six months. There is no inheritance tax in Massachusetts.

This certificate releases the lien of the Commonwealth of Massachusetts imposed by Chapter 65C of the General Laws, on any and. all interests which the decedent may have had in the property described below: Real Estate (full legal description not necessary)

In addition to this rule, only the value over $40,000 will be subjected to the tax. This means, if the value of an estate exceeds the $1 million threshold, anything above $40,000 will be taxed. Massachusetts uses a graduated tax rate, which ranges between 0.8% and a maximum of 16%.