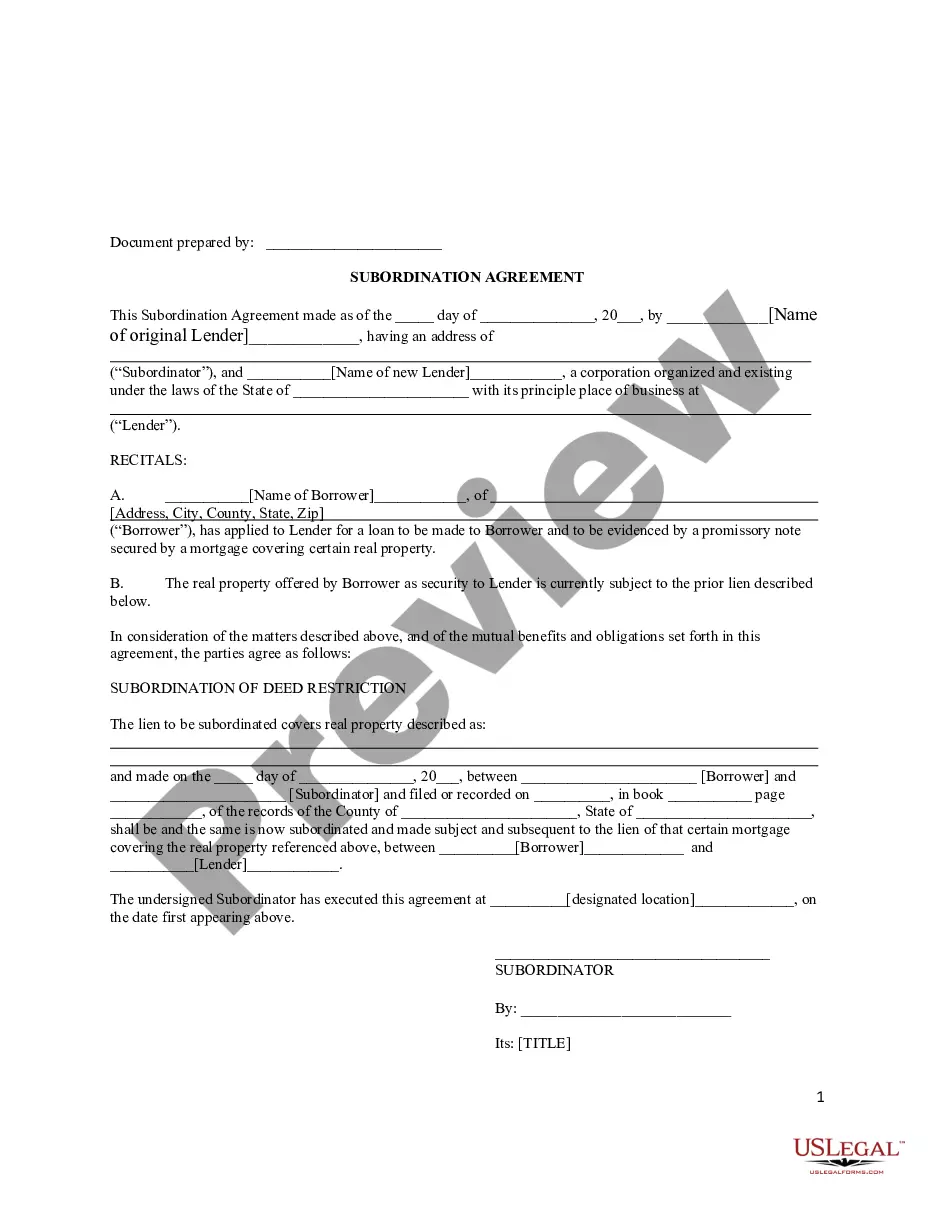

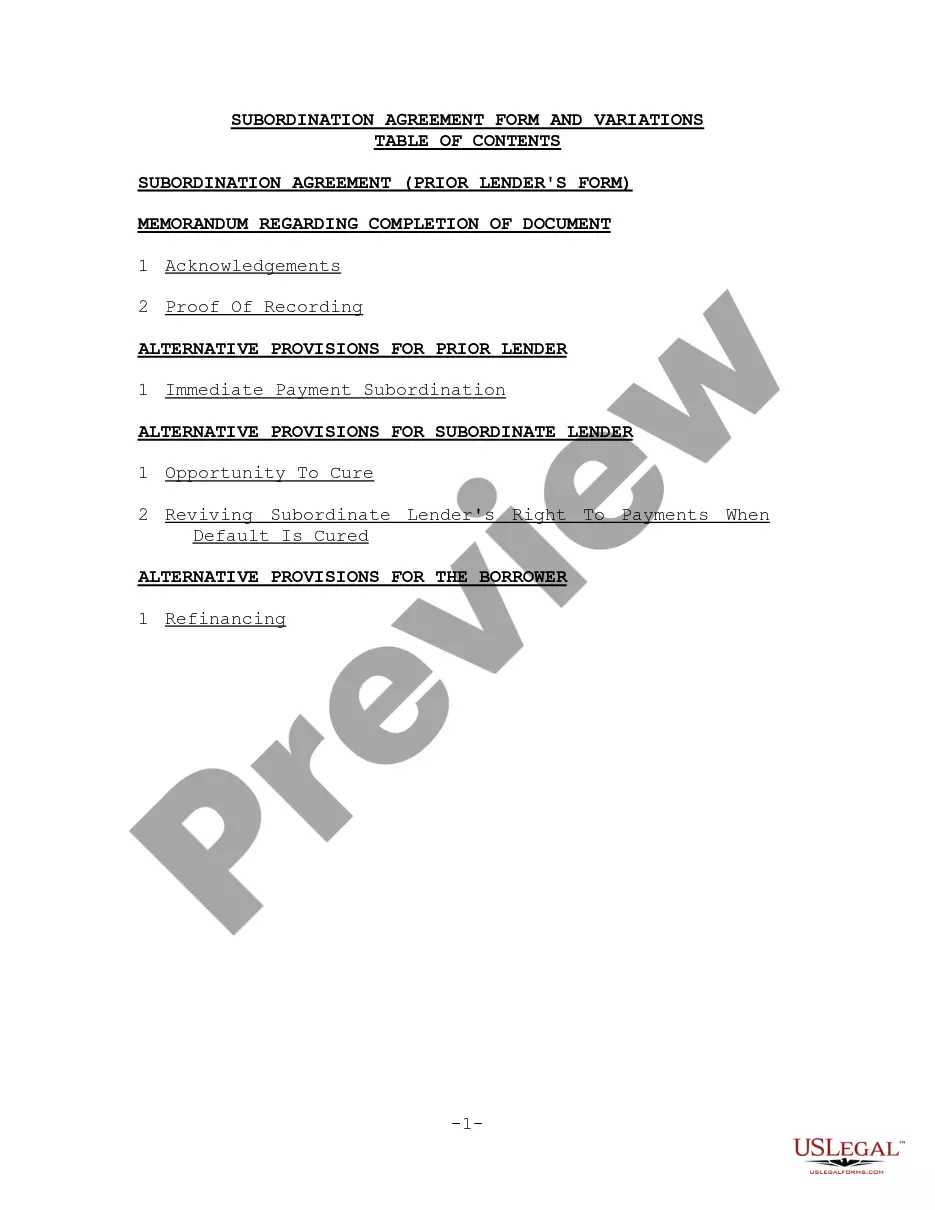

Kentucky Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

Choosing the right lawful record format could be a struggle. Obviously, there are a lot of layouts available online, but how can you discover the lawful kind you need? Use the US Legal Forms web site. The service offers a large number of layouts, including the Kentucky Subordination Agreement Subordinating Existing Mortgage to New Mortgage, that can be used for enterprise and personal requires. All of the kinds are checked out by experts and meet state and federal demands.

In case you are previously authorized, log in to your bank account and click the Acquire switch to have the Kentucky Subordination Agreement Subordinating Existing Mortgage to New Mortgage. Make use of your bank account to look through the lawful kinds you may have purchased formerly. Proceed to the My Forms tab of your bank account and acquire another copy in the record you need.

In case you are a fresh user of US Legal Forms, listed here are simple recommendations that you can stick to:

- Very first, ensure you have selected the proper kind for the city/state. You can look through the form utilizing the Preview switch and look at the form explanation to make certain it will be the right one for you.

- When the kind is not going to meet your preferences, utilize the Seach industry to get the right kind.

- When you are certain that the form is suitable, go through the Get now switch to have the kind.

- Select the costs program you need and enter in the essential information and facts. Design your bank account and pay money for the order with your PayPal bank account or credit card.

- Select the submit formatting and download the lawful record format to your product.

- Comprehensive, edit and printing and indicator the obtained Kentucky Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

US Legal Forms will be the greatest library of lawful kinds in which you can see different record layouts. Use the company to download skillfully-manufactured paperwork that stick to express demands.

Form popularity

FAQ

Again, if you're refinancing your first mortgage and the property also has a subordinate mortgage, the refinancing lender will usually handle the process of getting the necessary subordination agreement. But you need to ensure that the required subordination agreement is completed before the new loan's closing date.

There are also situations where your first purchase loan can become subordinate by law or regulation, without your lender's agreement. Here are two examples: If you have a Federal tax lien for unpaid income taxes, this debt automatically becomes a primary lien ahead of your first mortgage.

Many people have a subordinate mortgage in the form of a home equity line of credit or home equity loan. A subordinate mortgage is secured by your property but sits in second position, if you have a primary mortgage, for getting paid in the event you default.

Any subsequent loan that is taken out after your initial purchase loan is considered to be a junior-lien or subordinate mortgage. Therefore, subordinate financing is the use of two or more mortgages to finance the purchase of real estate or using your home's equity for liquid cash.

Over time, as the homeowner makes good on their monthly payments, the home also tends to appreciate in value. Second mortgages are often riskier because the primary mortgage has priority and is paid first in the event of default.

Many people have a subordinate mortgage in the form of a home equity line of credit or home equity loan. A subordinate mortgage is secured by your property but sits in second position, if you have a primary mortgage, for getting paid in the event you default.

A subordination real estate mortgage clause gives the loan it's in reference to first lien position. It states that any other loans or liens on the property take a second lien position. Most first mortgage lenders won't fund a loan unless there is a subordination clause giving them first lien position.

Getting A Second Mortgage A second mortgage will become a subordinate loan. If you repay the primary loan within the term of the second mortgage, the second mortgage can take its place as the primary loan.