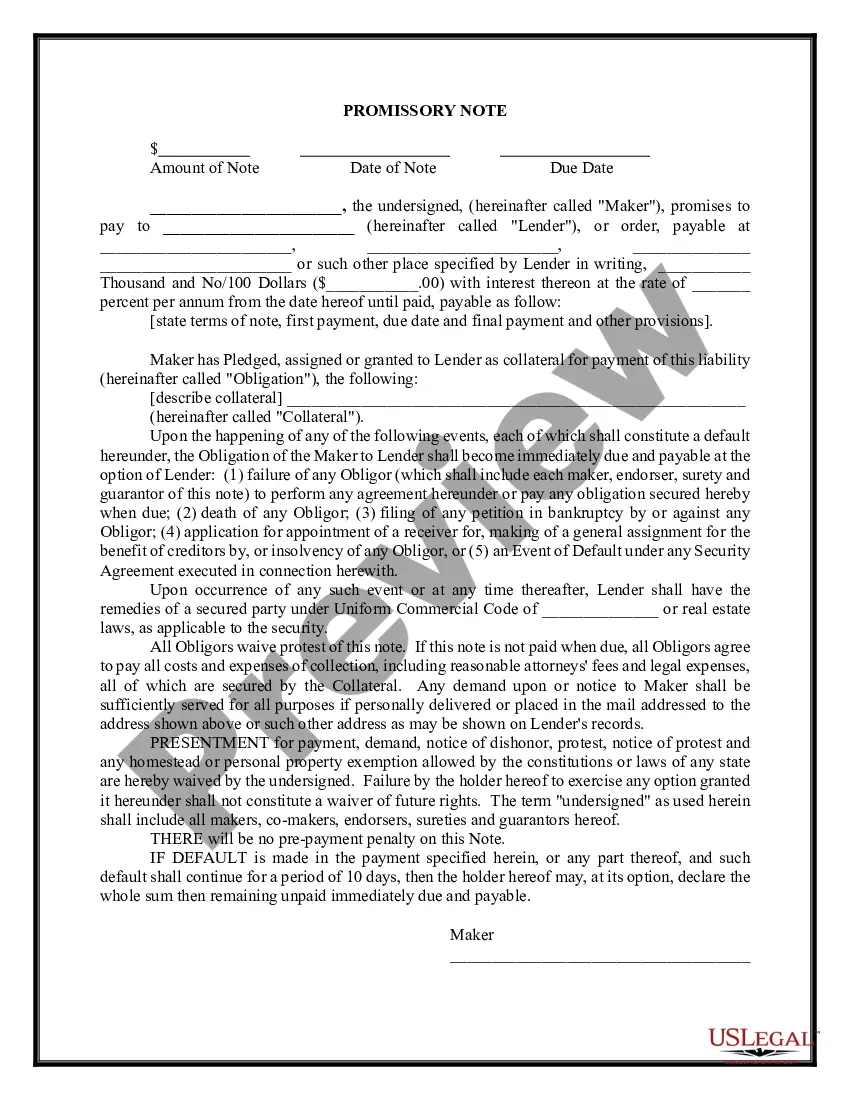

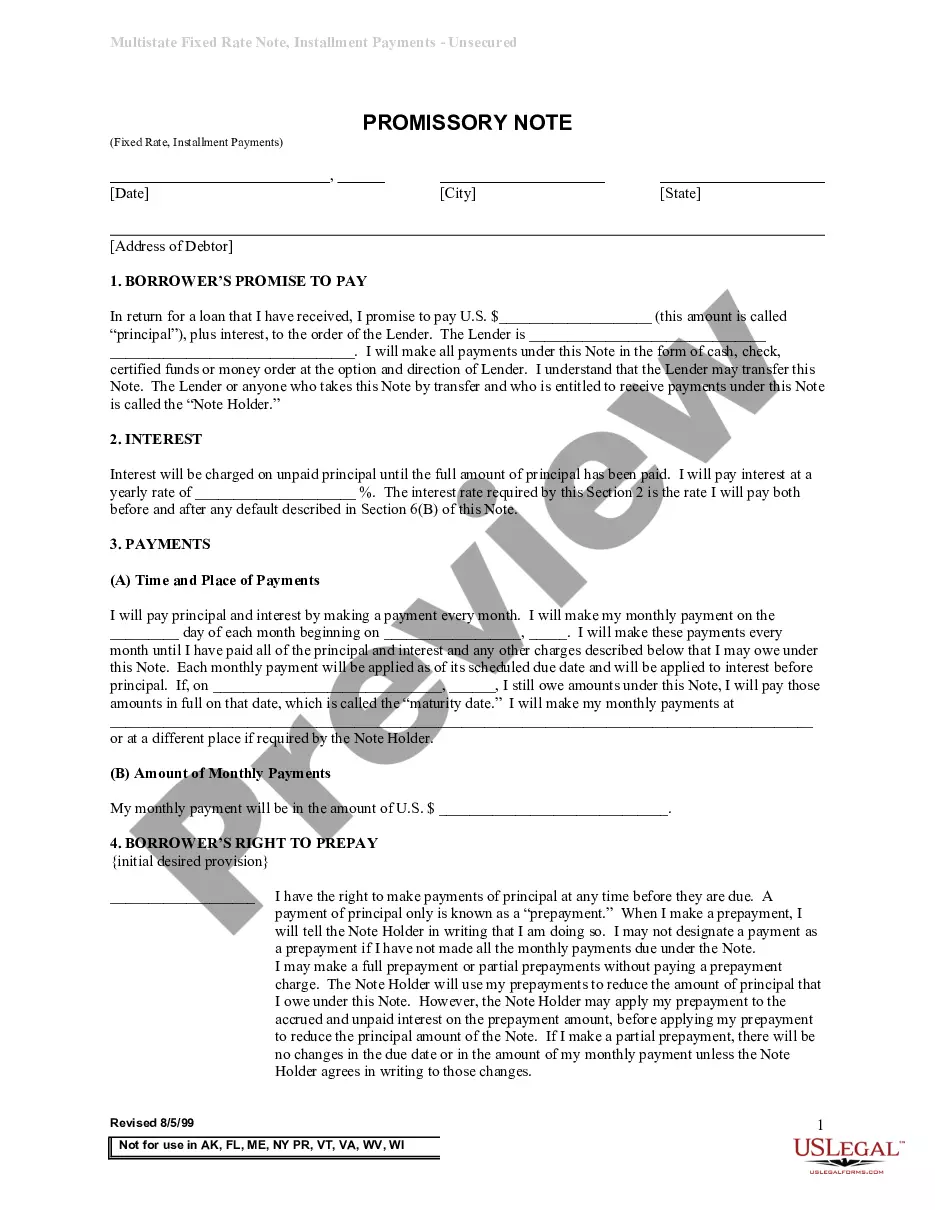

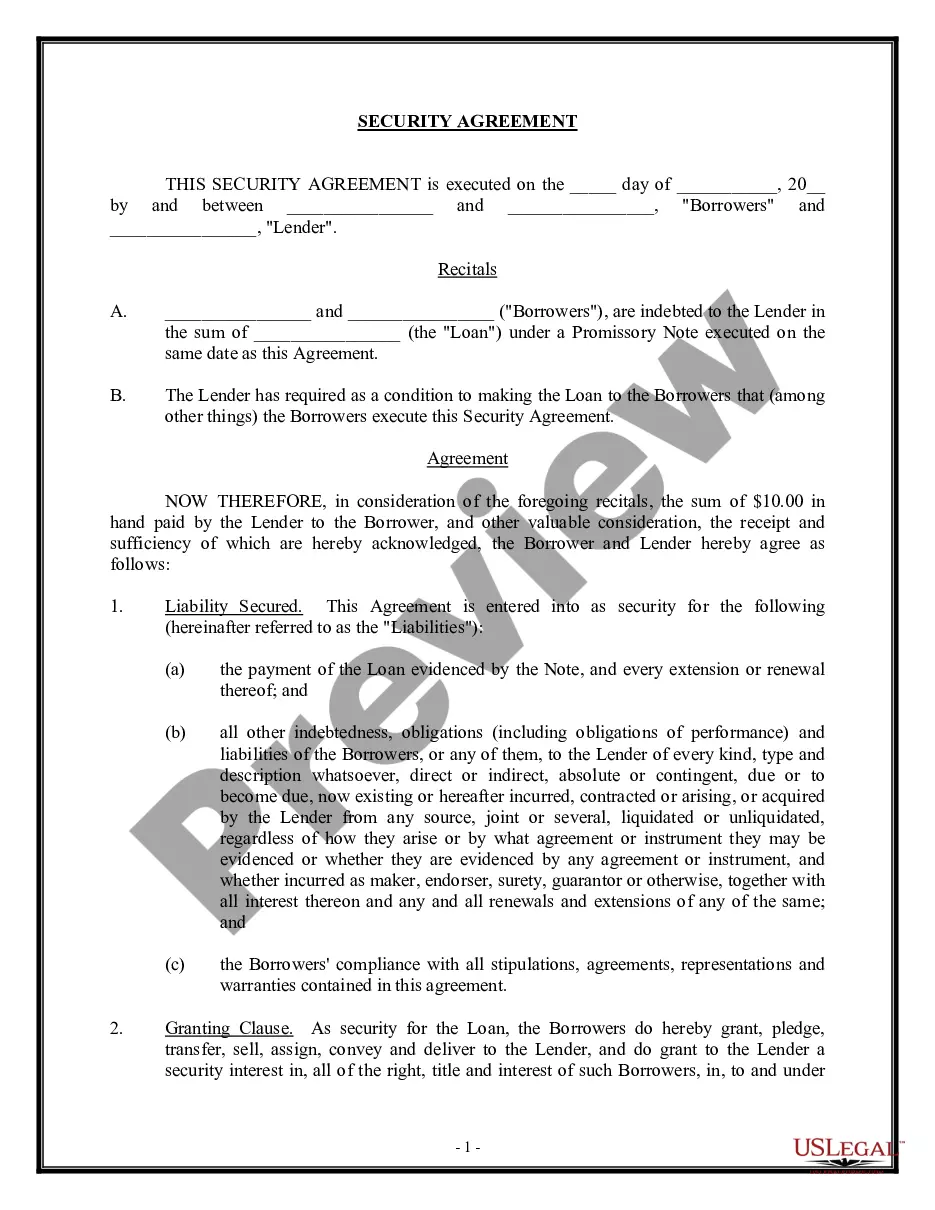

This form is a secured Promissory Note. The borrower promises to make all payments on the loan, with interest, to the lender. The form also provides that the maker has the right to make full or partial prepayments without paying prepayment charges.

Kansas Multistate Promissory Note - Secured

Category:

State:

Multi-State

Control #:

US-00601-A

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Multistate Promissory Note - Secured?

You can utilize time on the web exploring for the legal document template that aligns with the state and federal requirements you will require.

US Legal Forms offers thousands of legal forms that are reviewed by professionals.

You are able to download or print the Kansas Multistate Promissory Note - Secured from my service.

If available, take advantage of the Preview button to review the document template as well.

- If you have a US Legal Forms account, you may Log In and click on the Download button.

- After that, you can complete, modify, print, or sign the Kansas Multistate Promissory Note - Secured.

- Each legal document template you purchase is yours indefinitely.

- To obtain another copy of a purchased form, visit the My documents tab and click on the corresponding button.

- If you are accessing the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document template for the county/town of your preference.

- Check the form description to confirm you have chosen the appropriate form.

Form popularity

FAQ

The structure of a promissory note generally follows a clear format: it starts with the title, then identifies the parties, states the principal amount, outlines the interest rate, details the repayment schedule, and concludes with signatures. For a Kansas Multistate Promissory Note - Secured, including collateral details is crucial, as it provides additional assurance to the lender regarding repayment. This structured approach helps both parties to have a clear understanding of the agreement.

A common example of a promissory note is when a person borrows funds to buy a vehicle. In this scenario, the borrower agrees to repay the lender a specific amount over time, often with interest. The Kansas Multistate Promissory Note - Secured can serve as a legal document to protect both the lender and the borrower, ensuring clarity on repayment terms and conditions.

The format of a promissory note typically includes the heading, parties involved, the amount borrowed, interest rate, repayment schedule, and signatures. A Kansas Multistate Promissory Note - Secured must clearly outline these elements to ensure that both parties understand their rights and obligations. It is important to keep the document organized and straightforward, which helps avoid any confusion during the repayment process.

Yes, the Kansas Multistate Promissory Note - Secured follows a standard format. It typically includes sections for borrower and lender information, repayment terms, and signatures. You can find various templates online that ensure you capture all necessary details. Using platforms like uslegalforms can provide you with professionally drafted formats that meet legal standards.

In Kansas, the statute of limitations for enforcing a promissory note is generally five years. This timeframe begins from the date of default, emphasizing the importance of prompt action in case of non-payment. With a Kansas Multistate Promissory Note - Secured, understanding these legal timelines can help protect your financial interests.

Yes, a promissory note is indeed a legally binding document, provided it includes specific essential elements. This enforceability helps protect the rights of both borrowers and lenders. When dealing with a Kansas Multistate Promissory Note - Secured, you can rest assured that the terms are recognized by law, making adherence crucial.

One notable disadvantage of a promissory note is the potential for default, which can lead to financial loss for the lender. In the case of secured notes, losing collateral can be a concern for borrowers. Additionally, navigating the terms of a Kansas Multistate Promissory Note - Secured may require careful consideration to ensure compliance and protection.

Yes, certain promissory notes, specifically secured ones, are backed by collateral. This collateral serves as assurance for lenders, reinforcing the obligation to repay. By opting for a Kansas Multistate Promissory Note - Secured, borrowers can typically enjoy lower interest rates, thanks to the added security.

The primary distinction lies in collateral. A secured promissory note involves assets backing the obligation, whereas an unsecured note does not involve collateral. In the case of a Kansas Multistate Promissory Note - Secured, the presence of collateral can lower interest rates, providing a clear advantage for both borrower and lender.

Yes, a promissory note can be secured by collateral, which provides a safety net for lenders. With a Kansas Multistate Promissory Note - Secured, borrowers pledge assets to ensure repayment. This arrangement increases the lender's security, making it a favorable option in many lending situations.