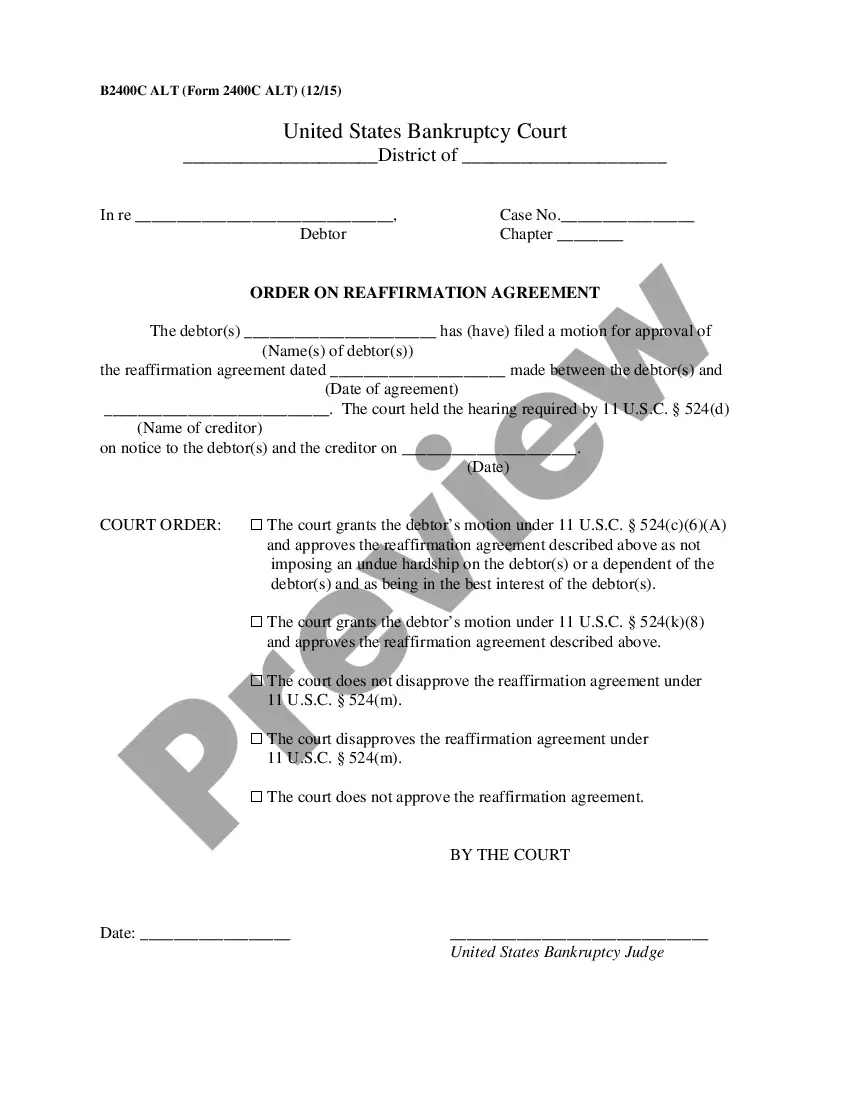

Indiana Reaffirmation Agreement, Motion and Order

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Reaffirmation Agreement, Motion And Order?

Choosing the best authorized record template can be quite a battle. Naturally, there are plenty of themes available on the Internet, but how do you get the authorized type you want? Take advantage of the US Legal Forms website. The assistance offers a large number of themes, such as the Indiana Reaffirmation Agreement, Motion and Order, which you can use for business and personal demands. Each of the types are checked out by pros and meet federal and state specifications.

Should you be presently authorized, log in to the profile and then click the Down load key to get the Indiana Reaffirmation Agreement, Motion and Order. Utilize your profile to appear with the authorized types you possess bought formerly. Proceed to the My Forms tab of your respective profile and have yet another duplicate from the record you want.

Should you be a brand new user of US Legal Forms, listed below are straightforward guidelines that you can comply with:

- Very first, make certain you have selected the correct type for your area/area. You may examine the form while using Review key and read the form explanation to ensure this is the right one for you.

- When the type does not meet your expectations, use the Seach field to find the proper type.

- Once you are certain the form is suitable, select the Buy now key to get the type.

- Opt for the pricing prepare you need and type in the required information. Create your profile and pay for the order utilizing your PayPal profile or bank card.

- Select the file structure and down load the authorized record template to the system.

- Full, change and print out and indicator the received Indiana Reaffirmation Agreement, Motion and Order.

US Legal Forms is definitely the most significant catalogue of authorized types in which you can find different record themes. Take advantage of the company to down load skillfully-made paperwork that comply with state specifications.

Form popularity

FAQ

Agreeing to repay the excess loan amount in ance with the terms of the promissory note is called ?reaffirmation.? You can reaffirm an excess loan amount by signing a reaffirmation agreement with your loan servicer.

A reaffirmed debt remains your personal legal obligation to pay. Your reaffirmed debt is not discharged in your bankruptcy case. That means that if you default on your reaffirmed debt after your bankruptcy case is over, your creditor may be able to take your property or your wages.

You may rescind (cancel) your Reaffirmation Agreement at any time before the bankruptcy court enters your discharge, or during the 60-day period that begins on the date your Reaffirmation Agreement is filed with the court, whichever occurs later.

Reaffirming puts you personally on the hook for the debt, even after your discharge. The Court may not approve the reaffirmation if it is not in your best interest. The agreement is voluntary for you and for the creditor?the creditor may refuse to offer a reaffirmation.

For example, if a debtor reaffirms a car loan for $15,000 and the car securing the loan is worth $8,000, then, if the debt or defaults, the creditor may repossess the car and the debtor may still be liable to the creditor for $7,000 (the difference between the amount of the l oan and the value of the car at the time it ...

To cancel a reaffirmation agreement, you must notify the creditor. It is a good idea to notify the creditor in writing via certified mail with a return receipt postcard so you have proof that you have rescinded the agreement.