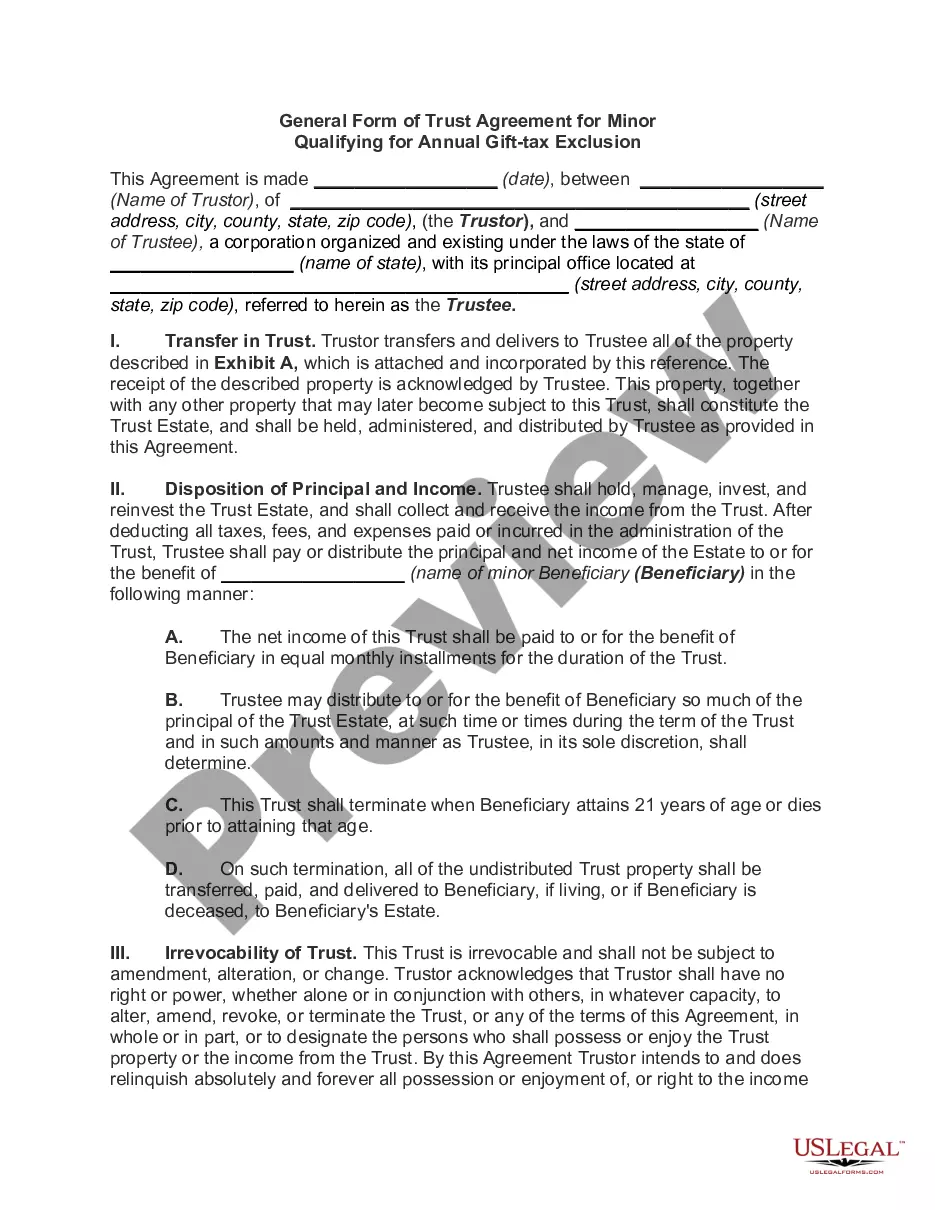

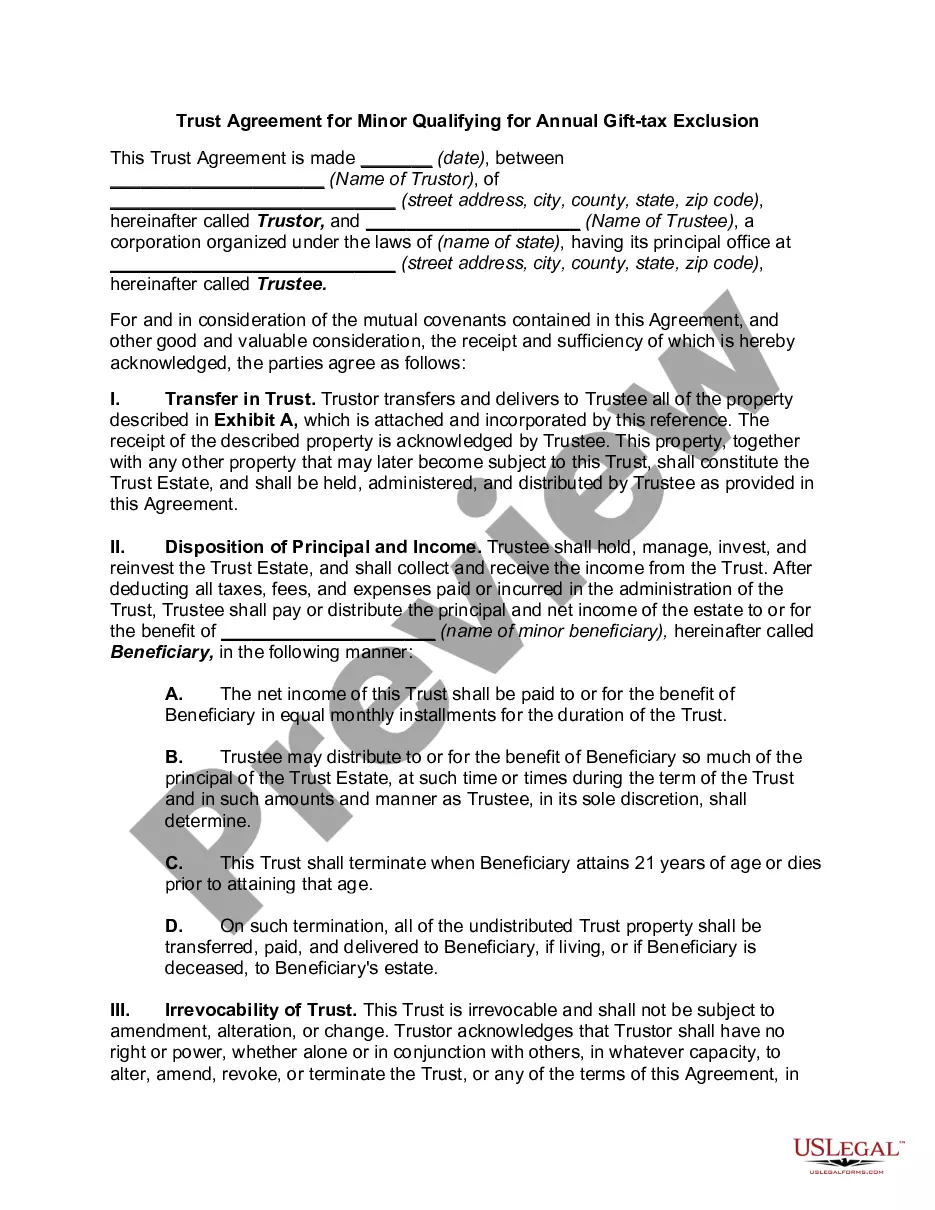

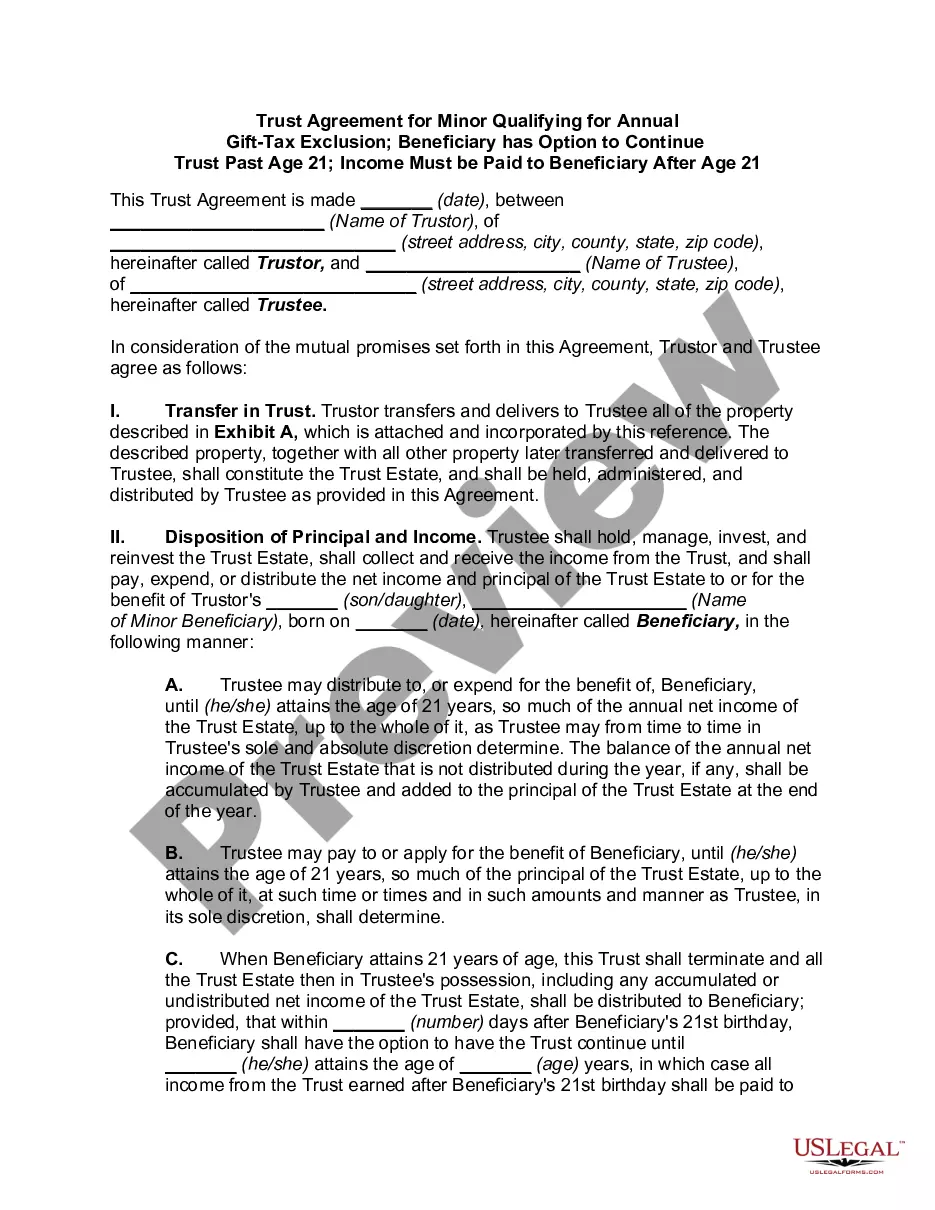

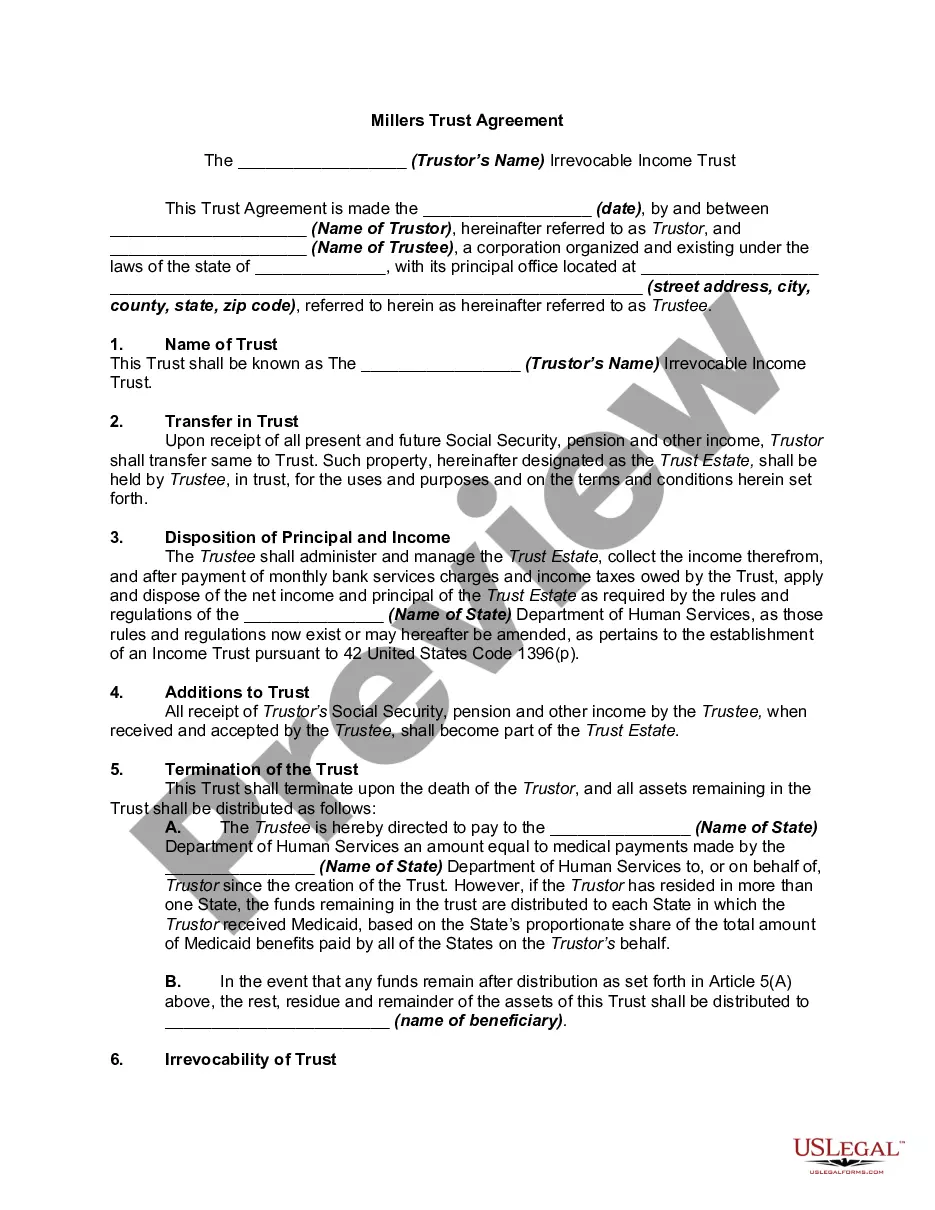

This form set up what is known as present interest trusts, with the intention of meeting the requirements of Section 2503(c) of the Internal Revenue Code.

Indiana Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children

Instant download

Description

Free preview

How to fill out Trust Agreement For Minors Qualifying For Annual Gift Tax Exclusion - Multiple Trusts For Children?

If you require thorough, download, or generate legal document templates, utilize US Legal Forms, the largest assortment of legal forms, which are available online.

Employ the site's straightforward and user-friendly search to locate the documents you need.

A selection of templates for business and personal purposes are categorized by groups and states, or keywords.

Step 4. After you have located the form you need, click on the Get now button. Choose the pricing plan you prefer and enter your credentials to register for an account.

Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the transaction.

- Use US Legal Forms to access the Indiana Trust Agreement for Minors Eligible for Annual Gift Tax Exclusion - Multiple Trusts for Children in just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and click the Download button to find the Indiana Trust Agreement for Minors Eligible for Annual Gift Tax Exclusion - Multiple Trusts for Children.

- You can also access forms you previously obtained from the My documents tab of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Utilize the Preview option to review the form’s details. Don’t forget to read the documentation.

- Step 3. If you are not satisfied with the form, use the Search bar at the top of the screen to find other versions of the legal form template.

Form popularity

FAQ

The best type of trust to set up largely depends on your specific financial and familial goals. Generally, a revocable living trust can offer flexibility for estate planning, while irrevocable trusts provide tax benefits and asset protection. For educational purposes, an Indiana Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children can be valuable to help ensure your beneficiaries, especially minors, receive adequate support over time.

The best type of trust for a minor is often an irrevocable trust, such as a 2503(c) trust, as it qualifies for annual gift tax exclusions and provides specific guidelines for how and when assets are distributed. This approach helps manage the funds effectively until the minor is of age. Remember to consider an Indiana Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children for a comprehensive solution.

The Uniform Transfers to Minors Act (UTMA) allows for assets to be transferred to minors without the need for a formal trust. In contrast, a 2503(c) trust is a formal trust that specifically qualifies for gift tax exclusions, allowing contributions to be managed more closely. When choosing between these options, an Indiana Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children can help clarify which structure best meets your goals.

The best type of trust for minors often includes irrevocable trusts like the 2503(c) trust, which allows parents to contribute gifts that qualify for the annual gift tax exclusion. These trusts are beneficial because they provide ultimate control over the assets and how they are distributed to minors. When setting up an Indiana Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, consider factors like flexibility and long-term management.

A minor trust is a trust specifically designed to hold and manage assets for the benefit of a minor until they reach adulthood or a specified age. These trusts often provide for the management of these assets in a way that supports the child's financial needs, while also adhering to regulations that qualify for tax exclusions. Utilizing an Indiana Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children can streamline the process of creating these trusts.

To establish a trust in Indiana, the trust must be created by written agreement, which clearly outlines the trust's terms and objectives. It must identify the trustee, beneficiaries, and the property involved. If you are considering an Indiana Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, ensure that the agreement complies with state laws and clearly states how assets will be managed for the minors.

Certain transactions may not qualify as gifts, including payments made directly for tuition or medical bills. To clearly differentiate between gifts and non-gifts, it is vital to consult an expert. Through the Indiana Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, you can better understand each transaction’s implications and navigate gifting rules more effectively.

In Indiana, as per IRS guidelines, you can gift up to a specific amount, known as the annual exclusion limit, without incurring gift tax. This limit is set at a federal level and applies regardless of state-specific laws. By leveraging the Indiana Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, you can effectively distribute gifts to your children while ensuring compliance with tax regulations.

When gifting to a non-US citizen spouse, the annual exclusion does not apply in the same manner as it does for US citizen spouses. Instead, you can use a special exemption that allows a higher gift amount without paying tax. This dynamic is crucial when considering an Indiana Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, as it helps to optimize your gifting strategy across different beneficiaries.

Annual exclusion gifts refer to amounts that you can give to any individual each year without incurring gift tax. For the current tax year, this limit is set by the IRS and can change annually. Utilizing the Indiana Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children allows you to strategically allocate gifts over multiple trusts, thus benefiting your minor beneficiaries while avoiding tax liabilities.