Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

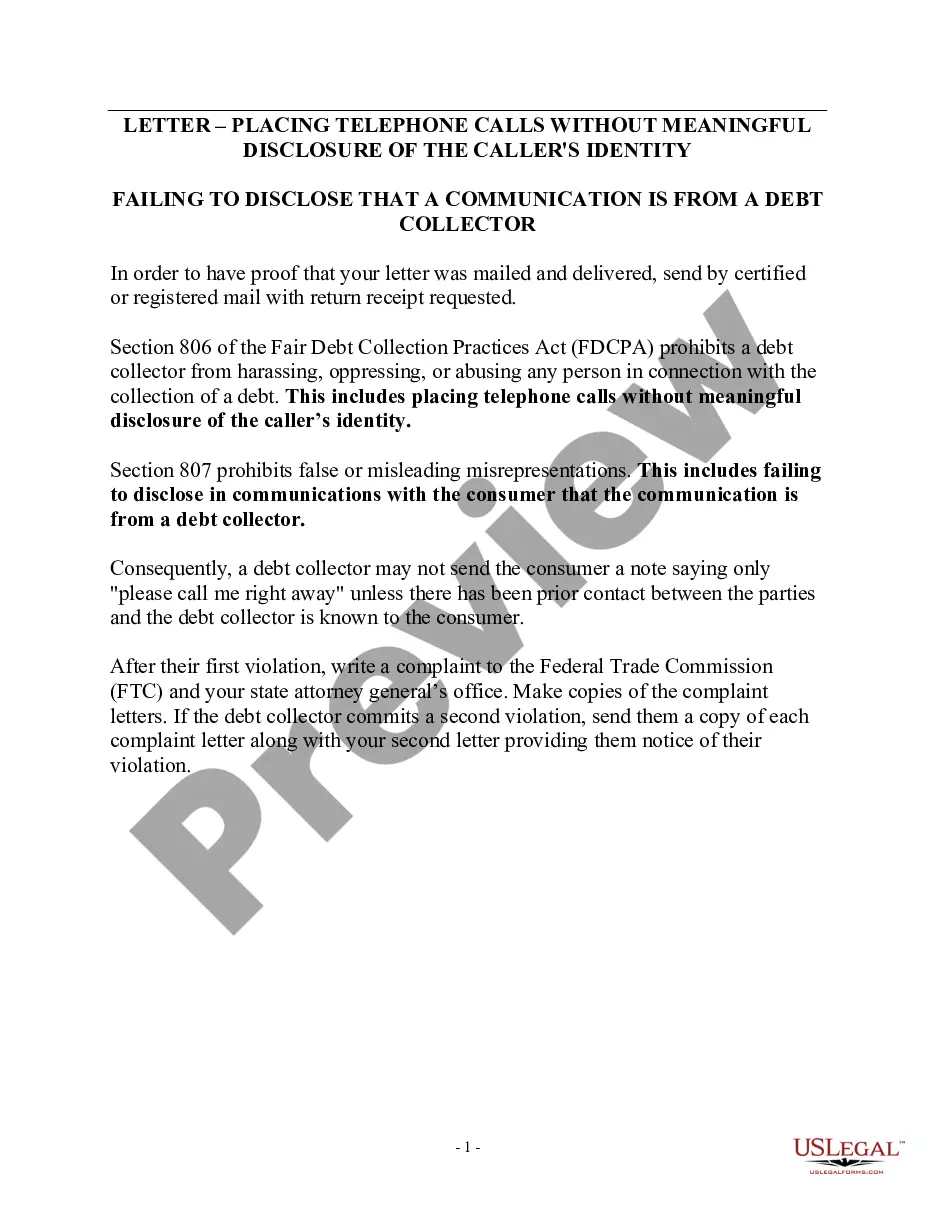

A debt collector may not harass, oppress, or abuse any person in connection with the collection of a debt. This includes leaving telephone messages with neighbors or other 3rd parties when the debt collector knows the consumer's name and telephone number and could have contacted the consumer directly.

Iowa Notice to Debt Collector - Unlawful Messages to 3rd Parties

Category:

State:

Multi-State

Control #:

US-DCPA-28

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Notice To Debt Collector - Unlawful Messages To 3rd Parties?

Finding the appropriate legal document template can be a challenge. Indeed, there are numerous templates accessible online, but how do you obtain the legal form you require.

Utilize the US Legal Forms website. The platform provides thousands of templates, including the Iowa Notice to Debt Collector - Unlawful Messages to 3rd Parties, suitable for both business and personal purposes. All forms are reviewed by professionals and comply with federal and state regulations.

If you are already registered, Log In to your account and click the Obtain button to get the Iowa Notice to Debt Collector - Unlawful Messages to 3rd Parties. Leverage your account to access the legal forms you have previously acquired. Visit the My documents section of your account and download another copy of the document you need.

US Legal Forms is indeed the largest collection of legal forms where you can browse various document templates. Utilize the service to download properly crafted paperwork that adhere to state requirements.

- Firstly, ensure you have chosen the correct form for your city/county. You can preview the form using the Preview button and examine the form description to confirm it is indeed the right one for you.

- If the form does not satisfy your requirements, use the Search field to find the appropriate form.

- Once you are confident that the form is suitable, select the Acquire now button to obtain the form.

- Choose the pricing plan you wish and provide the required information. Create your account and pay for the transaction using your PayPal account or credit card.

- Select the document format and download the legal document template to your device.

- Complete, modify, print, and sign the obtained Iowa Notice to Debt Collector - Unlawful Messages to 3rd Parties.

Form popularity

FAQ

If you're dealing with a third-party debt collector, there are five things you can do to handle the situation.Don't ignore them. Debt collectors will continue to contact you until a debt is paid.Get information on the debt.Get it in writing.Don't give personal details over the phone.Try settling or negotiating.

Don't be surprised if debt collectors slide into your DMs. A new rule allows debt collectors to contact you on social media, text or email not just by phone. The rule, which was approved last year by the Consumer Financial Protection Bureau's former president Kathleen L. Kraninger, took effect Tuesday, Nov.

Debt collectors are allowed to call you, but they cannot always leave a message on your answering machine. There are a few main instances when debt collectors might be sued for violating the privacy of those who are in debt, through a voicemail message. One of those instances is when it is accessed by a third party.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

Generally, a debt collector can't discuss your debt with anyone other than:You.Your spouse.Your parents (if you are a minor)Your guardian, executor, or administrator.Your attorney, if you are represented with respect to the debt.

Debt collectors are allowed to contact third parties to obtain or confirm location information, but the FDCPA does not allow debt collectors to leave messages with third parties. Location information is defined as a consumer's home address and home phone number or workplace and workplace address.

If you do have a legitimate issue with a debt collection that shows up on your credit report, you can dispute it through the collector or the credit bureaus. To contact the collector directly, be sure you file a letter in writing within 30 days of first receiving communication about the debt.

Under the FDCPA, a communication from a debt collector must meaningfully disclose the identity of the debt collector and provide what is called a "mini-Miranda" warning. The communication must identify the debt collector (name, employer, and telephone number).