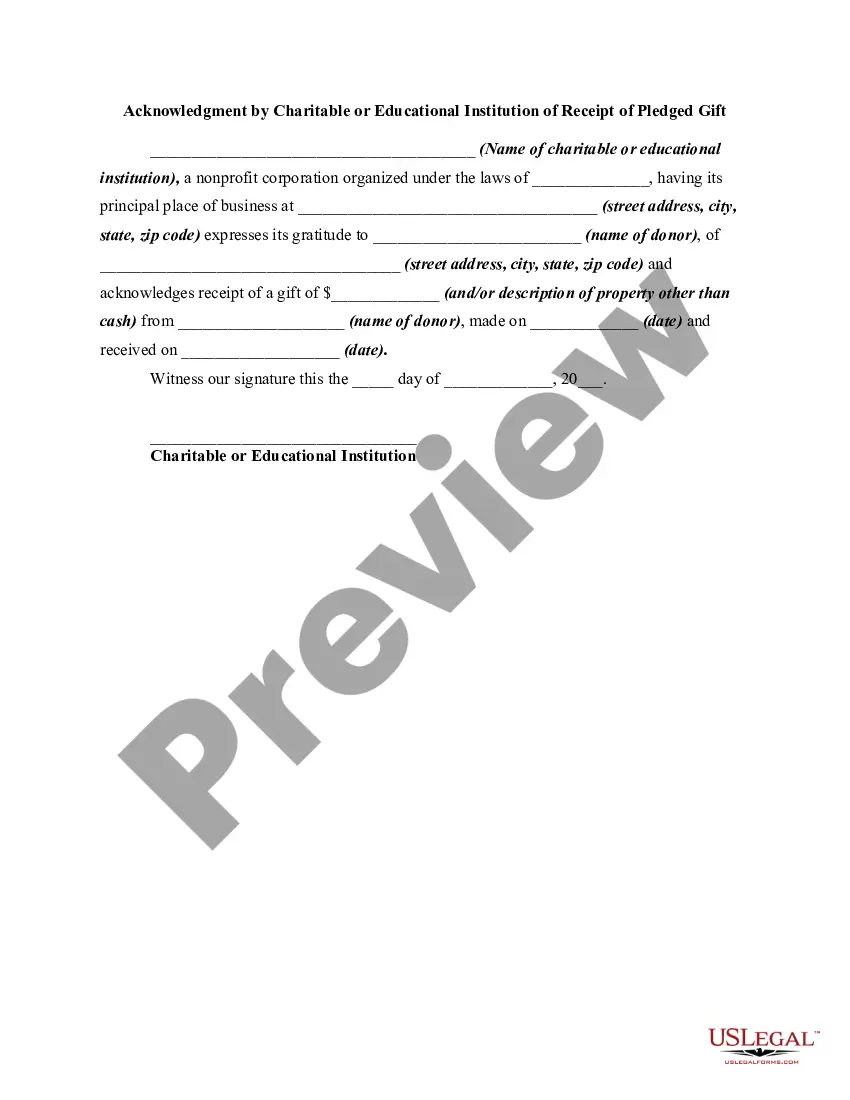

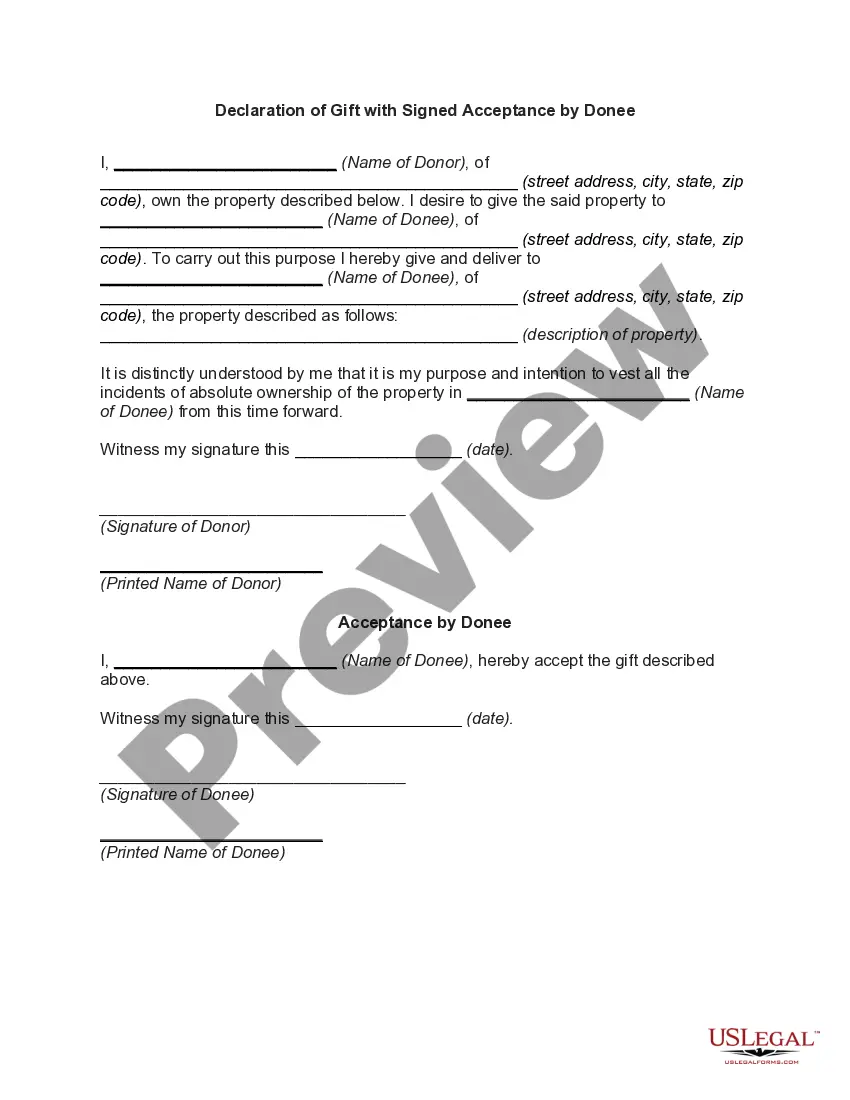

Iowa Acknowledgment by Charitable or Educational Institution of Receipt of Gift

Description

How to fill out Acknowledgment By Charitable Or Educational Institution Of Receipt Of Gift?

Finding the appropriate valid document template can be quite challenging. Certainly, there are numerous templates accessible online, but how do you find the valid form you require? Utilize the US Legal Forms website.

The service provides a vast array of templates, including the Iowa Acknowledgment by Charitable or Educational Institution of Receipt of Gift, which can be used for both business and personal purposes. All of the forms are reviewed by experts and meet federal and state regulations.

If you are already registered, Log In to your account and click on the Acquire button to obtain the Iowa Acknowledgment by Charitable or Educational Institution of Receipt of Gift. Use your account to verify the valid forms you have previously ordered. Navigate to the My documents section of your account and retrieve another copy of the document you require.

Complete, modify, print, and sign the received Iowa Acknowledgment by Charitable or Educational Institution of Receipt of Gift. US Legal Forms is the largest library of valid forms where you can find a variety of document templates. Utilize the service to download professionally created files that comply with state requirements.

- If you are a new user of US Legal Forms, here are simple instructions for you to follow.

- First, ensure you have selected the correct form for your area/region. You can review the form using the Review option and examine the form details to confirm this is the right one for you.

- If the form does not meet your requirements, use the Search field to locate the appropriate form.

- Once you are confident that the form is correct, select the Acquire now button to obtain the form.

- Choose the pricing plan you prefer and provide the necessary information. Create your account and complete your purchase using your PayPal account or Visa or Mastercard.

- Select the file format and download the valid document template to your device.

Form popularity

FAQ

Writing a receipt for a charitable donation involves including specific information to meet the Iowa Acknowledgment by Charitable or Educational Institution of Receipt of Gift standards. Start with your organization's name and contact details, then list the donor's information, the donation amount, and the date. Finally, make sure to include a statement indicating that no goods or services were provided in exchange for the gift. Tools such as US Legal Forms can help you generate a professional receipt quickly and easily.

To acknowledge receipt of a donation, a charitable or educational institution should provide a formal letter or receipt that includes important details. This document should state the donor's name, the amount of the gift, and the date it was received. By doing this, you fulfill the Iowa Acknowledgment by Charitable or Educational Institution of Receipt of Gift requirement. Utilizing platforms like US Legal Forms can streamline the process, ensuring that you create a compliant acknowledgment effortlessly.

To acknowledge a gift from a donor-advised fund, the charitable organization should issue a written acknowledgment that includes the donor's name, the amount received, and the date of the gift. It is important to clarify that the donation comes from the donor-advised fund, as this impacts the donor's tax implications. Utilizing our platform, US Legal Forms, can simplify the process of creating a compliant Iowa Acknowledgment by Charitable or Educational Institution of Receipt of Gift, ensuring that all necessary details are included.

The gift law in Iowa outlines the regulations surrounding the acceptance and reporting of donations by charitable organizations. It mandates that institutions must provide proper acknowledgements to donors, especially for contributions exceeding a certain amount. Understanding the Iowa Acknowledgment by Charitable or Educational Institution of Receipt of Gift is crucial for compliance, as it helps organizations navigate their legal responsibilities while fostering trust with their supporters.

An example of a written acknowledgement for a charitable contribution includes a letter that specifies the donor's name, the amount of the gift, and the date it was received. It may also express gratitude and mention how the donation will be used. This aligns with the Iowa Acknowledgment by Charitable or Educational Institution of Receipt of Gift, ensuring that the donor has a clear record for their tax filings and personal records.

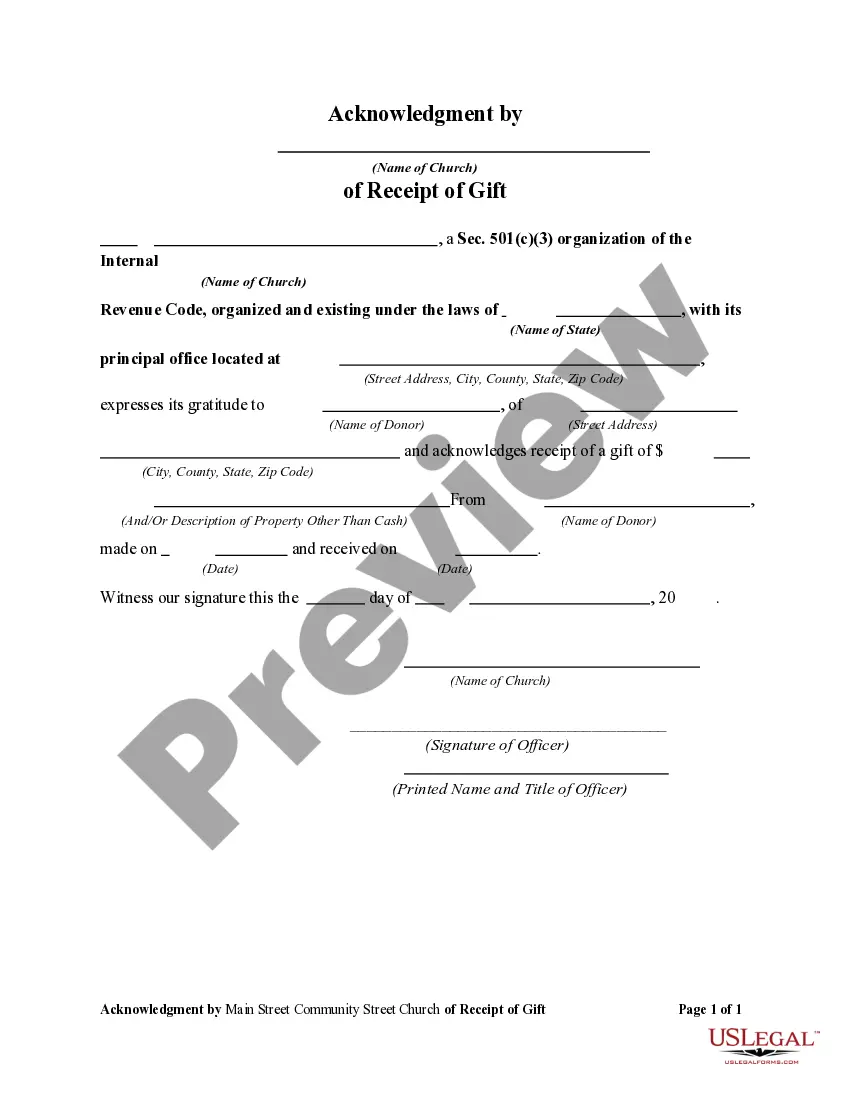

A gift acknowledgement is a formal document that a charitable or educational institution provides to recognize the receipt of a donation. This document serves as proof for the donor, confirming that their contribution has been received and is appreciated. In the context of Iowa Acknowledgment by Charitable or Educational Institution of Receipt of Gift, it is essential for tax purposes and helps maintain transparency between the donor and the organization.

What is Acknowledged Documents? A document is an exception to the Hearsay Rule if it is accompanied by a certificate of acknowledgment that is lawfully executed by a notary public or another officer who is authorized to take acknowledgments.

An Iowa notary acknowledgment form is used to authenticate a signed document. The document is presented to a commissioned officer (notary public) at which point the notary will verify the identities of all signing parties. When getting a document acknowledged, the signature fields can be filled out ahead of time.

After witnessing the document being signed, the Notary then completes the appropriate certificate wording for the signature witnessing. An acknowledgment, on the other hand, does not require the Notary to witness the signature in most states.

121.004. METHOD OF ACKNOWLEDGMENT. (a) To acknowledge a written instrument for recording, the grantor or person who executed the instrument must appear before an officer and must state that he executed the instrument for the purposes and consideration expressed in it. (3) seal the certificate with the seal of office.