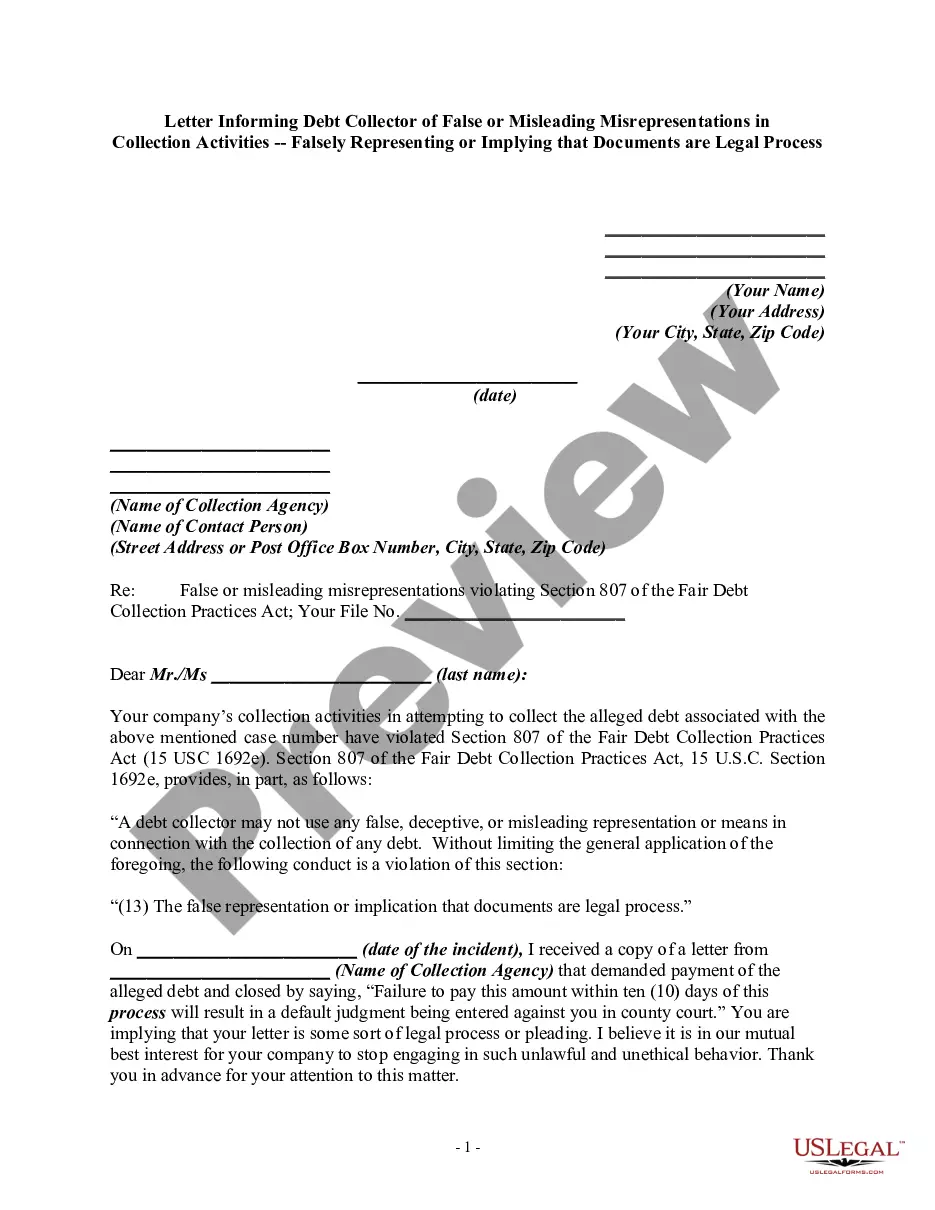

A debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of a debt. This includes falsely representing or implying that documents are legal process.

Hawaii Notice to Debt Collector - Falsely Representing a Document is Legal Process

Category:

State:

Multi-State

Control #:

US-DCPA-40

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Falsely Representing A Document Is Legal Process?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a broad selection of legal document formats that you can download or create.

By using the website, you can discover thousands of forms for both business and personal purposes, categorized by types, states, or keywords. You can find the latest versions of forms, such as the Hawaii Notice to Debt Collector - Falsely Representing a Document as Legal Process in just a few seconds.

If you have a subscription, Log In and download the Hawaii Notice to Debt Collector - Falsely Representing a Document as Legal Process from the US Legal Forms repository. The Download button appears on every form you view. You have access to all previously downloaded forms via the My documents tab in your account.

Proceed with the purchase. Use a credit card or PayPal account to complete the transaction.

Choose the format and download the document to your device. Edit the form, fill it out, print it, and sign the downloaded Hawaii Notice to Debt Collector - Falsely Representing a Document as Legal Process. Each template added to your account has no expiration date and is yours indefinitely. Thus, if you wish to download or print another copy, simply go to the My documents section and click on the form you need. Access the Hawaii Notice to Debt Collector - Falsely Representing a Document as Legal Process with US Legal Forms, the most extensive collection of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal requirements.

- Ensure you have selected the appropriate form for your region/area.

- Click on the Preview button to review the form's content.

- Examine the form details to confirm you have chosen the right document.

- If the form does not meet your requirements, utilize the Search field at the top of the screen to find the one that does.

- If you are satisfied with the document, confirm your selection by clicking the Buy Now button.

- Then, select the pricing plan you desire and provide your credentials to register for the account.

Form popularity

FAQ

Disputing a false collection involves sending a formal dispute letter to the debt collector. In your letter, specify what you believe is incorrect and ask for validation of the debt. Taking this action is essential, particularly when confronting a Hawaii Notice to Debt Collector - Falsely Representing a Document is Legal Process.

Fighting false debt collection begins with carefully documenting all communications with the collector. You should gather evidence that demonstrates the inaccuracies, such as false claims or deceptive documents. This can significantly aid in your defense, especially in cases involving the Hawaii Notice to Debt Collector - Falsely Representing a Document is Legal Process.

To write a dispute to a debt collector, you should clearly state your intention to dispute the debt and include any relevant details. Be sure to request verification of the debt and make your communication through certified mail for documentation. These steps can help you effectively tackle any inaccuracies, particularly regarding a Hawaii Notice to Debt Collector - Falsely Representing a Document is Legal Process.

The 777 rule refers to the requirement that debt collectors must provide specific disclosures when attempting to collect a debt. This rule ensures that collectors identify themselves and include information about the debt. Knowing about the 777 rule can empower consumers, especially when they encounter a Hawaii Notice to Debt Collector - Falsely Representing a Document is Legal Process.

In Hawaii, the statute of limitations on debt collection typically spans six years. This period begins when the debt becomes delinquent, meaning when you miss a payment. Understanding this timeline is crucial, as it affects your rights in situations involving the Hawaii Notice to Debt Collector - Falsely Representing a Document is Legal Process.

15 US Code 1692 1 addresses false and deceptive practices in debt collection. It prohibits debt collectors from using misleading forms or communications that may falsely represent the legal status of a debt. Under this regulation, if a collector misrepresents a document as a legal process, it can be challenged through a Hawaii Notice to Debt Collector - Falsely Representing a Document is Legal Process.

The 777 rule is a guideline that refers to the legal obligations of debt collectors to verify a debt within seven days after their initial contact. This rule ensures that consumers have a chance to dispute the debt before further actions are taken. Familiarity with the 777 rule can empower individuals receiving notices, particularly those concerning the Hawaii Notice to Debt Collector - Falsely Representing a Document is Legal Process. US Legal Forms provides resources to help you navigate through these communications confidently.

A false and misleading debt collection practice occurs when a debt collector misrepresents the character, amount, or legal status of a debt. This includes using misleading documents, making false statements about legal action, or claiming to be affiliated with a government agency. Understanding these practices is essential when dealing with notices, especially under the Hawaii Notice to Debt Collector - Falsely Representing a Document is Legal Process. You can rely on US Legal Forms to help document and address these practices effectively.