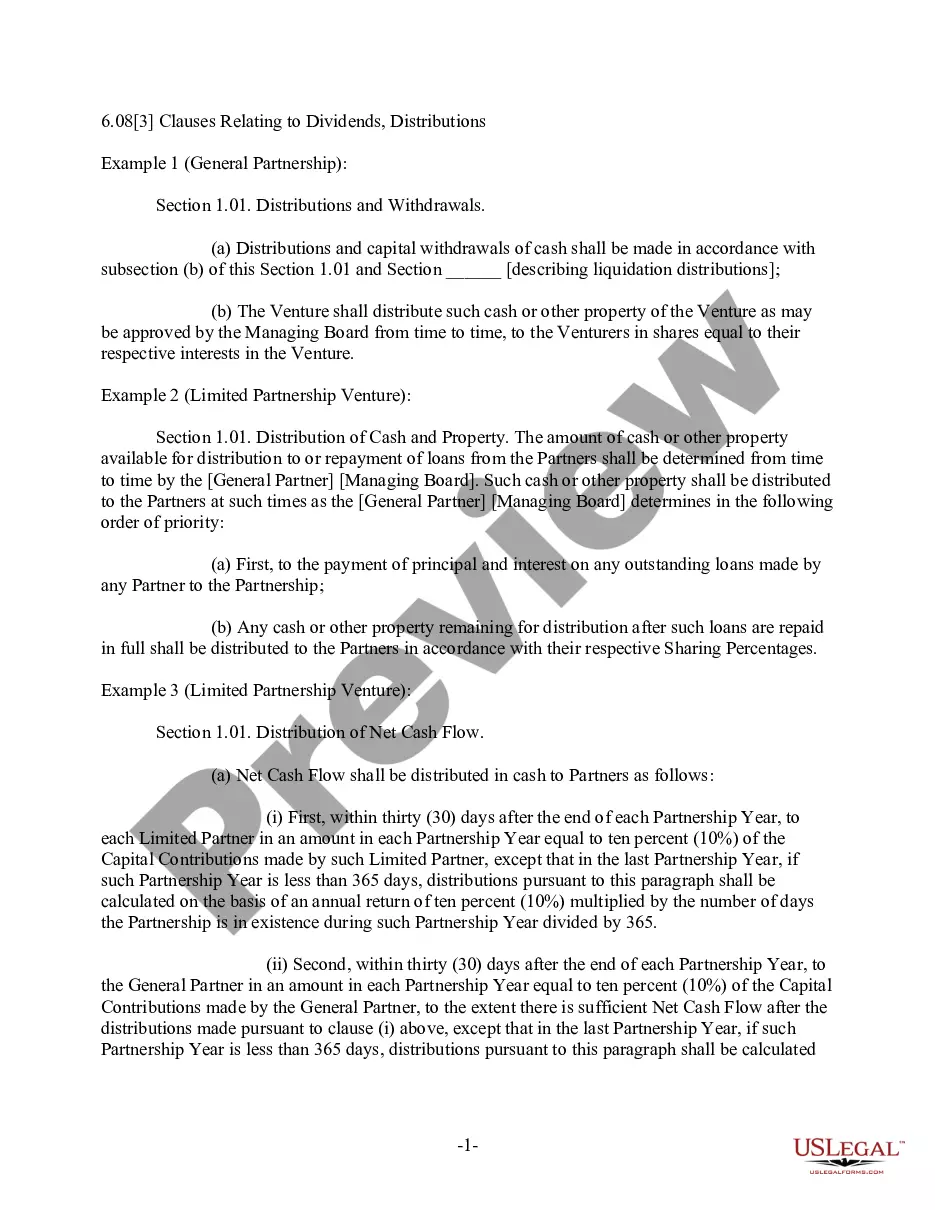

Guam Clauses Relating to Preferred Returns

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Clauses Relating To Preferred Returns?

US Legal Forms - one of the biggest libraries of lawful forms in the States - gives a wide array of lawful file web templates you are able to down load or print. While using site, you may get a huge number of forms for business and individual functions, categorized by categories, states, or keywords and phrases.You will discover the latest types of forms like the Guam Clauses Relating to Preferred Returns in seconds.

If you already possess a registration, log in and down load Guam Clauses Relating to Preferred Returns through the US Legal Forms collection. The Down load button can look on each and every form you perspective. You gain access to all formerly saved forms inside the My Forms tab of your accounts.

If you want to use US Legal Forms the very first time, here are simple recommendations to get you began:

- Ensure you have chosen the right form to your area/county. Click the Review button to analyze the form`s content material. Look at the form explanation to actually have selected the appropriate form.

- In case the form doesn`t suit your demands, take advantage of the Search area on top of the display screen to get the one which does.

- Should you be content with the shape, verify your option by clicking the Purchase now button. Then, choose the costs prepare you want and give your qualifications to register for the accounts.

- Method the transaction. Use your charge card or PayPal accounts to perform the transaction.

- Choose the formatting and down load the shape on your own product.

- Make adjustments. Fill out, revise and print and indication the saved Guam Clauses Relating to Preferred Returns.

Each design you added to your money does not have an expiration date and is your own property eternally. So, in order to down load or print another version, just proceed to the My Forms segment and then click around the form you need.

Obtain access to the Guam Clauses Relating to Preferred Returns with US Legal Forms, one of the most extensive collection of lawful file web templates. Use a huge number of skilled and status-distinct web templates that meet your organization or individual needs and demands.

Form popularity

FAQ

Therefore, preferred stock dividends in arrears are legal obligations to be paid to preferred shareholders before any common stock shareholder receives any dividend. All previously omitted dividends must be paid before any current year dividends may be paid.

ASC 480-10-25-4 A mandatorily redeemable financial instrument shall be classified as a liability unless the redemption is required to occur only upon the liquidation or termination of the reporting entity.

ASC 480 defines a freestanding financial instrument as ?a financial instrument that is entered into separately and apart from any of the entity's other financial instruments or equity transactions, or that is entered into in conjunction with some other transaction and is legally detachable and separately exercisable.? ...

ASC 480-10 requires (1) issuers to classify certain types of shares of stock and certain share-settled contracts as liabilities or, in some circumstances, as assets and (2) SEC registrants to classify certain types of redeemable equity instruments as temporary equity.

As discussed in ASC 480-10-55-33, a warrant on redeemable shares (i.e., puttable or mandatorily redeemable shares) is a liability within the scope of ASC 480 because it creates a conditional obligation for the reporting entity to repurchase its shares for cash (or other assets).

It is a clause that also gives preferred stock holders priority of accumulated dividends over common stockholders in the event that the underlying asset is faced with a liquidity event.

Typically in a Preferred Equity investment, all cash flow or profits are paid back to the preferred investors (after all debt has been repaid) until they receive the agreed upon ?preferred return,? for example, 12%. Remaining distributions of cash flow are returned to Common Equity holders.

Accounting Standards Codification (ASC) 480, Distinguishing Liabilities from Equity topic, contains one subtopic: ASC 480-10, Overall, which provides guidance on how an issuer classifies and measures financial instruments with characteristics of both liabilities and equity.