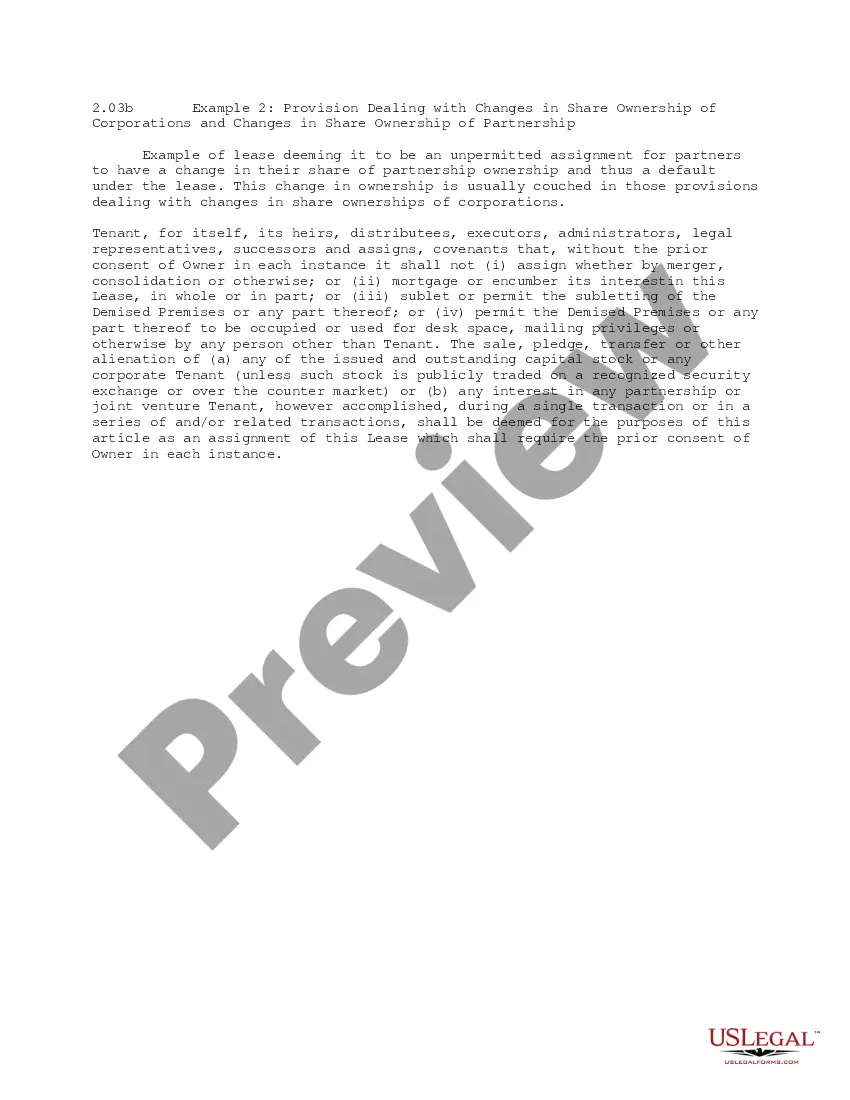

This office lease provision refers to a tenant that is a partnership or if the tenant's interest in the lease shall be assigned to a partnership. Any such partnership, professional corporation and such persons will be held by this provision of the lease.

Guam Standard Provision to Limit Changes in a Partnership Entity

Category:

State:

Multi-State

Control #:

US-OL203A

Format:

Word;

PDF

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Standard Provision To Limit Changes In A Partnership Entity?

Are you in a position where you need to have documents for either business or specific functions almost every time? There are plenty of lawful record layouts available on the net, but locating versions you can trust isn`t straightforward. US Legal Forms offers a large number of kind layouts, just like the Guam Standard Provision to Limit Changes in a Partnership Entity, which are written in order to meet federal and state needs.

If you are already informed about US Legal Forms website and possess your account, just log in. After that, you may acquire the Guam Standard Provision to Limit Changes in a Partnership Entity web template.

Unless you offer an account and need to start using US Legal Forms, follow these steps:

- Discover the kind you will need and ensure it is for the right metropolis/region.

- Utilize the Preview button to analyze the shape.

- See the information to ensure that you have chosen the proper kind.

- In the event the kind isn`t what you`re trying to find, utilize the Research industry to discover the kind that meets your needs and needs.

- Whenever you find the right kind, simply click Acquire now.

- Pick the pricing strategy you would like, fill in the required info to generate your account, and pay for the transaction making use of your PayPal or Visa or Mastercard.

- Pick a convenient paper file format and acquire your copy.

Locate each of the record layouts you may have bought in the My Forms menu. You can aquire a extra copy of Guam Standard Provision to Limit Changes in a Partnership Entity whenever, if necessary. Just go through the required kind to acquire or print out the record web template.

Use US Legal Forms, one of the most substantial selection of lawful varieties, to conserve time as well as prevent blunders. The support offers appropriately created lawful record layouts that can be used for an array of functions. Produce your account on US Legal Forms and begin producing your lifestyle a little easier.

Form popularity

FAQ

There must be at least one limited partner and one general partner (GP) to form a limited partnership. The general partner oversees and manages the limited partnership, and the limited partners are not active in managing the business.

A limited partnership has two types of partners: general partners and limited partners. It must have one or more of each type. All partner, limited and general, share the profits of the business. Each general partner has unlimited liability for the obligations of the business.

As discussed in ASC 740-10-15-2, ASC 740's principles and requirements apply to domestic and foreign entities, including not-for-profit (NFP) entities with activities that are subject to income taxes, and applies to federal, state, local (including some franchise), and foreign taxes based on income.

Limited Partnership and Taxes Limited partnerships are treated as pass-through entities and file Form 1065 as an information return. The limited partnership also provides a Schedule K-1 to each partner so that their share of business income and losses can be reported on the partner's individual tax return.

The most common type of partner is a general partner, who actively manages and exercises control over the business operations. Limited partners have limited legal liability. This type of partner cannot manage or exercise control over the business.

The most common types of limited partners in the venture capital ecosystem are individuals, institutions, and family offices. Individual LPs are typically high-net-worth individuals who invest their own personal capital into venture capital funds.

In the United States, general and limited partnerships (except certain ?master limited partnerships? discussed below) are not subject to tax because their earnings and losses are passed directly to their owners and taxed at that level. ASC 740 does not apply to such partnerships.

There are three relatively common partnership types: general partnership (GP), limited partnership (LP) and limited liability partnership (LLP).