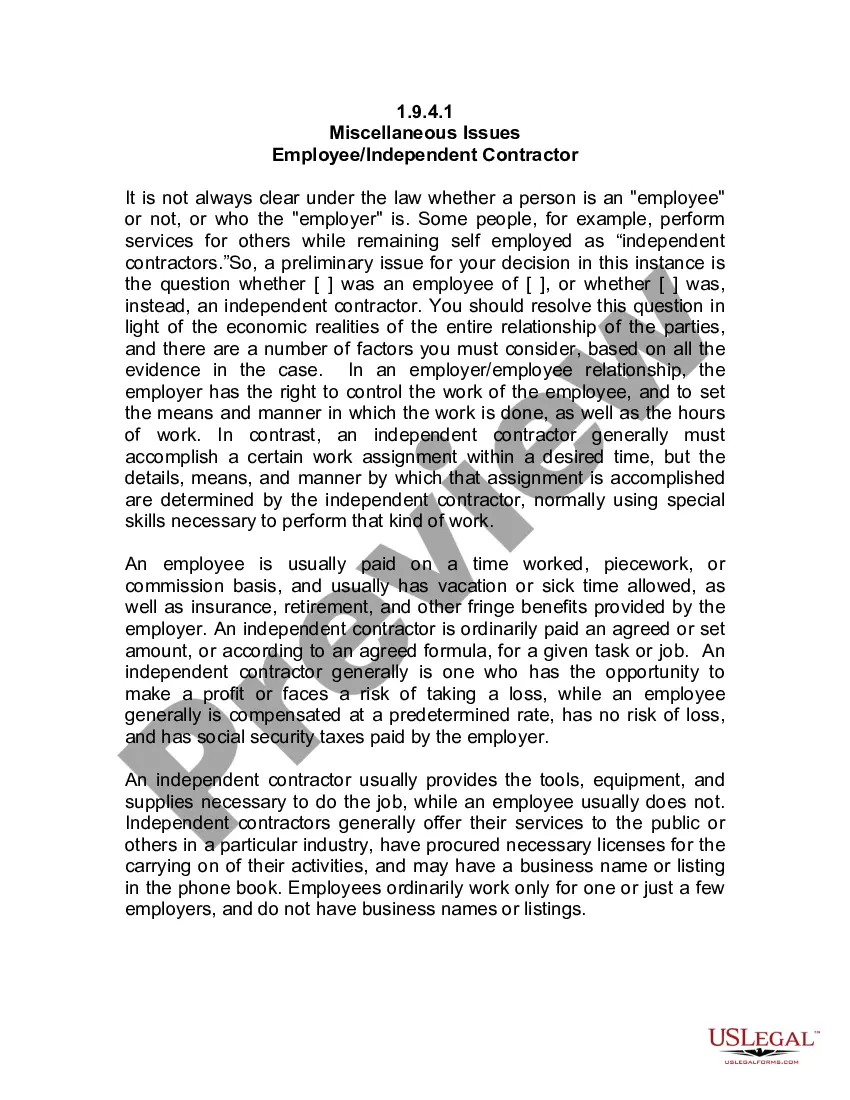

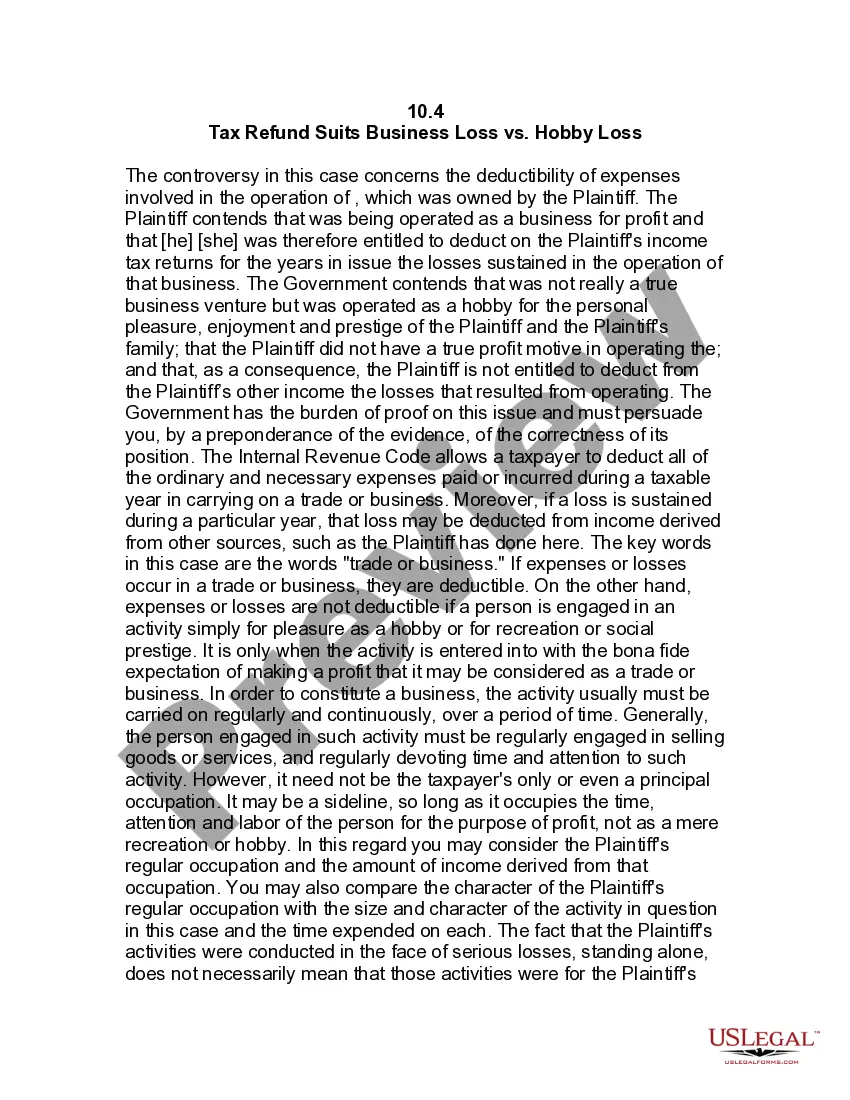

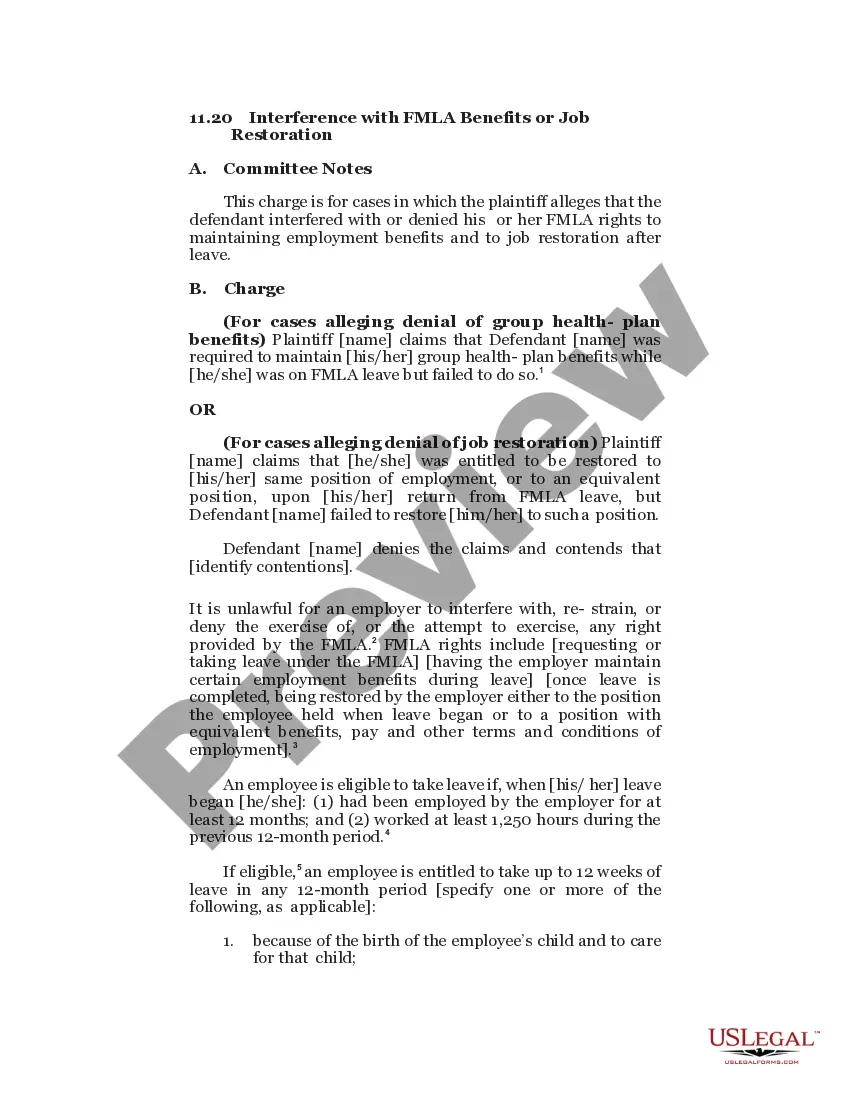

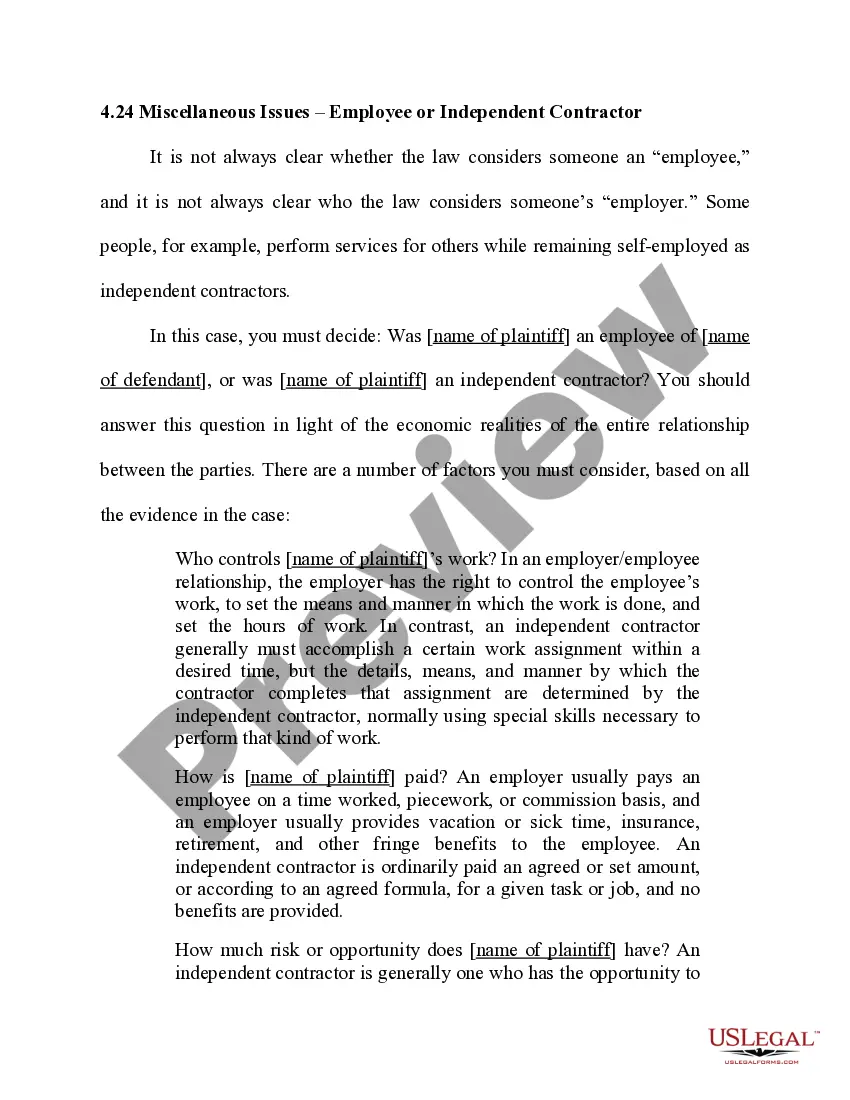

Guam Jury Instruction - 10.10.3 Employee vs. Self-Employed Independent Contractor

Description

How to fill out Jury Instruction - 10.10.3 Employee Vs. Self-Employed Independent Contractor?

Are you in the placement where you will need papers for possibly organization or individual reasons virtually every working day? There are tons of legal document themes accessible on the Internet, but finding versions you can depend on isn`t straightforward. US Legal Forms gives a huge number of form themes, much like the Guam Jury Instruction - 10.10.3 Employee vs. Self-Employed Independent Contractor, which are composed in order to meet federal and state needs.

Should you be already informed about US Legal Forms site and also have a merchant account, simply log in. Afterward, you are able to obtain the Guam Jury Instruction - 10.10.3 Employee vs. Self-Employed Independent Contractor web template.

If you do not have an accounts and want to start using US Legal Forms, abide by these steps:

- Obtain the form you want and ensure it is to the proper town/region.

- Take advantage of the Review button to check the shape.

- Browse the explanation to actually have selected the right form.

- In case the form isn`t what you are trying to find, use the Search discipline to find the form that meets your needs and needs.

- Once you get the proper form, simply click Acquire now.

- Select the rates strategy you would like, submit the specified info to create your account, and buy an order using your PayPal or charge card.

- Select a handy file structure and obtain your backup.

Discover all the document themes you may have purchased in the My Forms food list. You can obtain a extra backup of Guam Jury Instruction - 10.10.3 Employee vs. Self-Employed Independent Contractor any time, if possible. Just go through the needed form to obtain or produce the document web template.

Use US Legal Forms, one of the most comprehensive collection of legal kinds, in order to save time as well as stay away from faults. The support gives skillfully manufactured legal document themes that can be used for a range of reasons. Make a merchant account on US Legal Forms and begin creating your lifestyle easier.

Form popularity

FAQ

The general rule is that an individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done. If you are an independent contractor, then you are self-employed.

Becoming an independent contractor is one of the many ways to be classified as self-employed. By definition, an independent contractor provides work or services on a contractual basis, whereas, self-employment is simply the act of earning money without operating within an employee-employer relationship.

Benefits of being an independent contractor Independent contractors get to be their own boss. ... Independent contractors have flexibility over their working hours. ... Independent contractors earn more (before tax) ... Independent contractors can claim deductions. ... Independent contractors can experiment with business ideas.

The law further states that independent contractor status is evidenced if the worker: (1) has a substantial investment in the business other than personal services, (2) purports to be in business for himself or herself, (3) receives compensation by project rather than by time, (4) has control over the time and place ...

What Is an Independent Contractor? An independent contractor is a self-employed person or entity contracted to perform work for?or provide services to?another entity as a non-employee. As a result, independent contractors must pay their own Social Security and Medicare taxes.

Generally speaking, the difference between independent contractors and employees in California is whether or not the entity paying for services has the right to control or direct the manner and means of work (tending to signify an employment relationship.)