Guam Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor

Description

How to fill out Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor?

Discovering the right legal record format could be a battle. Naturally, there are plenty of web templates accessible on the Internet, but how can you get the legal develop you want? Take advantage of the US Legal Forms site. The service offers 1000s of web templates, like the Guam Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor, that you can use for organization and personal demands. All of the forms are checked out by pros and meet up with federal and state requirements.

If you are previously authorized, log in to the accounts and then click the Download button to have the Guam Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor. Make use of accounts to search from the legal forms you possess ordered earlier. Visit the My Forms tab of your respective accounts and get yet another backup from the record you want.

If you are a fresh customer of US Legal Forms, listed here are easy guidelines that you can stick to:

- First, ensure you have selected the correct develop to your metropolis/state. You can examine the shape utilizing the Preview button and read the shape explanation to make certain this is the best for you.

- If the develop fails to meet up with your expectations, take advantage of the Seach discipline to discover the right develop.

- Once you are sure that the shape is proper, go through the Acquire now button to have the develop.

- Select the costs prepare you need and enter in the required info. Build your accounts and purchase an order utilizing your PayPal accounts or charge card.

- Choose the document format and down load the legal record format to the system.

- Complete, change and print out and indicator the attained Guam Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor.

US Legal Forms may be the biggest catalogue of legal forms that you will find various record web templates. Take advantage of the service to down load skillfully-made files that stick to status requirements.

Form popularity

FAQ

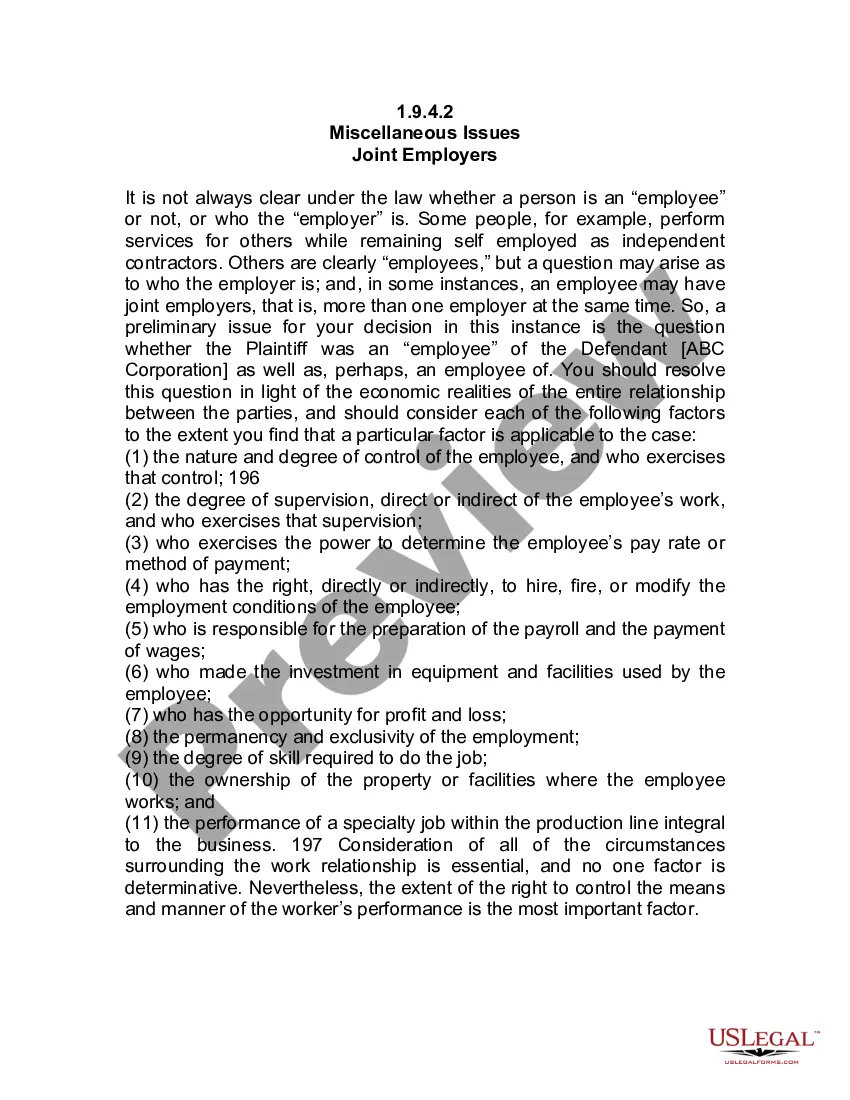

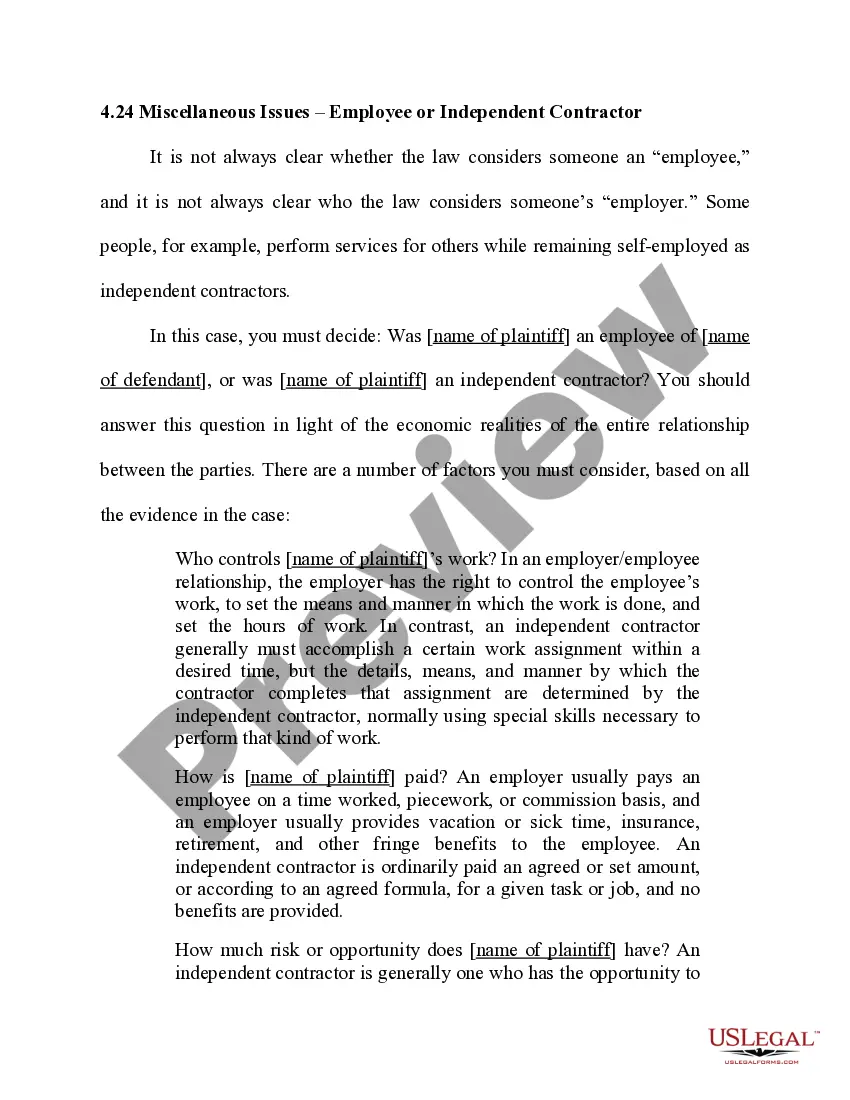

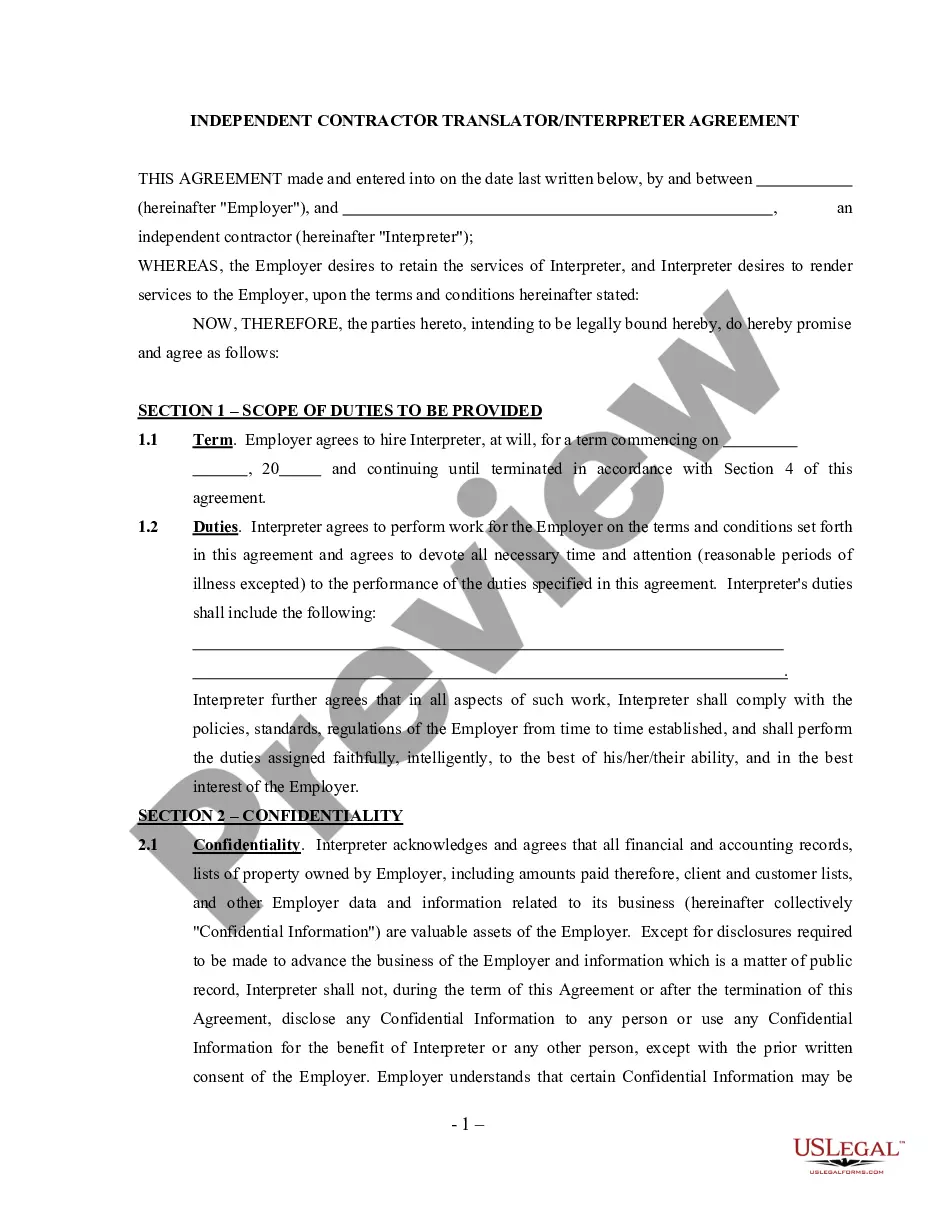

The law further states that independent contractor status is evidenced if the worker: (1) has a substantial investment in the business other than personal services, (2) purports to be in business for himself or herself, (3) receives compensation by project rather than by time, (4) has control over the time and place ...

As an independent contractor, you're the boss of your own taxes. This means there's no employer to withhold taxes for you. The T2125 form. You'll want to become good friends with the T2125 tax form: It's the form you'll use to report your business income and expenses.

The general rule is that an individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done. If you are an independent contractor, then you are self-employed.

Usually, employees will not have any financial risk as any expenses will be reimbursed, and they will not have fixed ongoing costs. Self-employed individuals, on the other hand, can have financial risk and incur losses because they usually pay fixed monthly costs even if work is not currently being done.