Georgia Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself

Description

How to fill out Notice Of Violation Of Fair Debt Act - Creditor Misrepresented Himself?

Finding the appropriate legal document template can be a challenge. Of course, there are numerous templates available online, but how do you obtain the legal form you require.

Utilize the US Legal Forms website. The platform offers countless templates, such as the Georgia Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself, which you can use for business and personal needs. All documents are reviewed by experts and meet federal and state requirements.

If you are already registered, Log Into your account and click the Download button to obtain the Georgia Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself. Use your account to browse the legal documents you have previously purchased. Visit the My documents tab in your account to retrieve another copy of the document you need.

Select the document format and download the legal document template for your device. Finally, complete, modify, print, and sign the received Georgia Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself. US Legal Forms is the largest collection of legal documents where you can access a variety of document templates. Use the service to obtain professionally crafted documents that comply with state regulations.

- Firstly, ensure you have selected the correct form for your region/area.

- You can view the form using the Review button and read the form description to ensure it is suitable for you.

- If the form does not meet your needs, take advantage of the Search field to find the right form.

- Once you are confident that the form is appropriate, click the Get now button to acquire the form.

- Choose the pricing plan you prefer and fill in the necessary information.

- Create your account and pay for the order using your PayPal account or credit card.

Form popularity

FAQ

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.

Your credit card debt, auto loans, medical bills, student loans, mortgage, and other household debts are covered under the FDCPA.

Among the insider tips, Ulzheimer shared with the audience was this: if you are being pursued by debt collectors, you can stop them from calling you ever again by telling them '11-word phrase'. This simple idea was later advertised as an '11-word phrase to stop debt collectors'.

Statute of Limitations and Your Credit ReportCollection accounts can remain on your report for seven years and 180 days from the original delinquency. Depending on the type of account and your location, this can be more than or less than the statute of limitations.

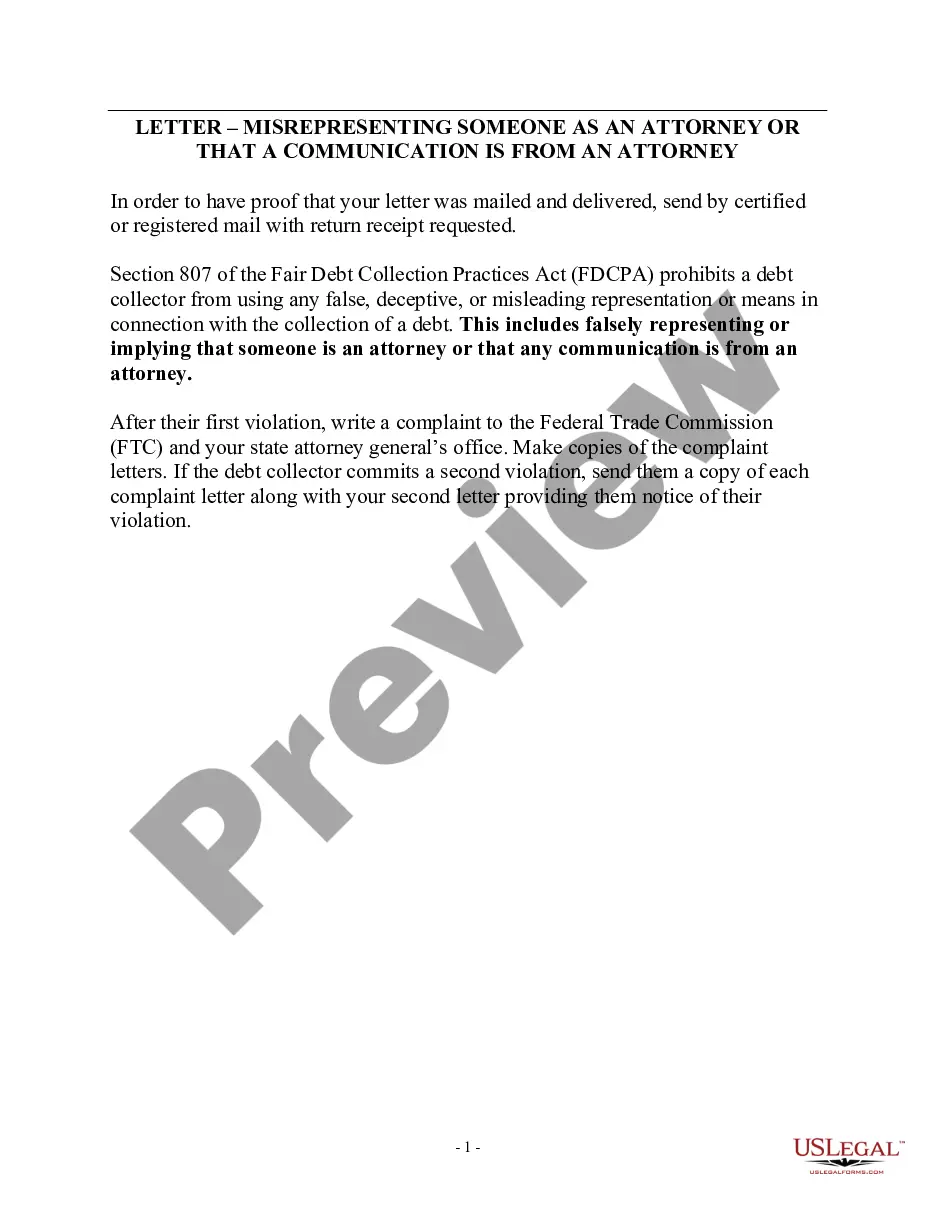

The Fair Debt Collection Practices Act (FDCPA) The FDCPA prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

The time limit is sometimes called the limitation period. For most debts, the time limit is 6 years since you last wrote to them or made a payment. The time limit is longer for mortgage debts.

Most debts in Georgia have a statute of limitations of four years, like medical debt, credit card debt and auto loans. Mortgages have a slightly longer statute of limitations of six years, and any debt you may owe to your state for tax purposes has a statute of limitations of seven years.

In most cases, the statute of limitations for a debt will have passed after 10 years. This means a debt collector may still attempt to pursue it (and you technically do still owe it), but they can't typically take legal action against you.

They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.