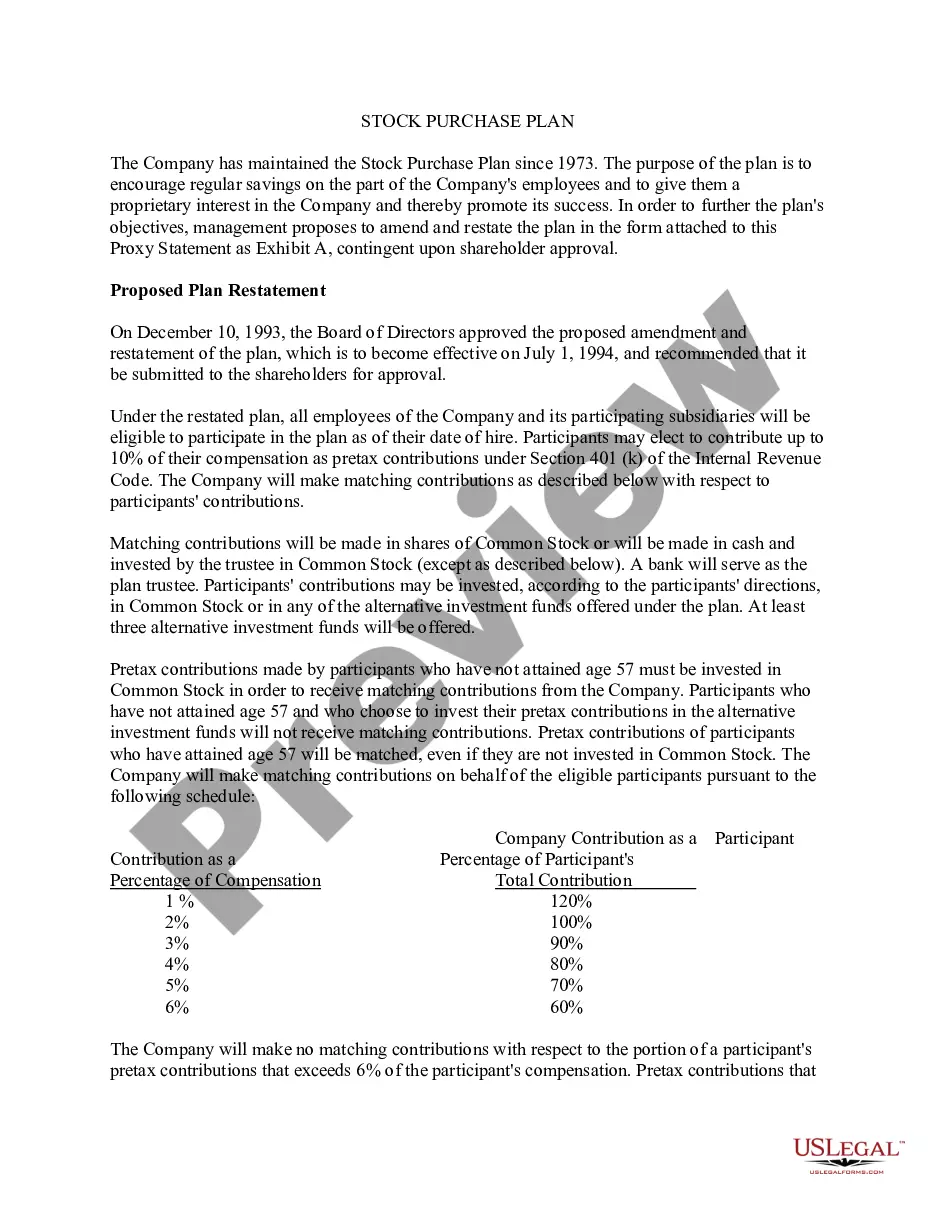

19-179 19-179 . . . Employee Stock Purchase Plan under which each employee of corporation and its wholly-owned direct or indirect, domestic and foreign subsidiaries that have authorized participation in Plan (Participating Company) can contribute up to 15% of earnings through payroll deductions and Participating Company contributes a cash amount equal to 5% of participant's payroll deductions for first year of participation, additional 7% for second year, additional 10% for third year, additional 13% for fourth year and additional 15% for fifth year. Custodian of plan purchases shares of common stock on open market or from corporation at current market prices, using payroll deductions and applicable matching Company contributions

Connecticut Amended and Restated Employee Stock Purchase Plan

Category:

State:

Multi-State

Control #:

US-CC-19-179

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Amended And Restated Employee Stock Purchase Plan?

You can commit time on-line searching for the legitimate document format which fits the federal and state needs you require. US Legal Forms provides a huge number of legitimate forms which are evaluated by experts. You can easily obtain or print out the Connecticut Amended and Restated Employee Stock Purchase Plan from my service.

If you currently have a US Legal Forms accounts, you may log in and then click the Download key. Next, you may total, edit, print out, or indication the Connecticut Amended and Restated Employee Stock Purchase Plan. Every single legitimate document format you purchase is the one you have permanently. To have one more version of the bought form, check out the My Forms tab and then click the corresponding key.

If you are using the US Legal Forms internet site the first time, follow the basic recommendations under:

- Initial, make certain you have selected the best document format for your region/town of your choice. See the form description to make sure you have selected the right form. If available, utilize the Preview key to look through the document format also.

- If you would like get one more edition in the form, utilize the Search industry to discover the format that meets your requirements and needs.

- When you have located the format you desire, just click Buy now to move forward.

- Find the rates program you desire, type in your qualifications, and register for a free account on US Legal Forms.

- Complete the financial transaction. You may use your bank card or PayPal accounts to fund the legitimate form.

- Find the formatting in the document and obtain it in your gadget.

- Make alterations in your document if required. You can total, edit and indication and print out Connecticut Amended and Restated Employee Stock Purchase Plan.

Download and print out a huge number of document web templates making use of the US Legal Forms web site, which offers the largest selection of legitimate forms. Use professional and express-particular web templates to handle your business or personal requirements.

Form popularity

FAQ

If you are risk-averse, you might consider selling your ESPP shares right away so you don't have overexposure in one stock, particularly that of your own employer. ESPP shares can put you in an overexposed position. If the stock value goes down, you may suffer losses and in extreme cases, even lose your job.

If you leave your company while enrolled in their employee stock purchase program, your eligibility for the plan ends, but you will continue to own the stock the company purchased for you during employment. The company will no longer purchase shares on your behalf after your termination date.

A: Yes. You may withdraw from the ESPP by notifying Fidelity and completing a withdrawal election. When you withdraw, all of the contributions accumulated in your account will be returned to you as soon as administratively possible and you will not be able to make any further contributions during that offering period.

In this situation, you sell your ESPP shares more than one year after purchasing them, but less than two years after the offering date. This is a disqualifying disposition because you sold the stock less than two years after the offering (grant) date.

ESPP lookback allows you to buy shares at a lower price point. An ESPP lookback allows you to purchase the share price of either A: the enrollment date (1 Jan) or B: the purchase date (30 Jun), whichever is lower.

An employee stock purchase plan (or ESPP) can be a very valuable benefit. In general, if your employer offers an ESPP, we think you should participate at the level you can comfortably afford and then sell the shares as soon as you can.

Qualifying disposition: You sold the stock at least two years after the offering (grant date) and at least one year after the exercise (purchase date). If so, a portion of the profit (the ?bargain element?) is considered compensation income (taxed at regular rates) on your Form 1040.

To get a favorable tax treatment, you have to hold the shares purchased under a Section 423 plan at least one year after the purchase date, and two years after the grant date. Q. How am I taxed in my ESPP? A.

In an ESPP with a reset feature, the look-back purchase price will "reset" if the stock price at a future purchase date is lower than the stock price on the first day of the offering period. On the date that a reset feature is triggered, the terms of the award have been modified.

Taxes on your ESPP transaction will depend on whether the sale is a qualifying disposition or not. The sale will be considered a qualifying disposition if it meets both of these criteria: You held the stocks for at least one year from the PURCHASE date. You held the stocks for at least two years from the OFFERING date.