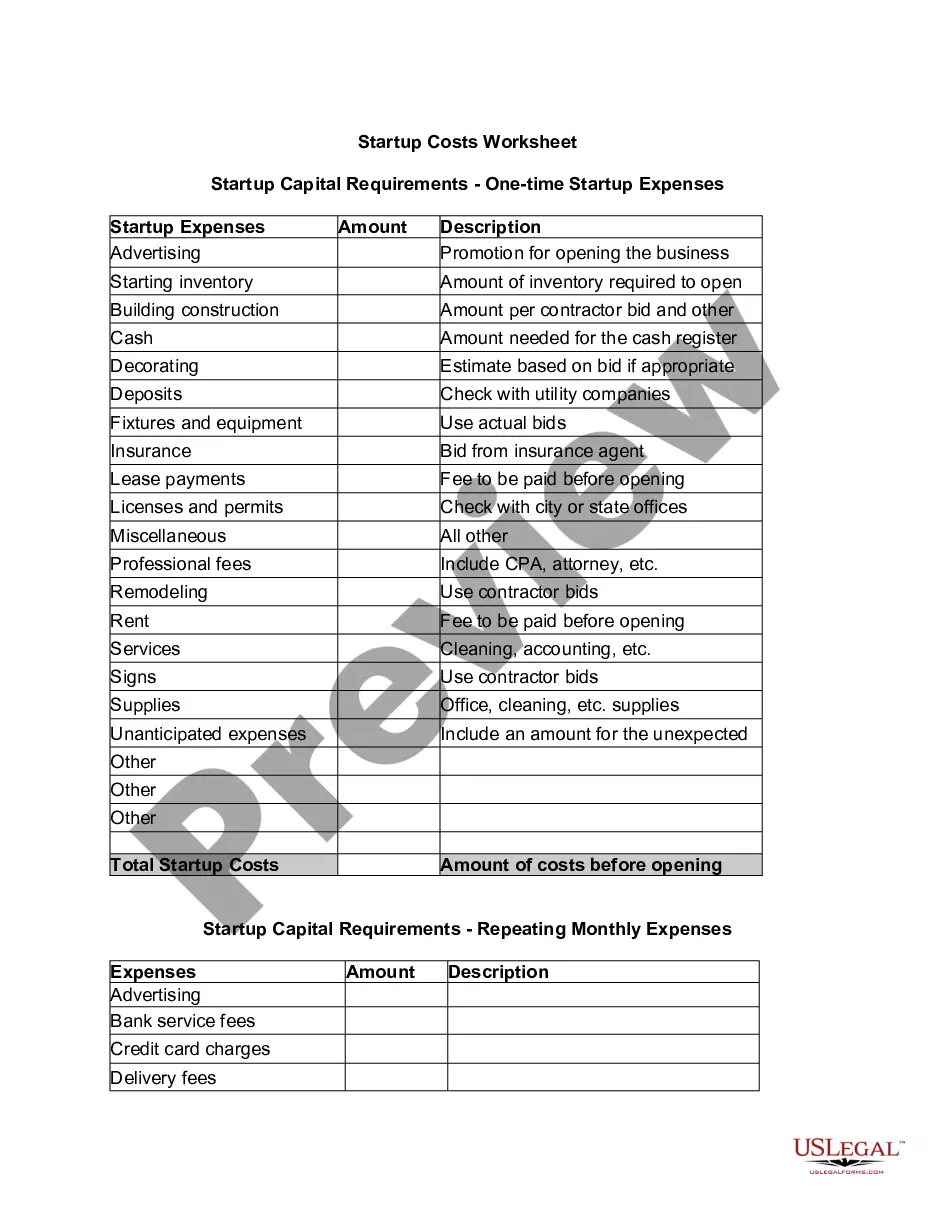

Connecticut Startup Costs Worksheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Startup Costs Worksheet?

You can invest time on the internet trying to locate the proper legal document template that meets the federal and state regulations you require.

US Legal Forms offers thousands of legal templates that have been reviewed by professionals.

It is easy to acquire or print the Connecticut Startup Costs Worksheet from my service.

If available, use the Review button to look through the document template as well. In order to find another version of the form, use the Search field to locate the template that suits your needs and requirements.

- If you already have a US Legal Forms account, you can Log In and click on the Download button.

- After that, you can complete, modify, print, or sign the Connecticut Startup Costs Worksheet.

- Every legal document template you purchase is your permanent property.

- To obtain another copy of any purchased form, go to the My documents tab and click on the relevant button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document template for the state/city of your preference.

- Review the form outline to confirm that you have chosen the right template.

Form popularity

FAQ

The IRS allows you to deduct $5,000 in business startup costs and $5,000 in organizational costs, but only if your total startup costs are $50,000 or less. If your startup costs in either area exceed $50,000, the amount of your allowable deduction will be reduced by the overage.

Start-Up Expenses are reported in aggregate - one amount equal to the total of all expenses incurred. For active business activities, these costs are entered either under Assets/Depreciation or under Business Expenses depending...

For those companies reporting under US GAAP, Financial Accounting Standards Codification 720 states that start up/organization costs should be expensed as incurred.

Key Takeaways. Startup costs are the expenses incurred during the process of creating a new business. Pre-opening startup costs include a business plan, research expenses, borrowing costs, and expenses for technology. Post-opening startup costs include advertising, promotion, and employee expenses.

Business expenses incurred during the startup phase are capped at a $5,000 deduction in the first year. This limit applies if your costs are $50,000 or less. 3fefffeff So if your startup expenses exceed $50,000, your first-year deduction is reduced by the amount over $50,000.

Under Generally Accepted Accounting Principles, you report startup costs as expenses incurred at the time you spend the money. Some of your initial expenses, such as buying equipment, are not classified as startup costs under GAAP and have to be capitalized, not expensed.

To qualify as startup costs, the costs must be ones that could be deducted as business expenses if incurred by an existing active business and must be incurred before the active business begins (Sec. 195(c)(1)).

Begin by adding up all your startup costs and costs for organizing your new business. Subtract the costs for the of $5,000 for startup costs and $5,000 for organizational costs that you can deduct in the first year.

You can enter your startup cost under the Business tab in TurboTax. In the Business Income and Expenses section click "I'll choose what I work on."

Start-Up Expenses are reported in aggregate - one amount equal to the total of all expenses incurred. For active business activities, these costs are entered either under Assets/Depreciation or under Business Expenses depending...