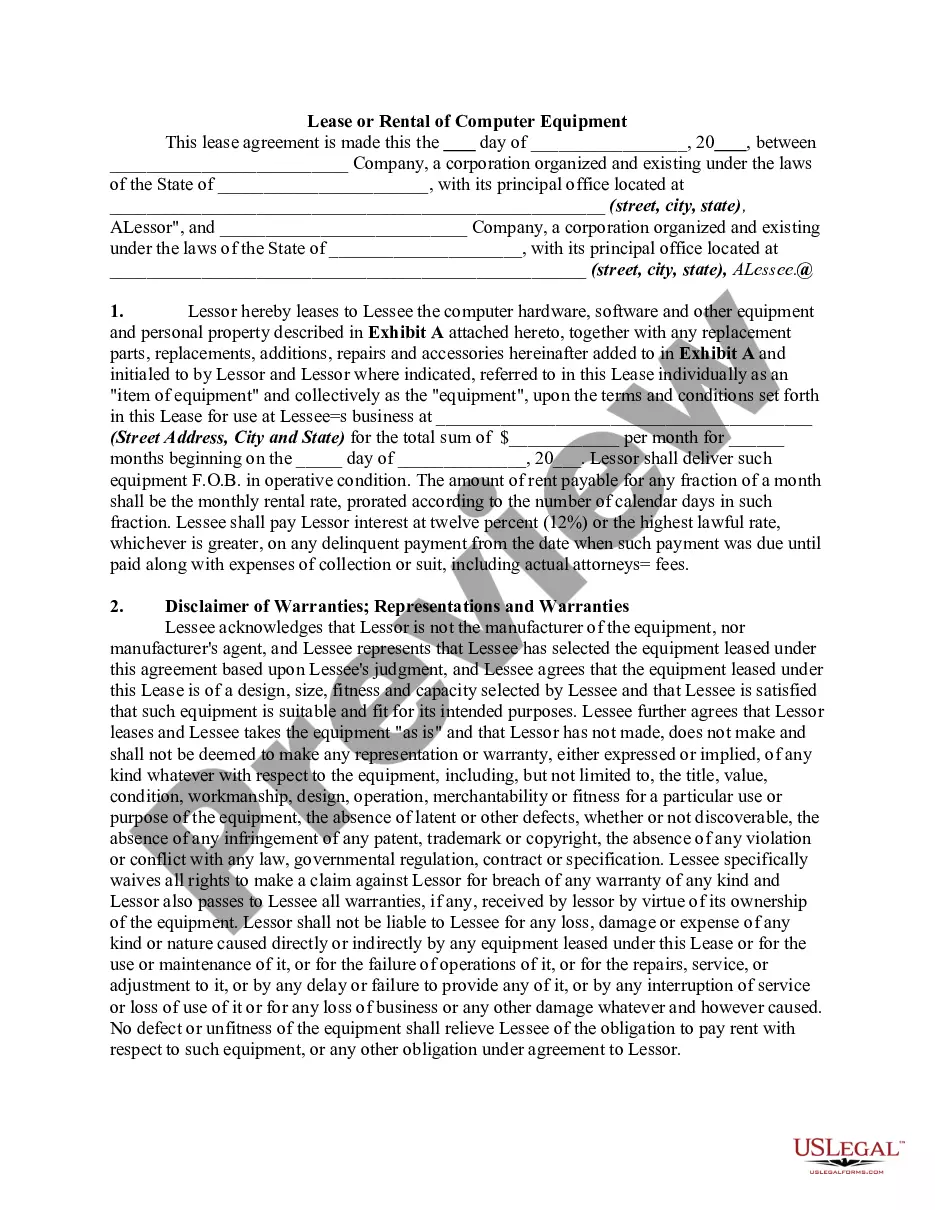

The rate of technology change is increasing, with an emphasis on client/server

technology, faster system development, and shorter life cycles. This has led to spiraling information technology (IT) budgets, driving the need for a re-evaluation of IT management issues. Organizations must find new ways to accommodate technological change. Leasing has recently emerged as a feasible, cost-effective alternative to purchasing equipment, particularly in the desktop and laptop areas.

Connecticut Guidelines for Lease vs. Purchase of Information Technology

Instant download

Description

Free preview

How to fill out Guidelines For Lease Vs. Purchase Of Information Technology?

Are you currently in a situation where you will require documentation for either business or personal matters almost every day.

There are many legal document templates available online, but finding ones you can rely on is challenging.

US Legal Forms offers thousands of template forms, such as the Connecticut Guidelines for Lease vs. Purchase of Information Technology, that are crafted to satisfy federal and state requirements.

Utilize US Legal Forms, arguably the largest collection of legal documents, to save time and avoid mistakes.

The service offers professionally crafted legal document templates that you can use for a variety of purposes. Create your account on US Legal Forms and start simplifying your life.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Next, you can download the Connecticut Guidelines for Lease vs. Purchase of Information Technology template.

- If you do not have an account and wish to use US Legal Forms, follow these instructions.

- Locate the template you need and ensure it is for your specific city/state.

- Use the Review button to examine the document.

- Read the description to confirm that you have selected the correct template.

- If the template is not what you are looking for, use the Search field to find a document that meets your requirements.

- Once you obtain the right template, click Buy now.

- Choose the pricing plan you want, fill out the necessary information to create your account, and make the payment using your PayPal or credit card.

- Select a convenient file format and download your copy.

- Access all the document templates you have purchased in the My documents section. You can download or print the Connecticut Guidelines for Lease vs. Purchase of Information Technology template whenever needed. Simply click on the desired template to download or print the document format.

Form popularity

FAQ

Section 4a 60 of the Connecticut General Statutes addresses the procurement and use of information technology resources. It outlines regulations aimed at ensuring responsible practices when leasing or purchasing technology. Leveraging these guidelines can enhance your understanding and decision-making in technology transactions.

In addition, licenses for the use of software accessed electronically are not considered sales of tangible personal property, and therefore are not subject to state sales tax, as long as no transfer of tangible personal property occurs as a part of the transaction.

Categorized as computer and data processing services, digital goods and services are currently subject to a 1 percent sales and use tax rate. As of October 1, 2019, the full Connecticut state sales tax rate of 6.35 percent will apply.

Canned or prewritten computer software is tangible personal property. The sale, leasing, or licensing of the software (including upgrades) is taxable at 6%.

Are services subject to sales tax in Connecticut? "Goods" refers to the sale of tangible personal property, which are generally taxable. "Services" refers to the sale of labor or a non-tangible benefit. In Connecticut, specified services are taxable.

Sales of canned software - delivered on tangible media are subject to sales tax in Connecticut. In the state of Connecticut, so long as no tangible personal property was delivered to the buyer in addition to downloaded software, the software will be taxed at 1% rate applicable to computer and data processing services.

If a business purchases a digital good (only digital goods, NOT digital automated services or remote access software) for business purposes, then the purchase is exempt from sales tax.

But, in most, it's a mixed bag. California exempts most software sales but taxes one type: canned software delivered on tangible personal property an actual object you can touch or hold, such as a disc. Nebraska taxes most software sales with the exception of one type: SaaS.

Several exemptions are certain types of safety gear, some types of groceries, certain types of clothing, children's car seats, children's bicycle helmets, college textbooks, compact fluorescent light bulbs, most types of medical equipment, and certain motor vehicles.

Data scanning, creating custom software, computer training, and online access to information are within the scope of taxable computer and data processing services. Computer and data processing services are subject to tax in Connecticut if the benefit of the services is received in this state.