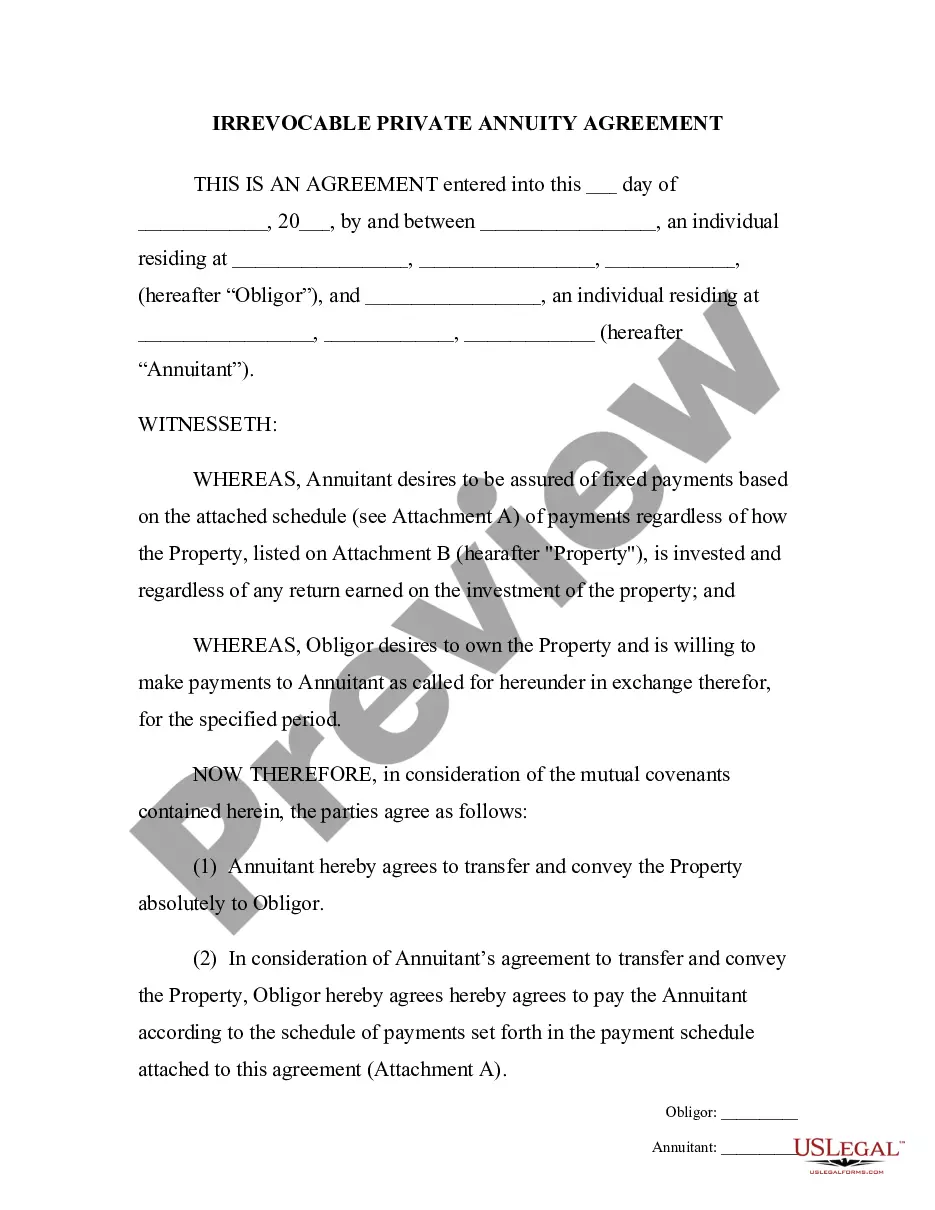

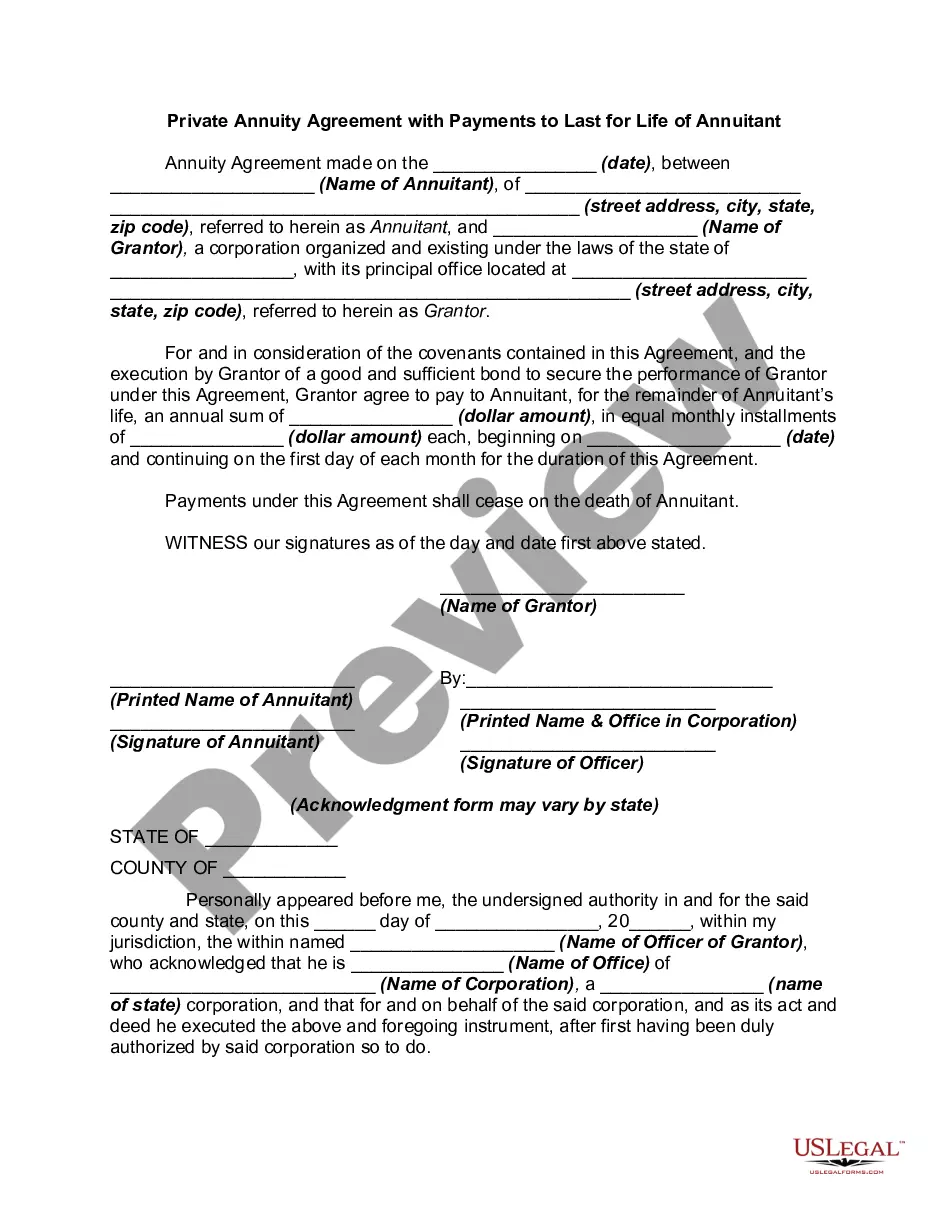

California Agreement Replacing Joint Interest with Annuity

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Agreement Replacing Joint Interest With Annuity?

Finding the appropriate legal document template can be challenging.

It goes without saying, there are numerous designs available online, but how do you obtain the legal form you require.

Utilize the US Legal Forms website. The service offers a multitude of templates, such as the California Agreement Replacing Joint Interest with Annuity, that you can utilize for both business and personal needs.

If the form does not meet your needs, use the Search field to find the appropriate form. Once you are certain that the form is suitable, click the Get now button to acquire the form. Choose the pricing plan you desire and enter the required information. Create your account and complete the purchase using your PayPal account or credit card. Select the file format and download the legal document template for your use. Once received, fill out, print, and sign the California Agreement Replacing Joint Interest with Annuity. US Legal Forms is the largest collection of legal templates where you can find various document formats. Use this service to download professionally created documents that adhere to state requirements.

- All of the documents are reviewed by professionals and comply with federal and state regulations.

- If you are currently registered, Log In to your account and click the Download button to obtain the California Agreement Replacing Joint Interest with Annuity.

- Use your account to search through the legal documents you have acquired previously.

- Visit the My documents section of your account to get another copy of the document you need.

- If you are a new user of US Legal Forms, here are simple steps to follow.

- First, ensure you have selected the correct form for your state/region. You can browse the form using the Review button and read the form details to confirm it is the right fit for you.

Form popularity

FAQ

A court issues the order and often divides retirement assets. However, if the annuity is nonqualified and taxes have already been paid on the money invested in the account, a QDRO is not required to split the annuity. Only the earnings are taxed upon withdrawal.

A life insurance policy can be exchanged for an annuity under the rules of a 1035 exchange, but you cannot exchange an annuity contract for a life insurance policy.

Life insurance and annuities have the rare advantage of being protected from most judgments and liens. While laws vary from state to state, often these insurance proceeds are considered uncollectible assets. As a matter of policy, they also bypass probate.

So what is not allowable in a 1035 exchange? Single Premium Immediate Annuities (SPIAs), Deferred Income Annuities (DIAs), and Qualified Longevity Annuity Contracts (QLACs) are not allowed because these are irrevocable income contracts.

Generally speaking, an annuity is not garnishable. There are certain kinds of income which are exempt from being seized by creditors to pay a judgment owing, and the income received from an annuity would be one of them.

Generally, the Section 1035 exchange rules allow the owner of a financial product, such as a life insurance or annuity contract, to exchange one product for another without treating the transaction as a saleno gain is recognized when the first contract is disposed of, and there is no intervening tax liability.

Jointly owned annuities are similar to annuities owned by a single person in that the death benefit is triggered by the death of one of the owners. This means that although the second owner is still alive, the annuity will pay out the death benefit to the beneficiary.

Are Annuities Protected From Creditors in California? California has asset protection laws in place to benefit residents. For unmatured life policies including annuities, the exempt amounts are $9,700 for an individual and $19,400 for a married couple. A money judgment can be enforced beyond these dollar amounts.

In some states, annuities are unconditionally exempt from seizure by creditors or bankruptcy court. States such as Florida and Texas have laws that prevent creditors from seizing any money that is held inside an annuity or cash value life insurance policy.

The California Life and Health Insurance Guarantee Association provides LIMITED PROTECTION of your life, health, and annuity benefits if, at the time your insurance company becomes insolvent, you are a California resident policyholder, or if you are the beneficiary, assignee, or payee of such policyholder regardless of