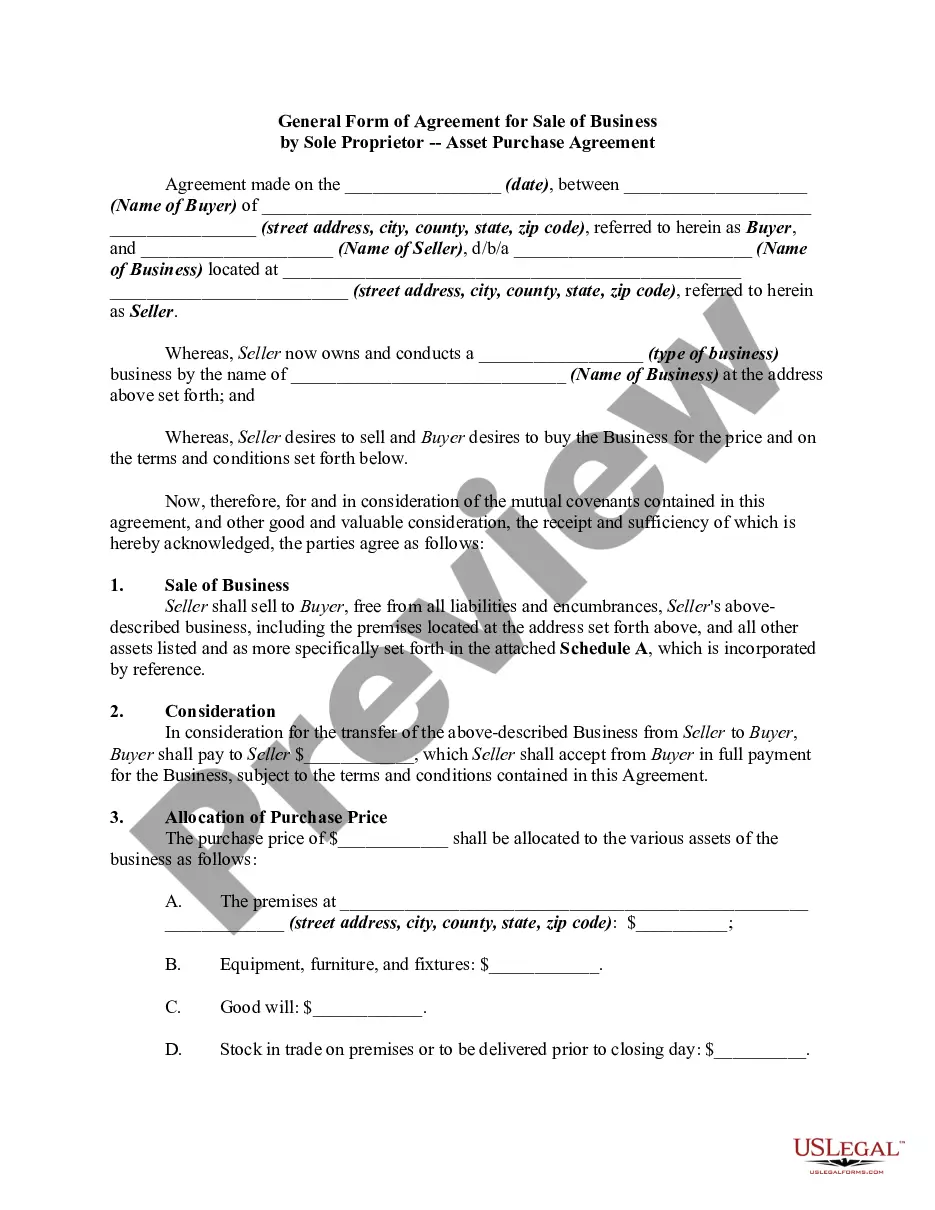

This form is an Asset Purchase Agreement. The buyer agrees to purchase from the seller certain assets which are listed in the agreement. The form also provides a listing of certain assets which will be excluded from the sale. The form must be signed in the presence of a notary public.

California Asset Purchase Agreement - Business Sale

Category:

State:

Multi-State

Control #:

US-00418

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Asset Purchase Agreement - Business Sale?

US Legal Forms - one of the largest collections of legal templates in the United States - offers a variety of legal document templates that you can download or create.

By using the website, you can access thousands of templates for business and personal use, categorized by types, states, or keywords. You can obtain the latest versions of documents like the California Asset Purchase Agreement - Business Sale in moments.

If you already possess a subscription, Log In and download the California Asset Purchase Agreement - Business Sale from the US Legal Forms repository. The Download button will be visible on every template you view. You have access to all previously saved documents in the My documents section of your account.

Select the format and download the document to your device.

Make modifications. Complete, modify, print, and sign the saved California Asset Purchase Agreement - Business Sale. Each template you added to your account has no expiration date and is yours indefinitely. Therefore, if you wish to download or create another version, simply visit the My documents section and click on the template you need.

- If you wish to use US Legal Forms for the first time, below are straightforward steps to get started.

- Ensure you have selected the appropriate template for your city/region. Click the Preview button to review the document's content.

- Examine the document summary to make sure you have chosen the correct template.

- If the template does not meet your needs, utilize the Search box at the top of the screen to find one that does.

- If you are satisfied with the document, confirm your selection by clicking the Buy now button. Then, choose the pricing plan you want and provide your details to register for an account.

- Complete the transaction. Use a credit card or PayPal account to finalize the purchase.

Form popularity

FAQ

When a person liable for sales and use taxes sells his or her business or stock of goods, the Buyer must withhold a specific portion of the purchase price to pay any sales or use taxes owed by the Seller to the California State Board of Equalization ("SBE") (RTC Section 6811).

In an asset sale, sellers are subject to potentially higher taxes than in a stock sale. While intangible assets, such as goodwill, are taxed at capital gains rates, other hard assets may be taxed at higher ordinary income tax rates. Currently, federal capital gains rates are around 20%, while state rates vary.

An asset sale involves the purchase of some or all of the assets owned by a company. Examples of common assets which are sold include; plant and equipment, land, buildings, machinery, stock, goodwill, contracts, records and intellectual property (including domain names and trademarks).

The bill of sale is typically delivered as an ancillary document in an asset purchase to transfer title to tangible personal property. It does not cover intangible property (such as intellectual property rights or contract rights) or real property.

In an asset sale, a firm sells some or all of its actual assets, either tangible or intangible. The seller retains legal ownership of the company that has sold the assets but has no further recourse to the sold assets. The buyer assumes no liabilities in an asset sale.

The result reflects whether your company made a profit or took a loss on the sale of the property.Step 1: Debit the Cash Account.Step 2: Debit the Accumulated Depreciation Account.Step 3: Credit the Property's Asset Account.Step 4: Determine the Property's Book Value.Step 5: Credit or Debit the Disposal Account.

Some items are exempt from sales and use tax, including: Sales of certain food products for human consumption (many groceries) Sales to the U.S. Government. Sales of prescription medicine and certain medical devices.

In an asset purchase, Buyer and Seller allocate the purchase price to the different assets, first to tangible assets, based on fair market value, then to intangibles other than goodwill, and finally to goodwill. The Buyer takes the assets with a tax basis equal to the portion of the purchase price allocated to them.

As of October 2016, only five states in the U.S. do not impose a state sales tax. The rest have a state sales tax with California charging the most. As a retailer, it is your responsibility to file and pay the sales taxes on products you sell within the state although most retailers simply charge it to the customer.

An asset purchase agreement is an agreement between a buyer and a seller to purchase property, like business assets or real property, either on their own or as part of a merger-acquisition.