Arizona MHA Request for Short Sale

Description

How to fill out MHA Request For Short Sale?

You can spend countless hours online searching for the valid document template that meets the state and federal requirements you need.

US Legal Forms offers thousands of valid templates that have been reviewed by experts.

You can download or print the Arizona MHA Request for Short Sale from their service.

If available, utilize the Preview button to review the document template as well.

- If you own a US Legal Forms account, you can Log In and click the Obtain button.

- Following that, you can complete, edit, print, or sign the Arizona MHA Request for Short Sale.

- Every legal document template you purchase is yours to keep indefinitely.

- To get an additional copy of any purchased form, go to the My documents tab and click the corresponding button.

- If you are using the US Legal Forms site for the first time, follow the simple instructions below.

- Firstly, ensure you have chosen the correct document template for the county/city of your choice.

- Read the form description to confirm you have selected the right template.

Form popularity

FAQ

The last step in the short sale process typically involves closing the transaction, where ownership of the property is officially transferred. At this stage, you will finalize all the paperwork, including the Arizona MHA Request for Short Sale, and ensure that any outstanding liens or conditions are resolved. Once completed, you will receive confirmation that the sale has been processed, allowing you to move forward from your previous mortgage obligations. It's wise to work with professionals who can guide you through this final phase.

A short sale may impact your security clearance, but this can depend on various factors such as your overall financial stability and how you manage your debts. It's important to remember that an Arizona MHA Request for Short Sale will be viewed by security clearance agencies, as any financial distress can be a concern. However, being proactive about addressing your financial situation can demonstrate responsibility, potentially mitigating negative effects. Always consult a qualified advisor to understand the implications fully.

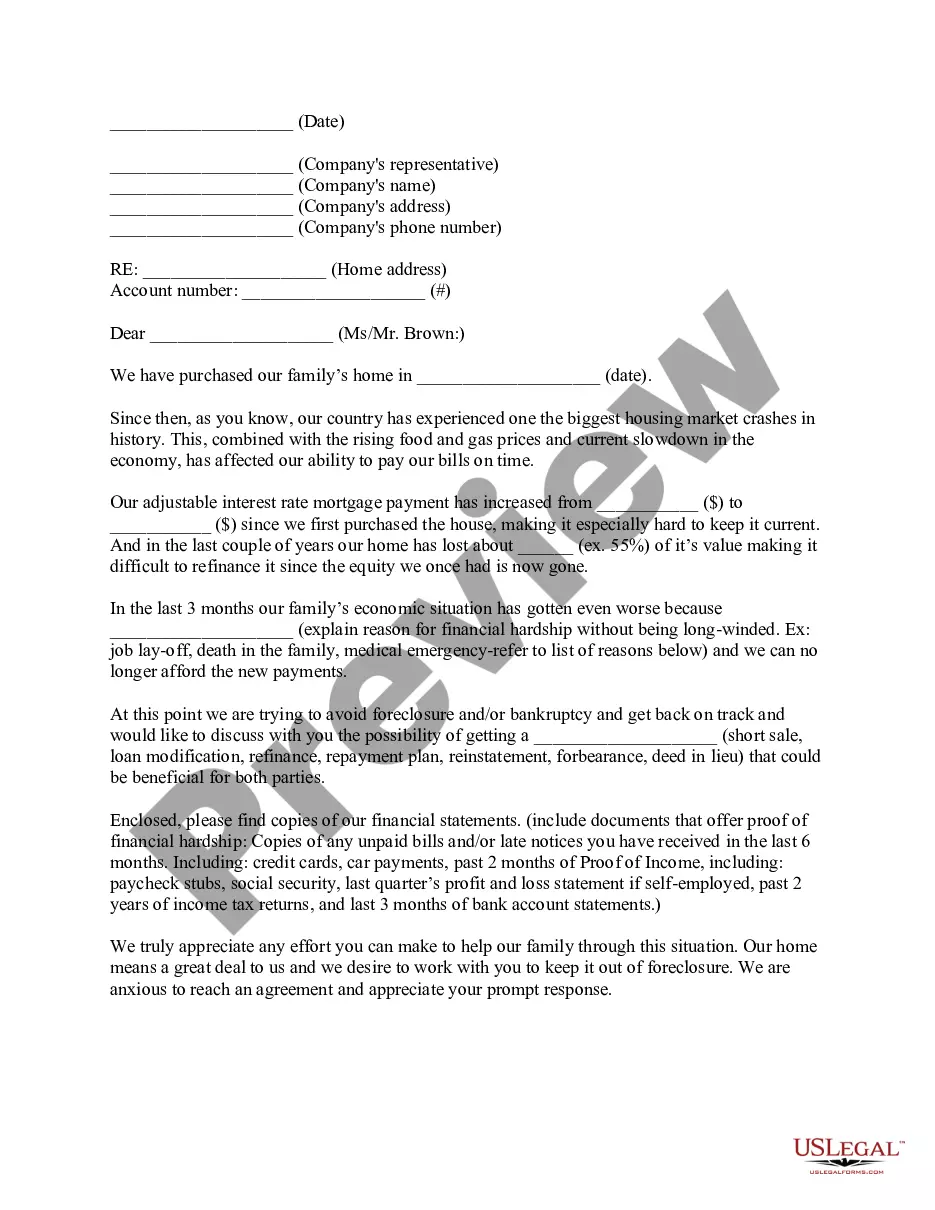

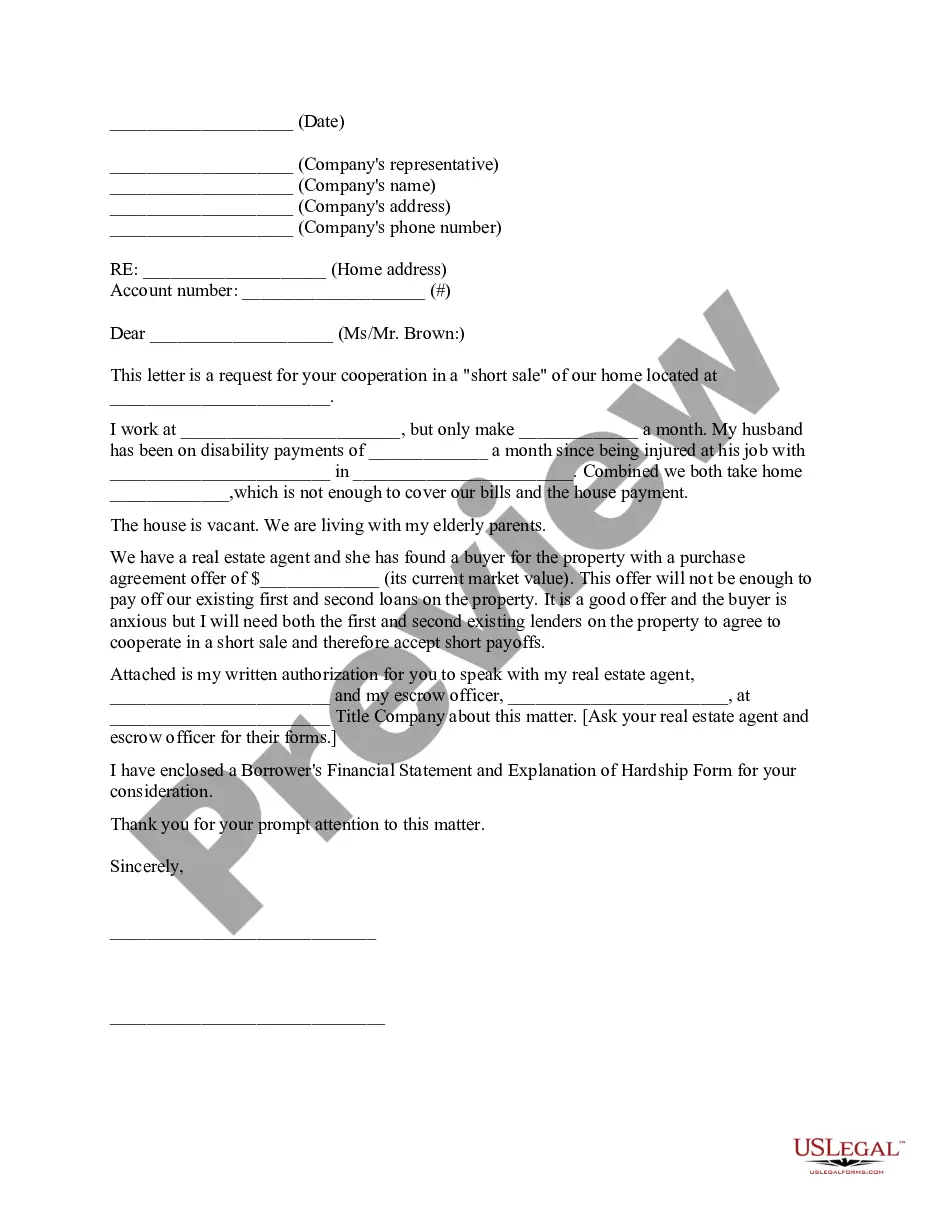

A short sale approval letter is an official document from the lender that confirms their acceptance of a short sale. This letter outlines the terms under which the sale can occur, which is essential for completing the Arizona MHA Request for Short Sale. It gives assurance to the buyer and seller that the lender agrees to let the property sell for less than the amount owed. Without this letter, proceeding with a short sale can be challenging.

A short sale in Arizona allows homeowners to sell properties for less than their outstanding mortgage balance with their lender's consent. This option can prevent foreclosure and reduce financial strain. By enabling an Arizona MHA Request for Short Sale, you open the door to a less stressful selling process. Consulting with experts familiar with Arizona's real estate might enhance your overall experience.

Offers on short sales can vary widely, but they are usually significantly lower than market value. The exact amount will depend on both the property’s condition and the amount the owner owes on the mortgage. When you prepare your Arizona MHA Request for Short Sale, it's critical to conduct thorough research to make a reasonable and appealing offer to the bank.

Requesting a short sale involves several key steps. First, gather financial documents that demonstrate your inability to meet mortgage payments. Then, work with your lender to submit an Arizona MHA Request for Short Sale, including an offer from a potential buyer. It’s recommended to engage a real estate expert to navigate this process effectively.

A significant downside of a short sale is its impact on your credit score, although it is generally less severe than a foreclosure. It may also take a considerable amount of time to complete the process, often leading to stress for homeowners. Furthermore, the bank might tax you on the forgiven debt. Thus, it’s crucial to weigh these factors carefully against your situation before submitting an Arizona MHA Request for Short Sale.

Homeowners experiencing financial difficulties typically qualify for a short sale. Factors such as job loss, medical expenses, or divorce can all contribute to an individual's eligibility. The bank will review these hardships through your Arizona MHA Request for Short Sale to determine if you meet their criteria. Ensuring all documentation is complete and accurate is critical during this request.

In Arizona, a short sale allows homeowners to sell their property for less than what they owe on their mortgage with the bank's approval. The lender agrees to accept the reduced amount to avoid the costs associated with foreclosure. It's essential to follow the proper steps, including submitting an Arizona MHA Request for Short Sale, to facilitate this process. Engaging with real estate professionals can significantly enhance the chance of a successful outcome.

A bank may deny a short sale for several reasons. For instance, if the offer does not meet the bank's expectations for the property's value, they might refuse the request. Additionally, if the homeowner does not demonstrate financial hardship or if there are discrepancies in documentation, the bank may also decline. Understanding this process is key when pursuing an Arizona MHA Request for Short Sale.