Arizona Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading

Description

How to fill out Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading?

Are you presently inside a place in which you need documents for either company or person uses nearly every working day? There are a variety of authorized file templates available on the Internet, but locating versions you can rely isn`t simple. US Legal Forms offers 1000s of develop templates, such as the Arizona Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading, that are published to satisfy state and federal demands.

Should you be previously knowledgeable about US Legal Forms site and have a merchant account, simply log in. After that, you may obtain the Arizona Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading format.

Should you not offer an bank account and wish to start using US Legal Forms, adopt these measures:

- Discover the develop you want and make sure it is for the proper city/state.

- Make use of the Review option to review the shape.

- See the explanation to actually have chosen the correct develop.

- In case the develop isn`t what you are trying to find, take advantage of the Research discipline to obtain the develop that suits you and demands.

- Once you find the proper develop, click on Purchase now.

- Choose the pricing strategy you need, fill out the desired info to produce your money, and buy an order using your PayPal or credit card.

- Pick a practical data file format and obtain your duplicate.

Locate each of the file templates you may have bought in the My Forms food list. You can obtain a more duplicate of Arizona Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading anytime, if necessary. Just select the essential develop to obtain or produce the file format.

Use US Legal Forms, by far the most extensive selection of authorized varieties, to save some time and stay away from mistakes. The support offers appropriately produced authorized file templates that you can use for an array of uses. Produce a merchant account on US Legal Forms and start creating your lifestyle easier.

Form popularity

FAQ

A Rule 10b-5 disclosure letter is a letter from lawyers confirming that they have undertaken certain due diligence procedures and that, on the basis of such procedures, have no reason to believe that an offering document contains an untrue statement of material fact or omits to state a material fact necessary in order ...

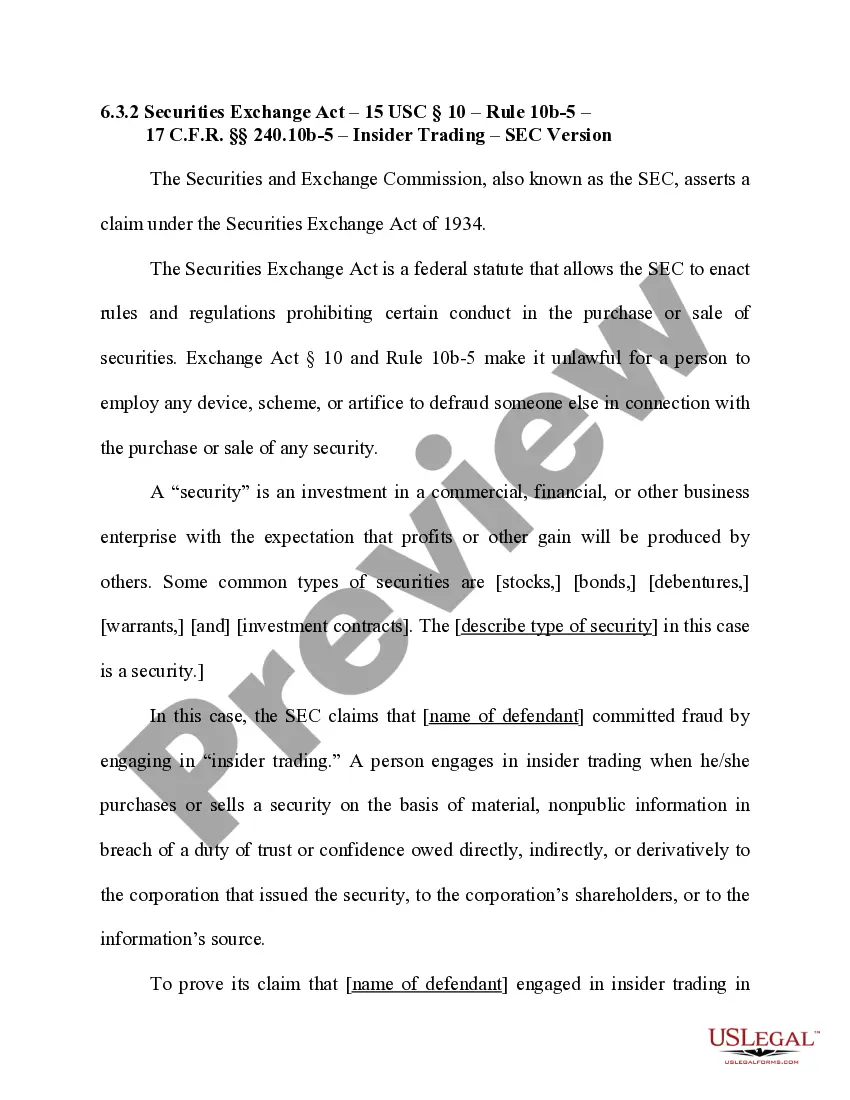

Rule 10b-5 covers insider trading, which occurs when confidential information is used to manipulate the market in one's favor. Changes to Rule 10b5-1, outlining ways for insiders to proactively avoid the appearance of insider trading, took effect on Feb. 27, 2023.

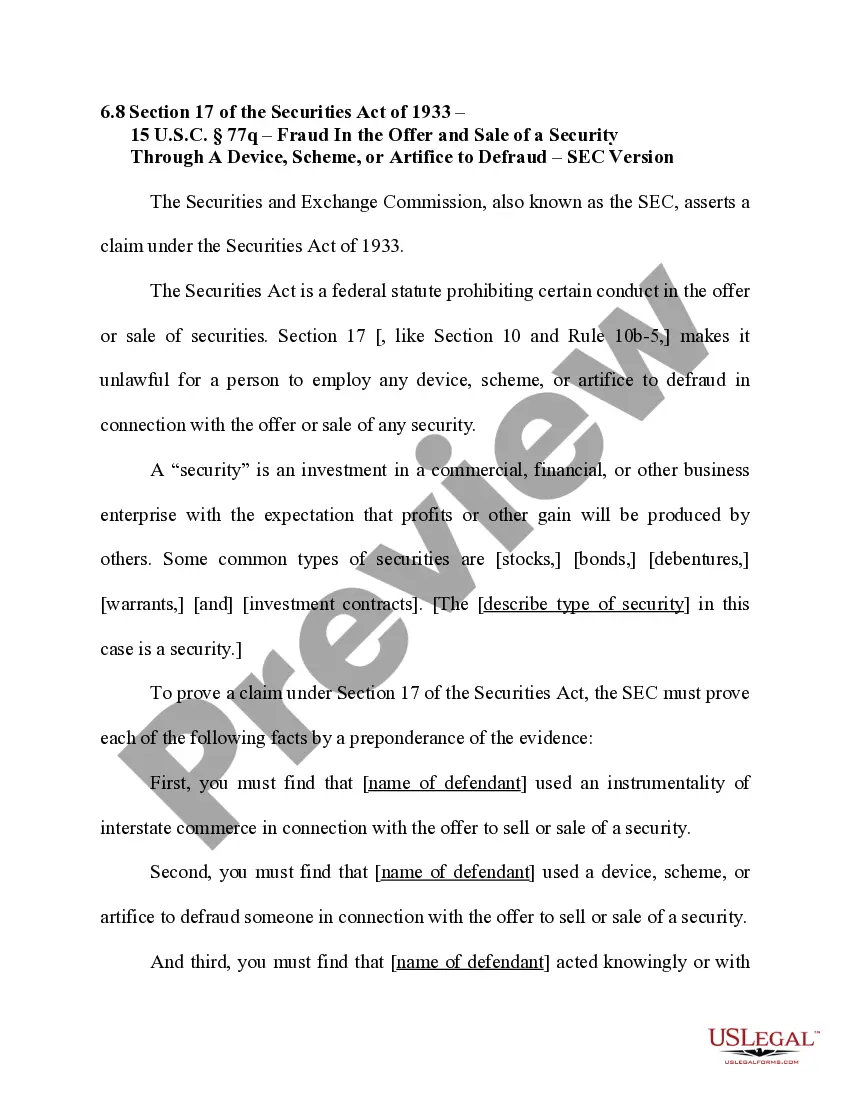

The rule renders it unlawful, in connection with the purchase or sale of any security, to: Employ any device, scheme, or artifice to defraud; Make any untrue statement of a material fact or to omit to state a material fact necessary in order to make the statements made not misleading; or.

Section 10(b) of the Exchange Act and Rule 10b-5 prohibit material misrepresentations and misleading omissions in connection with the purchase or sale of securities. To prove a violation of Section 10(b) of the Exchange Act and Rule 10b-5 thereunder, the Commission must prove that the defendants acted with scienter.

SEC Rule 10b-5, states that it is illegal for any person to defraud or deceive someone, including through the misrepresentation of material information, with respect to the sale or purchase of a security.

Rule 10b-5, adopted pursuant to section 10(b), prohibits fraudulent devices and schemes, material misstatements and omissions of any material facts, and acts and practices that operate as a fraud or deceit on any person in connection with the purchase or sale of a security.

Section 10(b) of the Exchange Act and Rule 10b-5 prohibit material misrepresentations and misleading omissions in connection with the purchase or sale of securities.

Rule 10b5-1 allows insiders to sell company stock by setting up a predetermined plan that specifies in advance the share price, amount, and transaction date. The insider selling the stock and the broker carrying out the transaction must certify that they are not aware of any material nonpublic information (MNPI).