Arizona Notice to Debtor

What is this form?

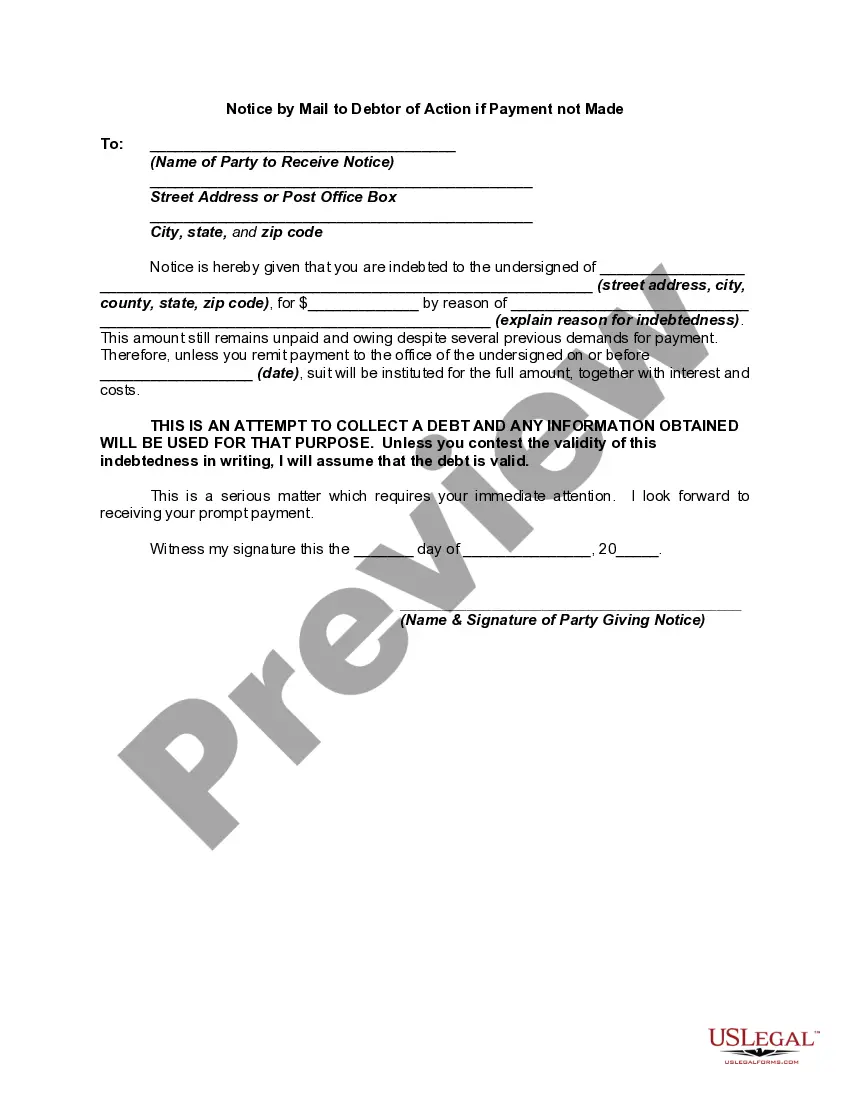

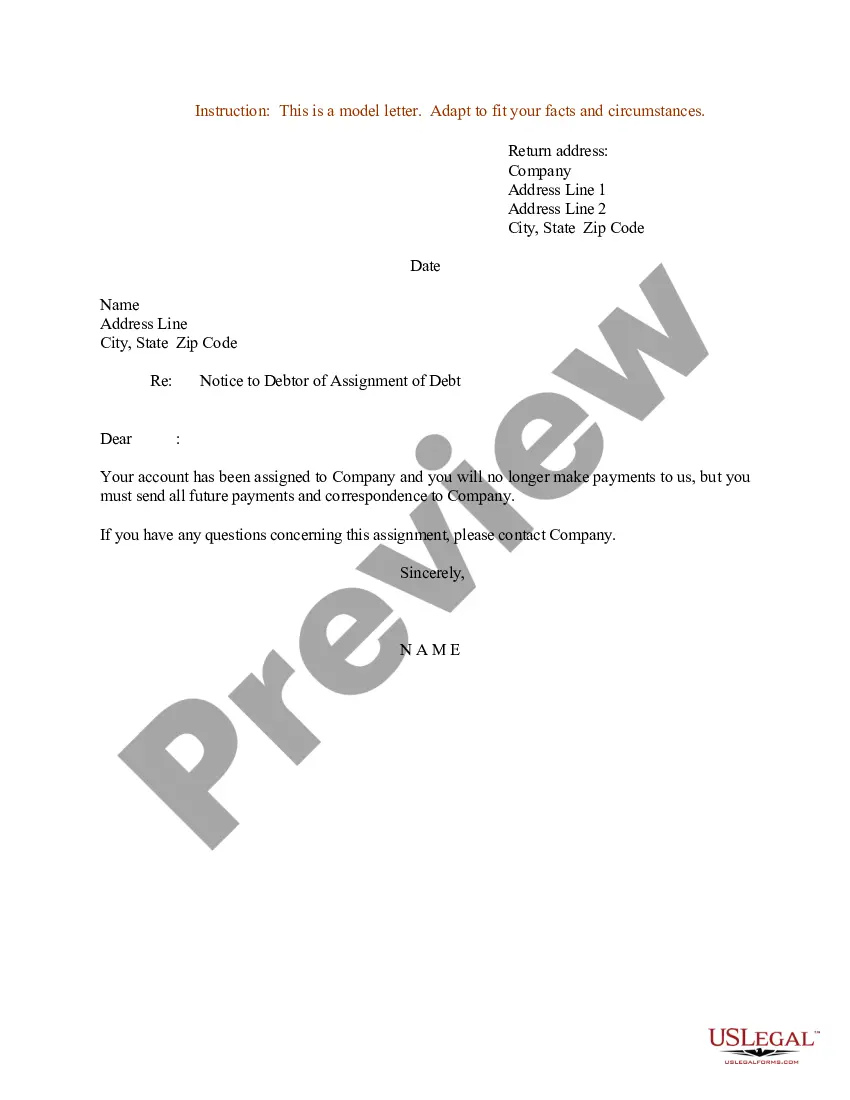

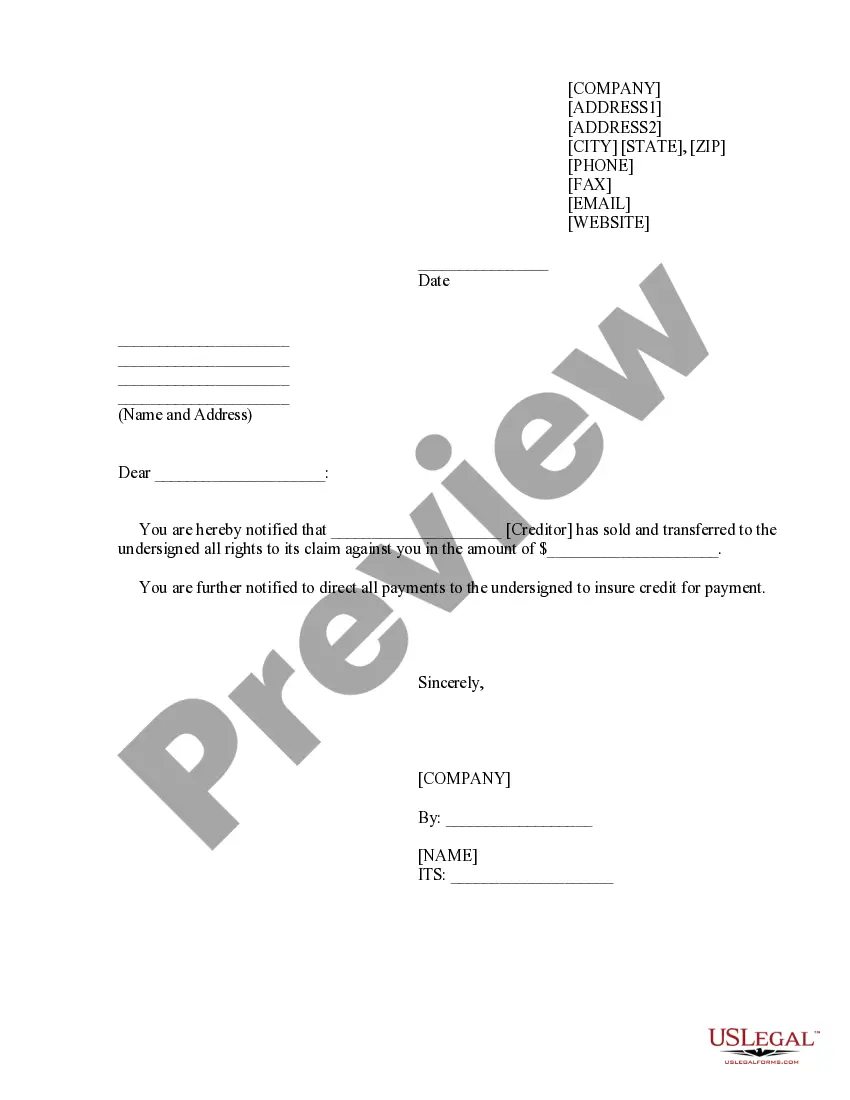

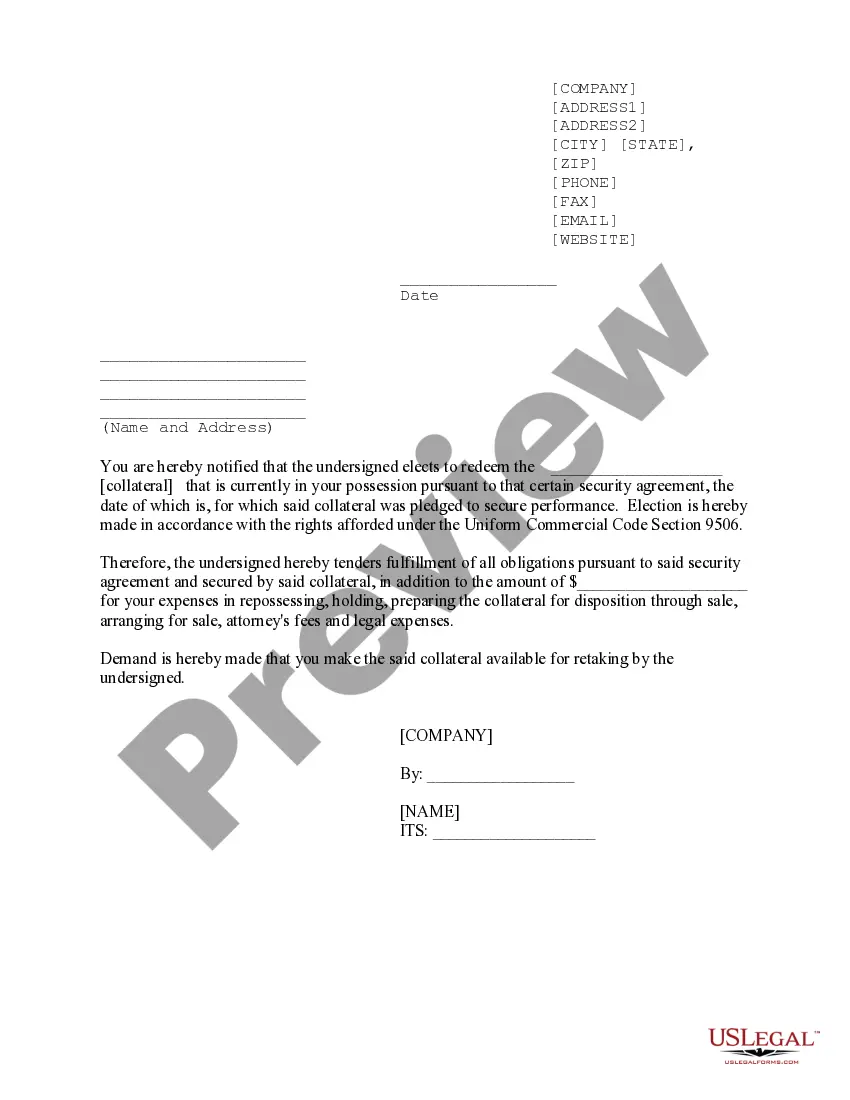

A Notice to Debtor is a legal document that serves to notify a debtor about important information regarding a debt obligation. This form is essential in ensuring that the debtor is formally informed about the assignment of a debt, which can help prevent delays in collections or disputes. It is particularly important for maintaining clear communication between the creditor and debtor, differing from other notices by specifically addressing assignments and payment demands.

What’s included in this form

- Debtor and Assignee details, including names and addresses

- Reference to the original security agreement and financing statement

- Notification of assignment of rights to the assignee

- Demand for payment, including amounts and commencement date

- Execution section for signatures of the assignor and assignee

Common use cases

This form should be used when a creditor has assigned their rights under a security agreement to another party (the assignee). It is used to formally inform the debtor of this assignment, thereby clarifying whom the debtor should make payments to. Scenarios include the transfer of debt obligations in business transactions, loan assignments, or other financial agreements where formal notification is required.

Who should use this form

- Creditors looking to assign debts to another party

- Assignees who need legal notice of the debt assignment

- Debtors who require clarity regarding whom to make payments

- Legal professionals managing financial agreements

How to prepare this document

- Identify the debtor and assignee by filling in their names and addresses.

- Reference the original security agreement and financing statement details, including the date.

- Clearly state the date of the assignment and include any necessary certification copies.

- Specify the payment amount and the start date for the payment obligations.

- Ensure both the assignor and assignee sign the document.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. It is advisable to check state requirements to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include complete names and addresses of the debtor and assignee.

- Not referencing the original security agreement correctly.

- Omitting the execution date or signatures.

- Leaving the payment amount or terms vague or incomplete.

Advantages of online completion

- Immediate access to a professionally drafted legal document.

- Editability allows customization based on individual circumstances.

- Cost-effective solution for legal document needs.

- Time-saving as it eliminates the need for in-person consultations.

Looking for another form?

Form popularity

FAQ

Creditors in Arizona generally have a six-year period to collect most types of debts. After this time, if the debt remains unpaid, it may become uncollectible. Using an Arizona Notice to Debtor can help you understand your standing with creditors and ensure that your rights are respected during this time frame.

The phrase to effectively stop debt collectors is, 'I do not wish to be contacted regarding this debt.' This statement can help protect you from further communication. Understanding your rights can be fortified by using the Arizona Notice to Debtor, empowering you to take control of the conversation with creditors.

To publish a notice to creditors in Arizona, you must first file the notice with the court that issued the order. Then, you should post the notice in a public place, often in a local newspaper, to notify all potential creditors of your intentions. The Arizona Notice to Debtor is vital for alerting creditors about the legal proceedings related to debts, ensuring all parties are informed.

Arizona's collections law governs how creditors can pursue debt collection. Debtors have rights that protect them from unfair practices, including harassment. Knowing how the Arizona Notice to Debtor works can help you navigate these laws effectively and ensure you are treated fairly throughout the collections process.

In Arizona, creditors can collect on a judgment for up to five years. However, creditors may file for a renewal of the judgment, extending their collection time for an additional five years. It's important to understand your rights and obligations regarding the Arizona Notice to Debtor, as it plays a crucial role in the collection process.

Creditor claims against an estate in Arizona generally must be filed within four months of the personal representative's appointment. This timeframe allows creditors to assert their rights while balancing the needs of the estate beneficiaries. Should any challenges arise, understanding the Arizona Notice to Debtor becomes essential in managing the estate’s debts appropriately. Using platforms like uslegalforms can simplify this process and ensure compliance with state laws.

Yes, a creditor can take your house in Arizona, but specific legal processes must be followed. Typically, this occurs through foreclosure if the homeowner fails to meet mortgage obligations. However, certain protections exist under Arizona law, which may allow you to keep your home even if you have debts. Familiarizing yourself with the Arizona Notice to Debtor can provide you with insights into safeguarding your property.

In Arizona, the statute of limitations defines the time frame in which creditors can enforce debts in court. Generally, this period is three to six years, depending on the type of debt. Once this period expires, creditors can lose their legal right to collect the debt through litigation. Staying informed about the Arizona Notice to Debtor helps you better understand your rights and timelines related to debt collection.

The notice sent to creditors in Arizona typically includes relevant information about the debtor’s financial status and any pending actions regarding their debt. This notice is crucial for ensuring that creditors are aware of their rights and responsibilities during the collection process. By following the Arizona Notice to Debtor guidelines, you can make sure all involved parties receive proper communication, promoting transparency.

In Arizona, certain properties are exempt from creditors to protect individuals from losing essential assets. Common exemptions include a primary residence, personal belongings, and tools required for work. Additionally, specific amounts of equity in a vehicle and retirement accounts may be protected under state law. Using the Arizona Notice to Debtor can clarify which properties you may keep safe from creditor claims.