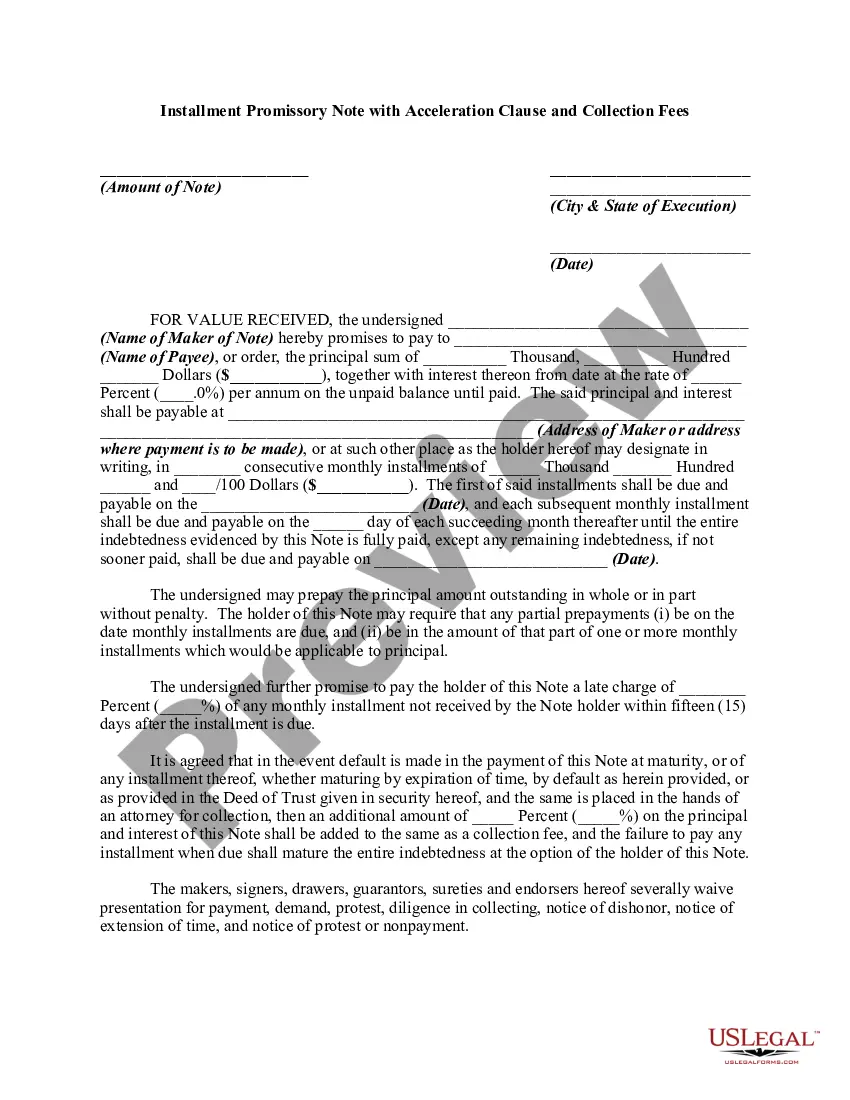

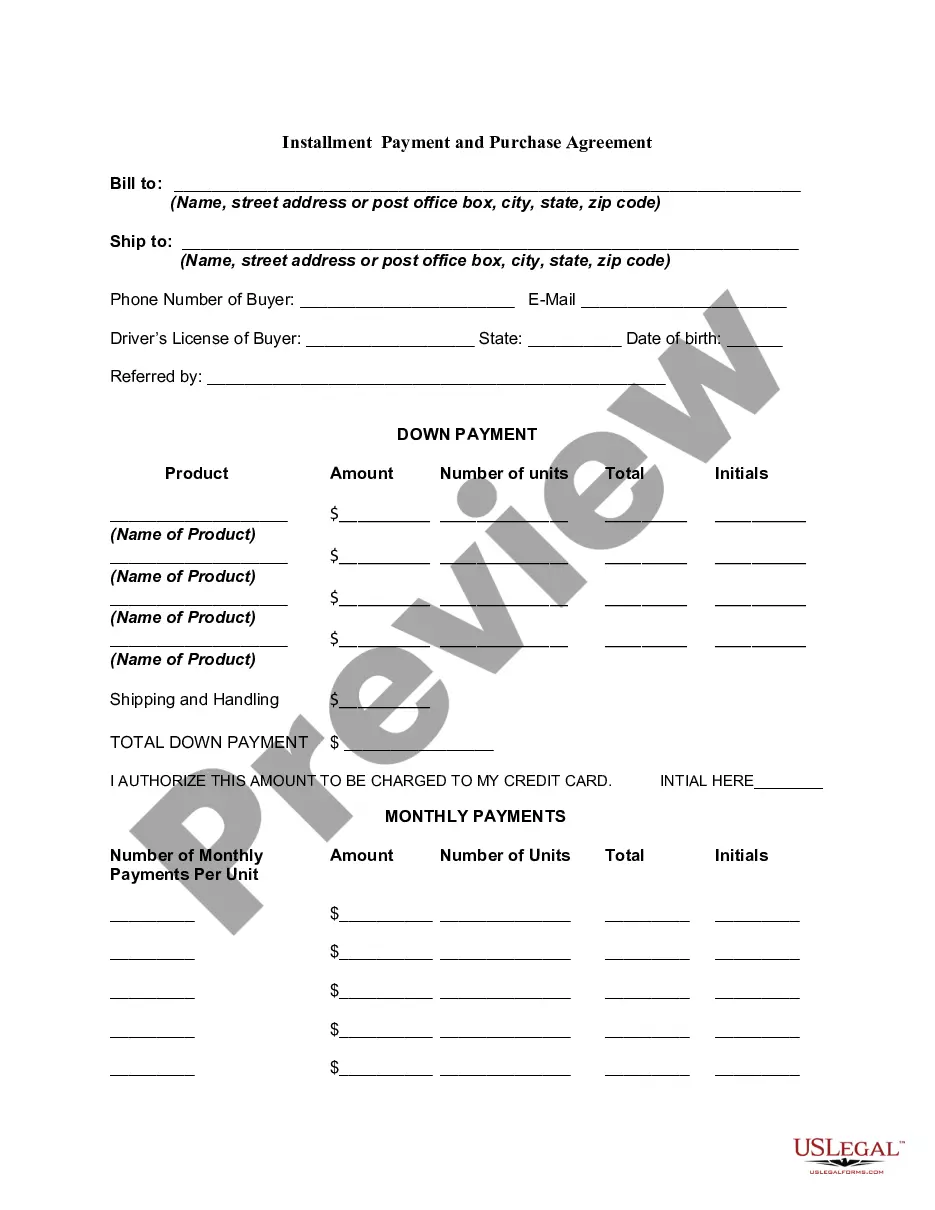

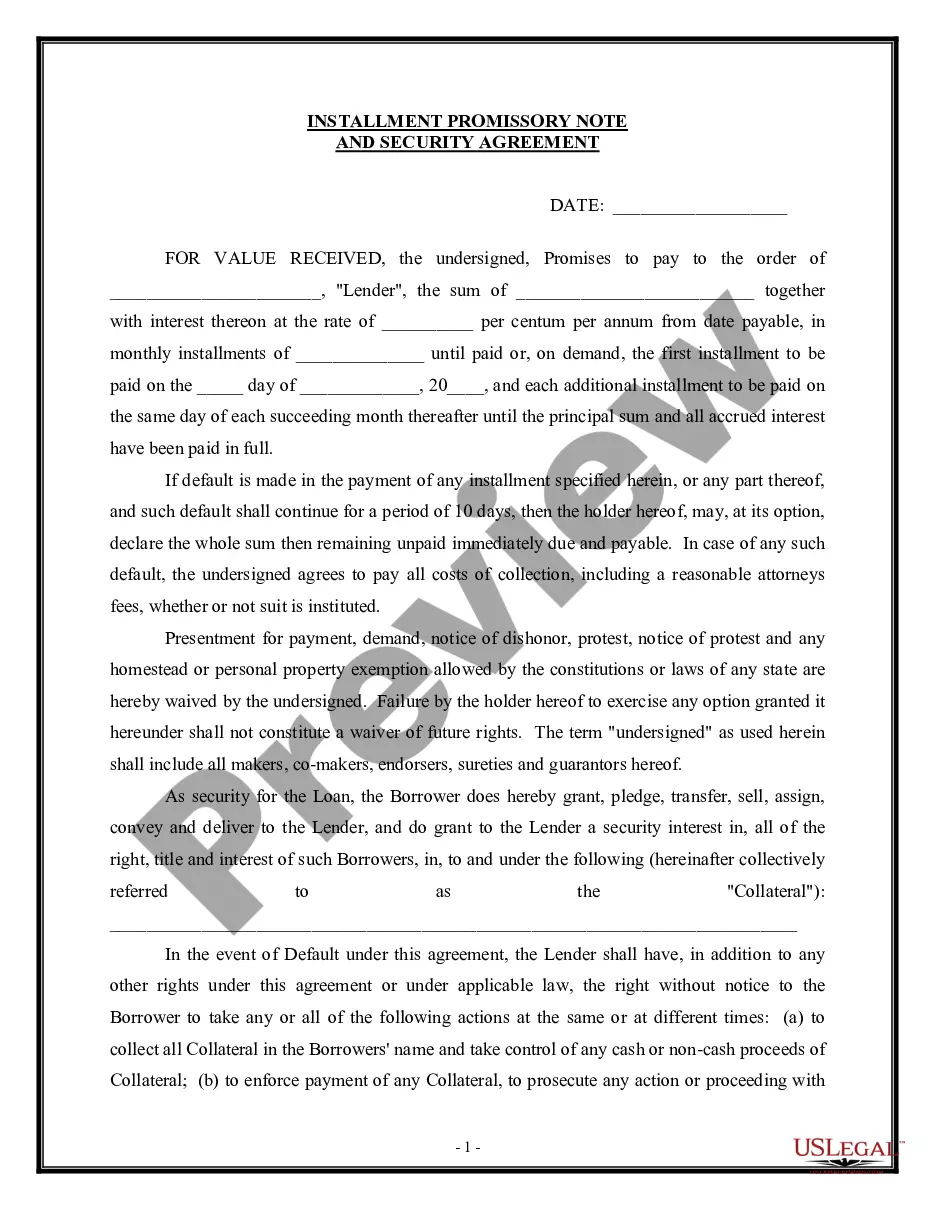

Arkansas Installment Promissory Note with Bank Deposit as Collateral

Description

How to fill out Installment Promissory Note With Bank Deposit As Collateral?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a vast array of legal form templates that you can obtain or print.

By utilizing the website, you will access thousands of forms for both business and personal purposes, organized by categories, states, or keywords.

You can find the most recent versions of forms such as the Arkansas Installment Promissory Note with Bank Deposit as Collateral within moments.

Review the form summary to ensure you have selected the right form.

If the form does not meet your requirements, use the Search field at the top of the screen to find one that does.

- If you have a monthly subscription, Log In and retrieve the Arkansas Installment Promissory Note with Bank Deposit as Collateral from the US Legal Forms library.

- The Download button will appear on every form you view.

- You can access all previously downloaded forms from the My documents tab of your account.

- If you are using US Legal Forms for the first time, here are simple instructions to help you get started.

- Ensure that you have selected the correct form for your city/state.

- Click the Preview button to examine the form's content.

Form popularity

FAQ

The document that connects the Arkansas Installment Promissory Note with Bank Deposit as Collateral is typically a security agreement. This agreement specifically outlines the terms under which the collateral, in this case, the bank deposit, secures the promissory note. By detailing the rights and responsibilities of both parties, this document ensures clarity and protection throughout the transaction. Ultimately, having clear documentation helps to enforce rights if any issues arise.

Promissory notes, including an Arkansas Installment Promissory Note with Bank Deposit as Collateral, can indeed be backed by collateral. This security feature helps mitigate the risk for lenders since they can claim the collateral if the borrower fails to repay. This structure not only protects the lender's interests but may also allow borrowers to secure lower interest rates. Understanding the implications of collateral is vital when negotiating any promissory note agreement.

Indeed, promissory notes can be backed by collateral, making an Arkansas Installment Promissory Note with Bank Deposit as Collateral a solid financial choice. The collateral may include bank deposits, real estate, or other valuable assets that the lender can seize if the borrower fails to repay. By having collateral, the lender minimizes risk, while borrowers may secure better terms for their loans. This mutual benefit improves financial relationships.

Yes, a promissory note can be secured by real property, including in the case of an Arkansas Installment Promissory Note with Bank Deposit as Collateral. This arrangement provides added security for the lender, ensuring their investment is backed by tangible assets. The borrower agrees that the property can be claimed if payment obligations are not met. This security element enhances the trust between both parties.

To secure an Arkansas Installment Promissory Note with Bank Deposit as Collateral, it's essential to create a lien on the property. This process involves recording the note with the appropriate governmental body, establishing the lender's legal claim to the property. By doing this, the lender's investment gains protection. Therefore, if the borrower defaults, the lender can pursue foreclosure on the property.

The owner must be aware that the earnest money deposit will be made in the form of a promissory note (i.e., not in cash) before it accepts the purchase offer. This fact must also be stated clearly in the purchase agreement itself.

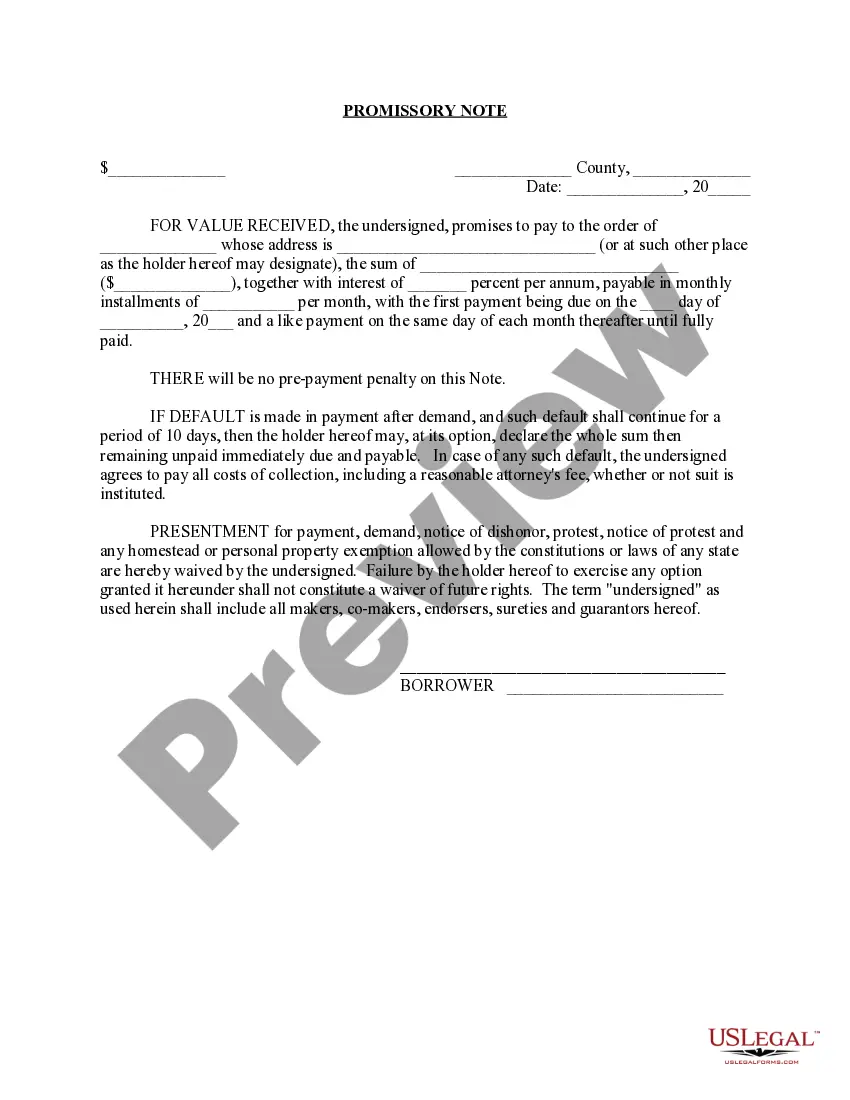

A promissory note is a contract that spells out the terms of a loan. It reduces misunderstandings and provides a legal remedy if the borrower doesn't pay or the lender oversteps its rights. If you're borrowing or lending money, you should consider having oneyou can write one either as the borrower or the lender.

Financial institutions such as banks and lenders often use promissory notes when issuing real estate mortgage loans or student loans. Companies or individuals also use promissory notes when issuing or taking on personal loans or corporate loans.

Let's get straight into it! Banks are under no legal requirement to accept promissory notes. Remember that laws can fluctuate from state to state, so it's always best to check directly with your local bank or a legal professional in your region.

Promissory notes legally bind the borrower and lender in an agreement where the borrower is responsible for paying back a loan or debt. They lay out the conditions of the loan and detail the time frame for paying back the loan as well as any interest that might accrue over the life of the loan.