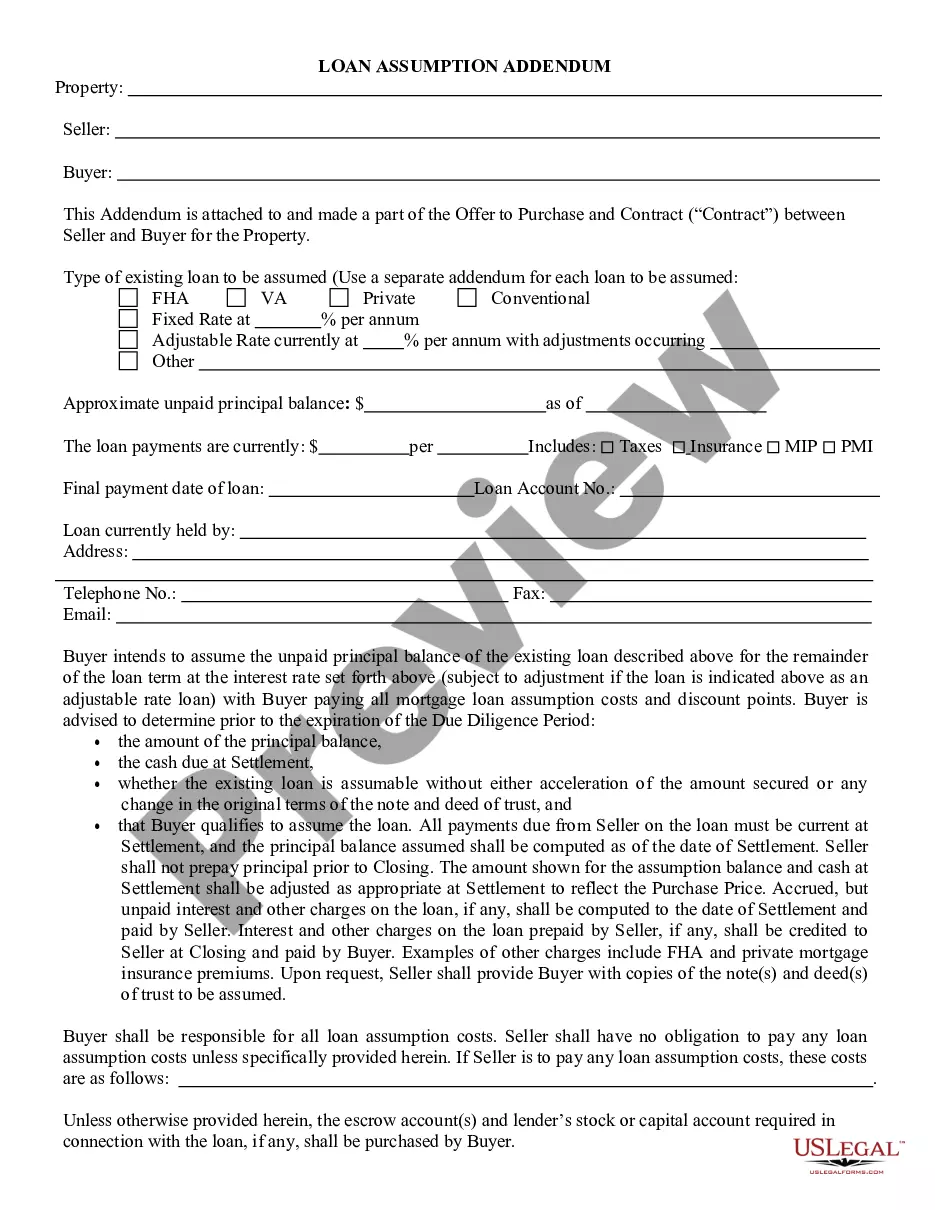

This form is an Assumption Agreement. The grantor desires to convey certain property to the grantee and the grantee agrees to assume the lien and the loan. The agreement must also be signed in the presence of a notary public.

Arkansas Loan Assumption Agreement

Category:

State:

Multi-State

Control #:

US-00561

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Assumption Agreement?

Locating the appropriate legal document template can pose a significant challenge.

Certainly, there exists a multitude of web templates available online, but how can you acquire the legal form you require.

Make use of the US Legal Forms platform.

First, ensure you have selected the correct form for your locality/county. You can preview the form with the Preview button and read the description to confirm it is suitable for you. If the form does not meet your requirements, use the Search field to find the appropriate one. Once you are certain that the form is correct, click the Buy Now button to acquire it. Choose the pricing plan you prefer and enter the necessary details. Create your account and complete the purchase using your PayPal account or credit card. Select the file format and download the legal document template to your device. Finally, complete, revise, print, and sign the acquired Arkansas Loan Assumption Agreement. US Legal Forms is the largest repository of legal forms where you can find various document templates. Utilize the service to download professionally crafted documents that adhere to state specifications.

- The service offers thousands of templates, including the Arkansas Loan Assumption Agreement, suitable for both business and personal needs.

- All forms are verified by experts and comply with federal and state regulations.

- If you're already a member, Log In to your account and click the Download button to access the Arkansas Loan Assumption Agreement.

- Utilize your account to browse the legal forms you have previously purchased.

- Visit the My documents tab in your account to obtain another copy of the required document.

- If you are a new user of US Legal Forms, here are some straightforward tips to follow.

Form popularity

FAQ

A loan assumption agreement is an agreement between a lender, original borrower, and a new borrower, where the new borrower agrees to assume responsibility for the debt owed by original borrower. These agreements are commonly seen in mortgages and real estate.

How does the loan assumption process work? Getting approved to assume a loan is similar to getting approved for a new mortgage. You will need to complete an application, provide documents, and meet the lender's credit, income, and financial requirements to get the loan assumption approved.

An assumable mortgage allows a home buyer to not just move into the seller's former house, but to step into the seller's loan, too. This means that the remaining balance, repayment schedule and rate will be taken over by the new owner.

"Assume" means the buyer takes on liability, and the seller is no longer primarily liable. "Subject to" means the seller is not released from responsibility. The word "assumption" is used when a buyer assumes personal liability for an existing debt.

A seller is still responsible for any debt payments if the mortgage is assumed by a third party unless the lender approves a release request releasing the seller of all liabilities from the loan. If approved, the title of the property is transferred to the buyer who makes the required monthly repayments to the bank.

Keep in mind that the average loan assumption takes anywhere from 45-90 days to complete. The more issues there are with underwriting, the longer you'll have to wait to finalize your agreement.

How does the loan assumption process work? Getting approved to assume a loan is similar to getting approved for a new mortgage. You will need to complete an application, provide documents, and meet the lender's credit, income, and financial requirements to get the loan assumption approved.

Lenders must typically approve an assumable mortgage. If done without approval, sellers run the risk of having to pay the full remaining balance upfront. Sellers also risk buyers missing payments, which can negatively impact their credit score.