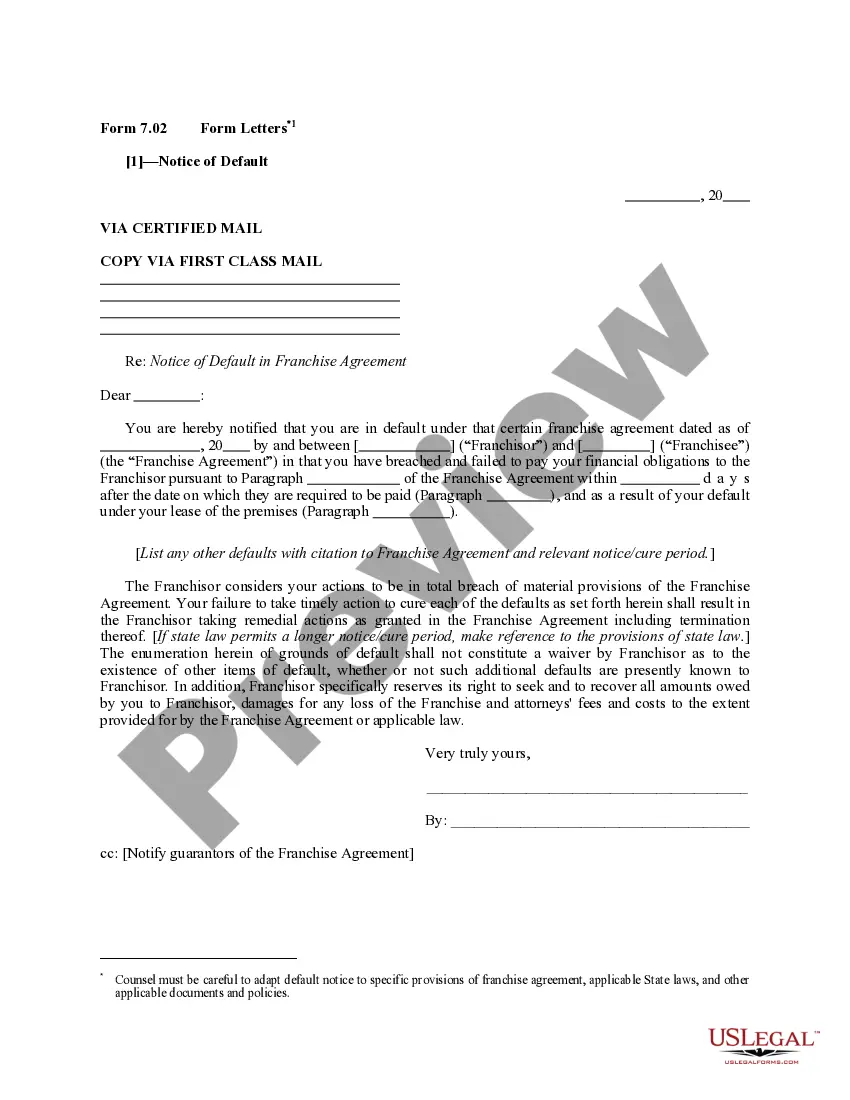

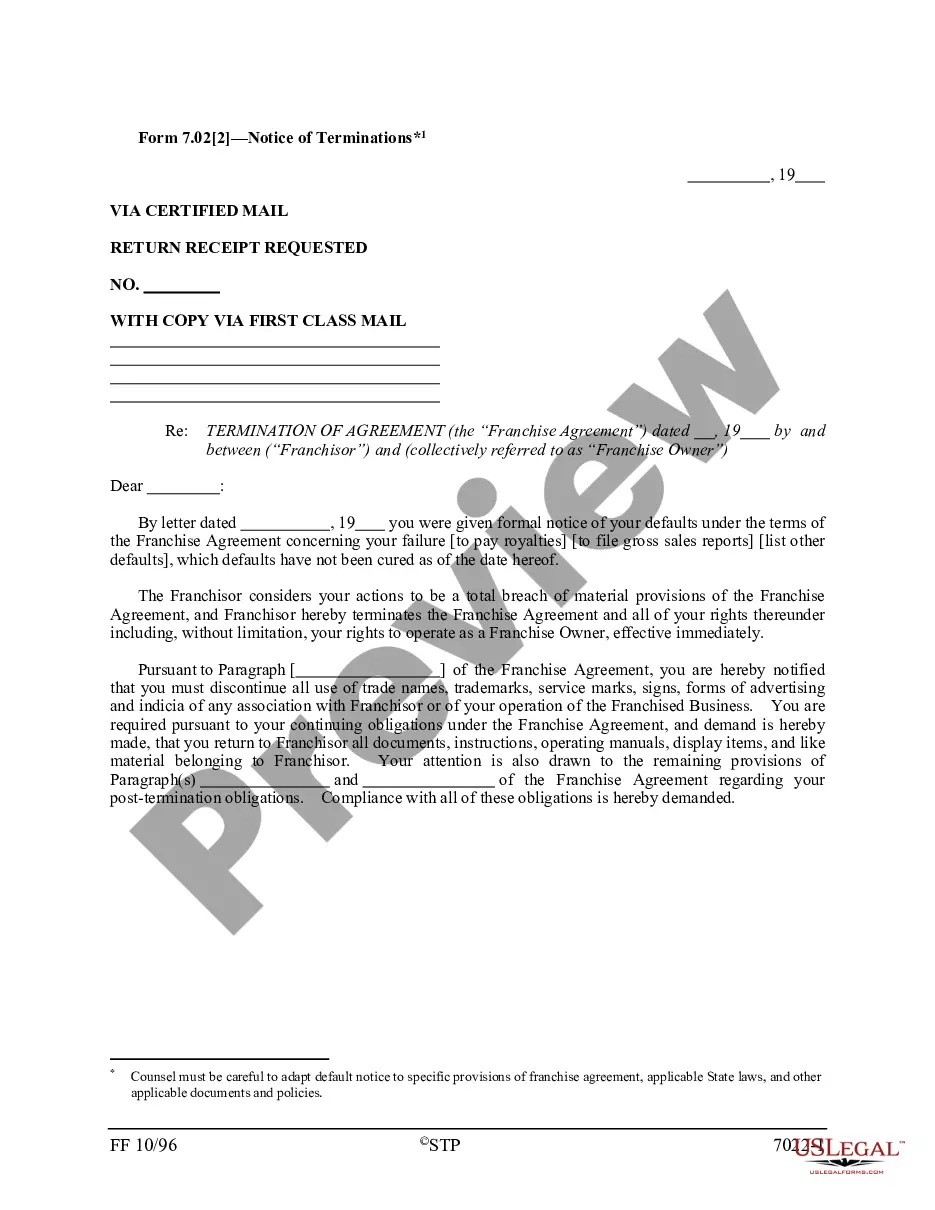

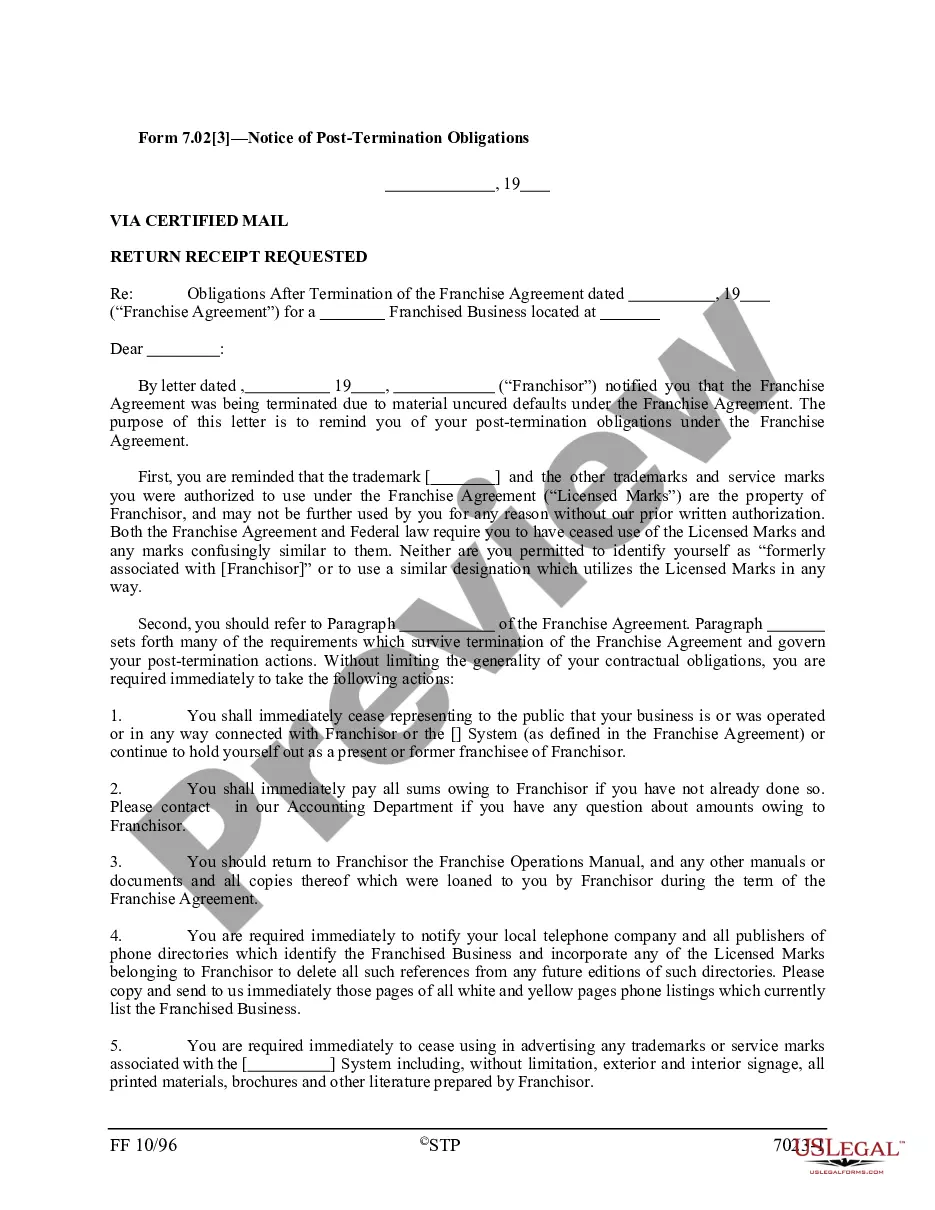

This letter informs a franchisee that he/she is in default of a franchise agreement and failure to take timely action to cure each of the defaults listed in the letter will result in the franchisor taking remedial actions as granted in the agreement.

Alabama Form Letters - Notice of Default

State:

Multi-State

Control #:

US-7-02-1-STP

Format:

Word;

Rich Text

Instant download

Description

How to fill out Form Letters - Notice Of Default?

Are you inside a placement where you need papers for either enterprise or personal reasons virtually every time? There are plenty of legal file layouts available on the net, but finding types you can rely isn`t effortless. US Legal Forms offers a huge number of develop layouts, such as the Alabama Form Letters - Notice of Default, which can be created to fulfill federal and state demands.

If you are presently informed about US Legal Forms site and also have your account, merely log in. Following that, it is possible to obtain the Alabama Form Letters - Notice of Default format.

If you do not come with an account and wish to begin using US Legal Forms, follow these steps:

- Get the develop you will need and ensure it is for the appropriate city/state.

- Utilize the Review option to analyze the shape.

- Read the outline to ensure that you have chosen the right develop.

- In the event the develop isn`t what you are looking for, take advantage of the Research field to get the develop that meets your needs and demands.

- Whenever you find the appropriate develop, just click Buy now.

- Choose the pricing plan you want, fill out the desired info to generate your account, and buy the order utilizing your PayPal or Visa or Mastercard.

- Pick a handy file file format and obtain your copy.

Get all the file layouts you possess purchased in the My Forms food selection. You can get a extra copy of Alabama Form Letters - Notice of Default at any time, if needed. Just click the necessary develop to obtain or produce the file format.

Use US Legal Forms, the most considerable assortment of legal kinds, to save lots of efforts and avoid blunders. The services offers professionally made legal file layouts that you can use for a variety of reasons. Generate your account on US Legal Forms and commence producing your lifestyle a little easier.

Form popularity

FAQ

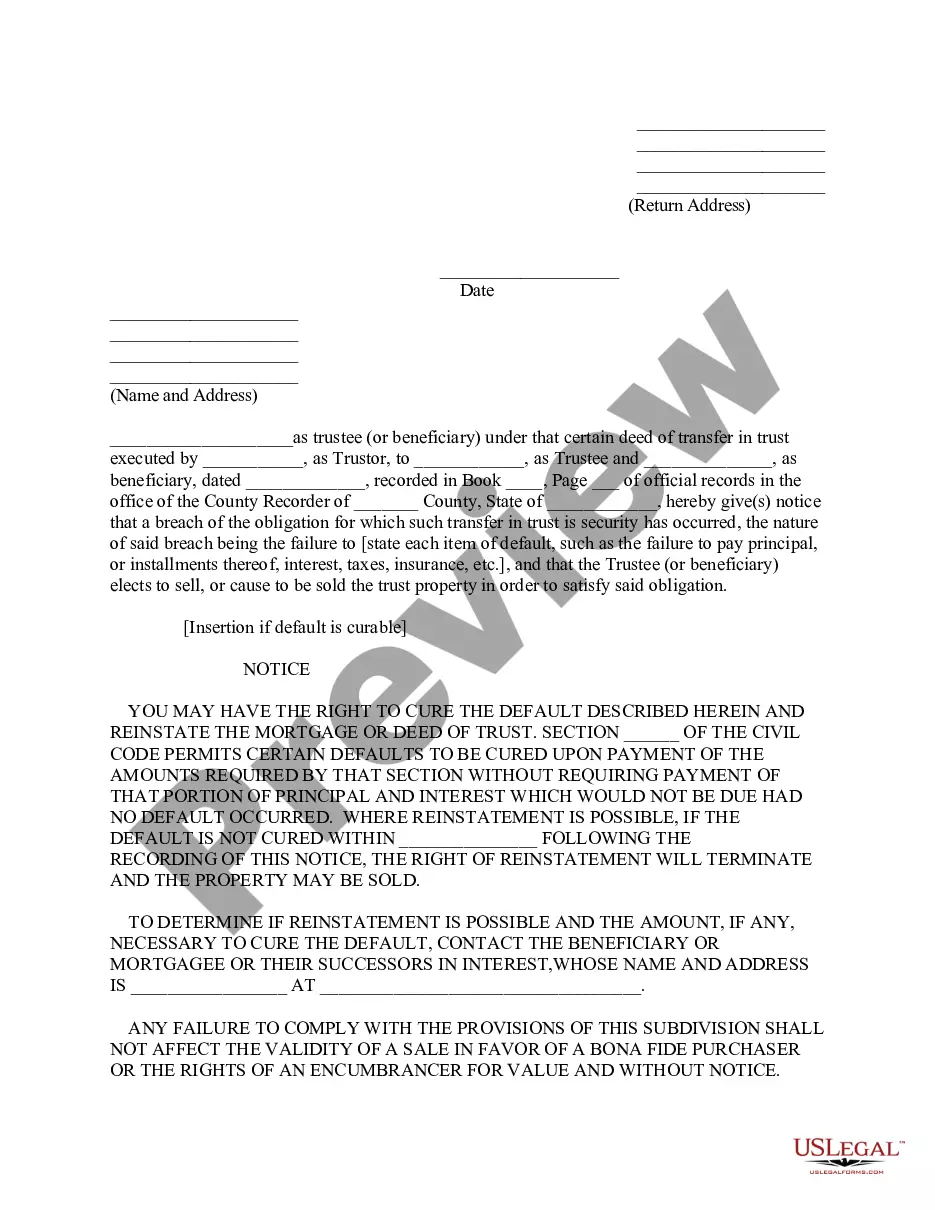

How Notices of Default Work The name and address of the borrower. The name and address of the lender. The legal address of the property. Full details on the nature of the default. What action is required to cure the default. The deadline and the intentions of the lender if the deadline is passed without a cure.

Your name and address (as the borrower) and the name and address of the creditor who is issuing the default notice. The type of agreement and details of how the agreement was broken. The action you need to take to pay the arrears in full by a certain date.

In the context of mortgage foreclosure, a notice of default is a formal notice that a lender filed with courts to notify the borrower who has failed to make payments that the lender intends to conduct a sale foreclosure.

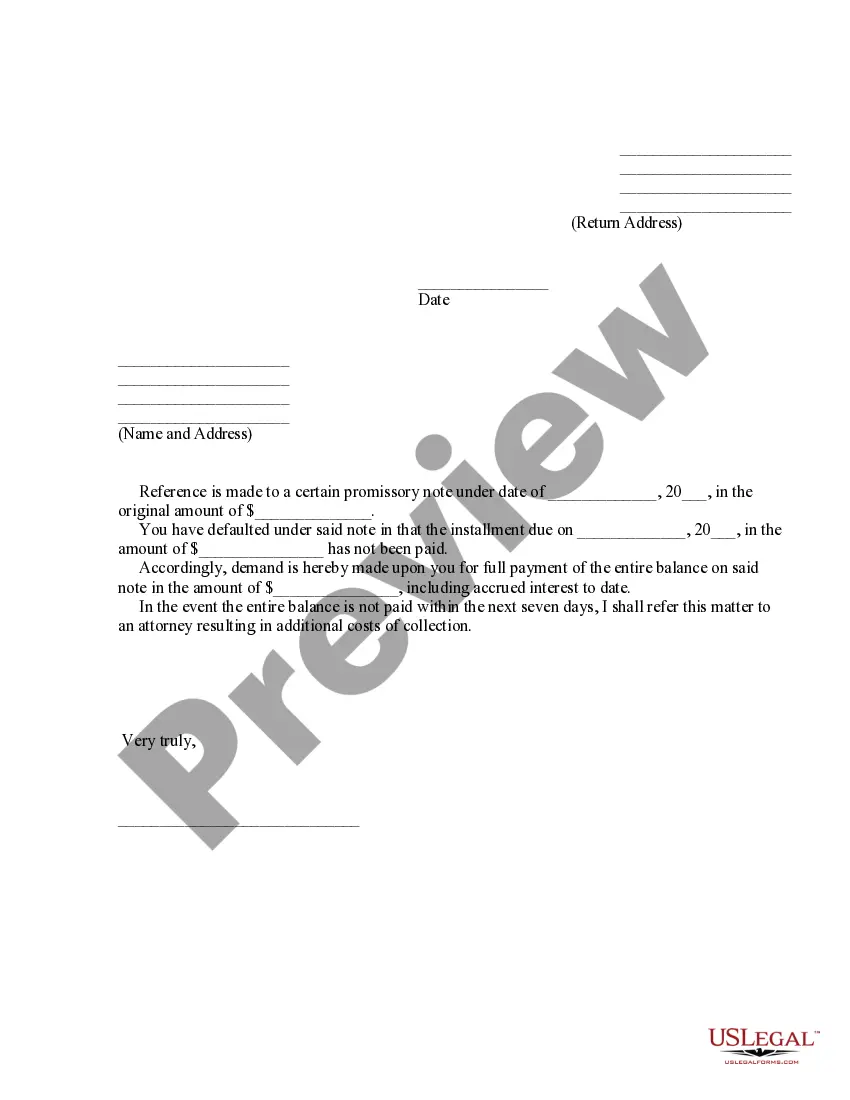

Dated: This is to notify you that you are now in default of your obligations under the above written contract as a result of You have days in which to cure this default. If you do not remedy the default within the allotted time, me us me us at the above address be contacted by phone at . e-mail address is .

A NOD is filed by lenders once their investments go into default status, and is recorded against the property itself. After a NOD is filed and foreclosure actions are documented and taken, credit bureaus are notified.

In the context of mortgage foreclosure, a notice of default is a formal notice that a lender filed with courts to notify the borrower who has failed to make payments that the lender intends to conduct a sale foreclosure.

In most cases, the foreclosure sale can occur 30 days after the default letter is served. If the default isn't cured by the time limit on the default letter, an acceleration letter is sent. This letter states that the balance of the loan, not just the past due balance, is due immediately.

Sample Loan Default Letter I am writing to inform you that your loan is now in default. We must receive payment on the total past due amount of by to prevent legal action. If you have overlooked this payment, please pay it in full now. If you need to make an alternate payment arrangement, please call us.