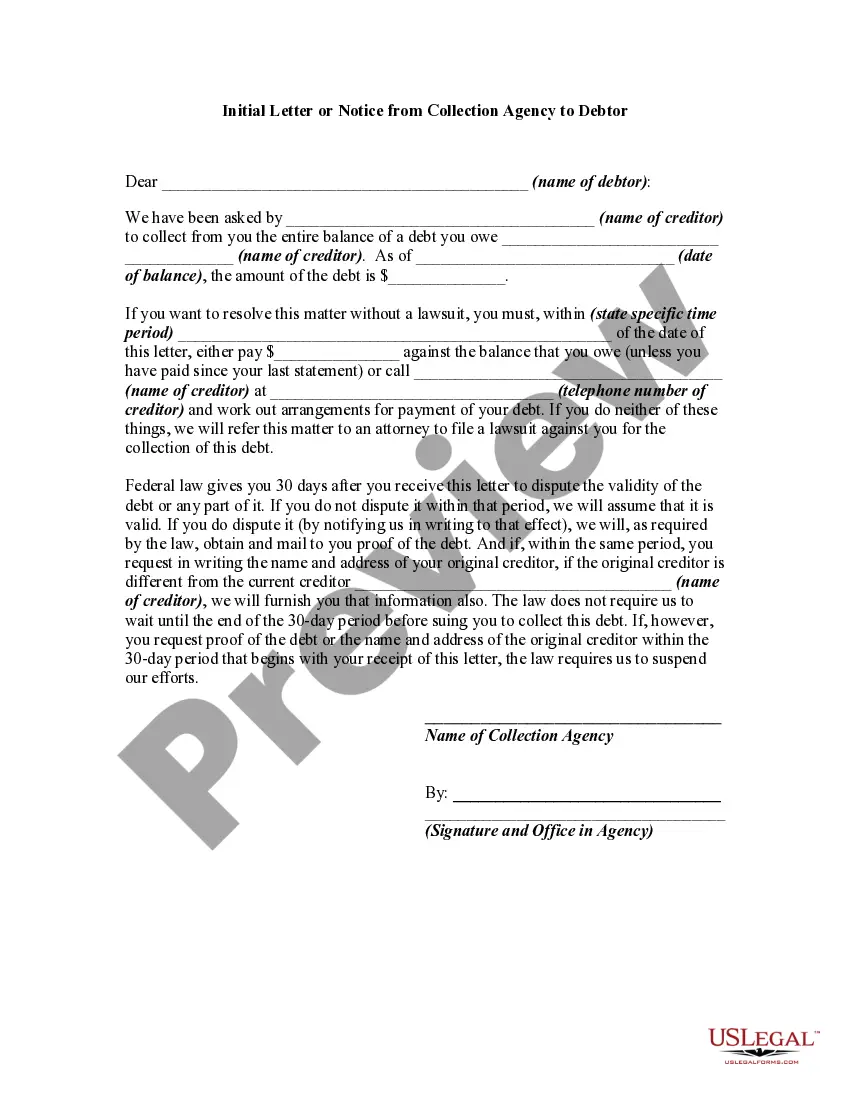

Alabama Collection Letter

Overview of this form

The collection letter is a formal document used to communicate with a debtor regarding an outstanding monetary obligation. It serves to remind the debtor about the amount due, facilitates communication about payment arrangements, and indicates the possibility of legal action if the debt remains unpaid. This letter is essential for establishing a paper trail and is integral to the debt collection process while differing from other forms like demand letters by being more specific in indicating potential legal action if the debt is not settled.

Key parts of this document

- Sender's information: Name and address of the creditor or the law firm handling the collection.

- Recipient's information: Name and address of the debtor.

- Account details: Current outstanding balance and account statement included.

- Contact information: Instructions for the debtor to reach out regarding payment options.

- Deadline for response: Specifies a time frame of ten days for the debtor to respond before legal action may commence.

- Legal disclaimer: Notifies the debtor of their rights regarding the debt.

When to use this form

This collection letter is utilized in situations where a creditor has attempted to collect a debt but has not received payment. It is typically issued before any legal proceedings, thereby providing the debtor with an opportunity to resolve the outstanding balance without escalating the matter to court. Use this form when you need to formally remind a debtor of their payment obligations and establish a timeline for resolution.

Who this form is for

- Creditors seeking to collect outstanding debts from individuals or businesses.

- Law firms representing creditors in debt collection matters.

- Business owners who have provided goods or services on credit.

Completing this form step by step

- Identify the parties: Enter the names and addresses of both the creditor and debtor.

- Specify the account details: Fill in the outstanding balance and attach the current account statement.

- Enter your contact information: Provide your phone number or office address for the debtor to reach you.

- Set a response deadline: Clearly indicate the ten-day period for the debtor to respond.

- Include legal disclaimers: Insert the required legal information regarding debt validity and the debtor's rights.

Does this document require notarization?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include the correct contact information, making it difficult for the debtor to respond.

- Not specifying the outstanding balance clearly, which can confuse the debtor.

- Neglecting to state the deadline for response, potentially affecting the timeline for collection actions.

Why use this form online

- Convenience: Download and customize the form to suit your needs.

- Editability: Easily modify sections to accurately reflect your situation.

- Reliability: Use a legally vetted document prepared by licensed attorneys, ensuring it meets necessary legal standards.

Legal use & context

- A Collection Letter serves as an official notice of debt, which is crucial for legal proceedings if further action is required.

- Sending a formal collection letter is often a prerequisite before initiating a lawsuit for unpaid debts.

- Debt collectors must comply with the Fair Debt Collection Practices Act (FDCPA) when using this form, ensuring transparency and fairness.

What to keep in mind

- A Collection Letter is essential for formally addressing unpaid debts.

- It includes necessary details such as the amount owed and a payment proposal.

- Ensure compliance with state laws and regulations regarding debt collection.

Looking for another form?

Form popularity

FAQ

An Alabama Collection Letter is a formal notice used by creditors or their law firms to inform a debtor about an outstanding debt. It lists the current balance, explains payment options, and creates a paper trail. The letter also warns that legal action could follow if the debt remains unpaid and is typically sent before any lawsuit.

A debt collection letter is sent when a creditor believes there is an unpaid balance. The form includes sender and recipient information, the current balance, and a ten-day deadline to respond. It offers payment options and explains the debtor’s rights, serving as a first step before potential legal action.

Check for the sender’s name and address, the recipient’s information, the account details and balance, clear contact instructions, a ten-day response deadline, and a legal disclaimer about debt rights. The Alabama Collection Letter includes these key components to indicate authenticity.

The Alabama Collection Letter does not specify a monetary threshold that triggers a lawsuit. It focuses on notifying the debtor, sharing account details, and outlining a ten-day window to respond before potential legal action. For thresholds, consult applicable Alabama law or a licensed attorney.

The form itself does not set a time limit for how long debt can be pursued. It establishes a ten-day deadline to respond and indicates potential legal action if unpaid. For state-specific time limits, consult applicable Alabama law or a licensed attorney.

It is tailored to Alabama practice, including a specific ten-day response deadline and a legal disclaimer about rights, along with standard sender, recipient, and account details. This emphasizes a pre-litigation process before any potential action.