Washington Affidavit of Occupancy and Financial Status

Understanding this form

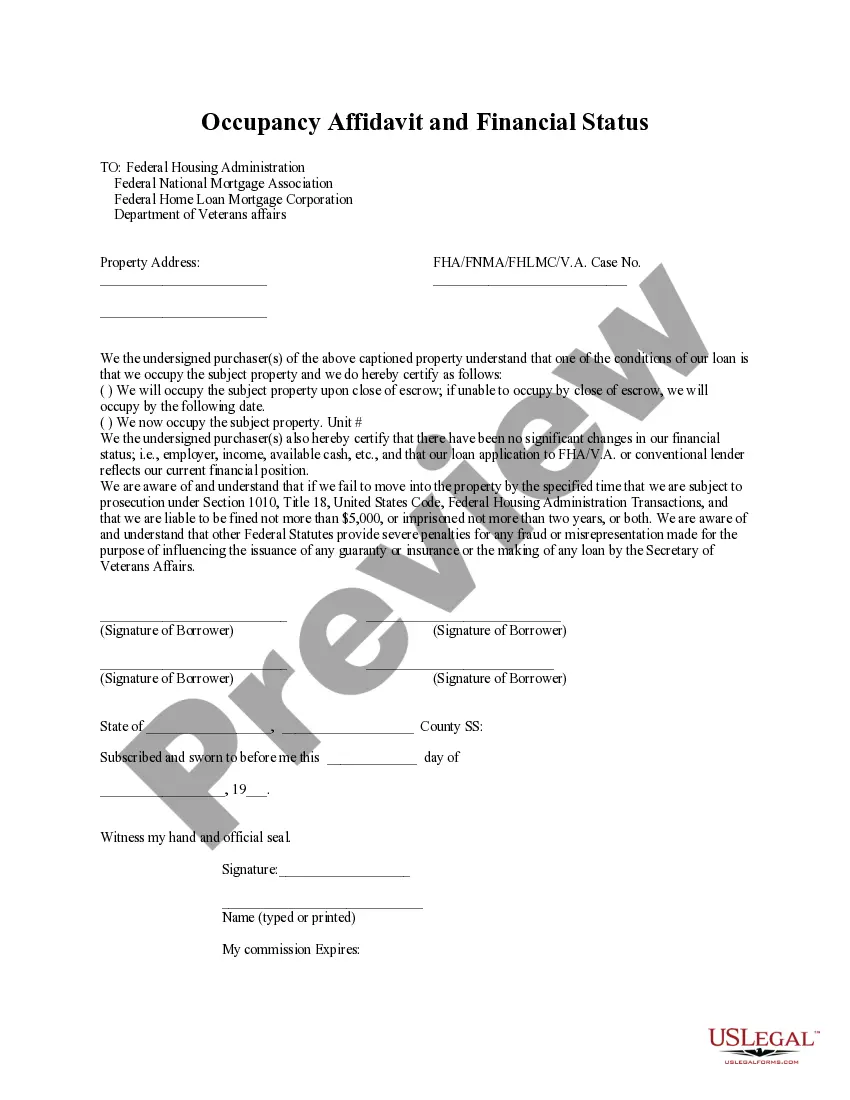

The Affidavit of Occupancy and Financial Status is a legal document that buyers use to confirm they will occupy the property as their primary residence and that their financial situation has not changed since their loan application. This form is essential in the mortgage process, demonstrating the buyer's commitment to living in the property and ensuring compliance with loan conditions from lending institutions.

Form components explained

- Identification of the property address and case number.

- Certification of the buyer's intent to occupy the property, including a timeframe for moving in.

- A declaration of no significant changes in financial status since the loan application.

- Warning about the penalties for failing to comply with occupancy requirements.

- Signature lines for the buyers and their respective dates.

Common use cases

This form should be used at the closing of a real estate transaction when a buyer is obtaining a mortgage. It is particularly relevant when the lender requires confirmation that the property will be the buyer's primary residence and that their financial situation remains stable compared to the information provided in the loan application.

Who can use this document

This form is intended for:

- Homebuyers who are acquiring real estate with a mortgage.

- Individuals who are required by their lender to confirm their intent to occupy the property.

- Buyers needing to affirm that their financial status has not changed since applying for their loan.

Instructions for completing this form

- Identify the property by entering the complete address at the top of the form.

- Fill in the relevant case number assigned by the lender.

- Choose the appropriate checkbox to indicate when you will occupy the property.

- Certify that there have been no significant changes in your financial status since the loan application.

- Sign and date the form to confirm your declarations.

Is notarization required?

To make this form legally binding, it must be notarized. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to provide the correct property address or case number.

- Leaving the date for occupancy blank or incorrectly filled out.

- Not checking the appropriate box indicating your occupancy plans.

- Inaccurately stating financial status changes or omitting details.

- Neglecting to sign and date the form, which can invalidate it.

Advantages of online completion

- Convenient access: Download and complete the form at your convenience.

- Editability: Make necessary changes before finalizing your information.

- Reliability: Ensure your affidavit is prepared consistently and in accordance with legal standards.

Looking for another form?

Form popularity

FAQ

Lenders will take a variety of things into account when determining whether you intend to live in a house and take occupancy type into consideration because people are much less likely to default on the mortgage of a house they are living in.

Lenders and loan officers confirm that they regularly encounter falsehoods about occupancy.Depending on the lender, buyers might be able to save a half to a full percentage point off the interest rate on the loan by calling their purchase a principal residence.

Owner-occupants are residents that own the property that they live at. Some loans are only available to owner-occupants and not absentee owners or investors. To be considered owner-occupied, residents usually must move into the home within 60 days of closing and live there for at least a year.

If you're struggling financially and having trouble paying your mortgage, you may find a field inspector knocking on your door. These inspectors verify that a home remains occupied after its owners miss a mortgage payment. If you're still living in your home, the inspector won't perform an interior search.

Lenders will take a variety of things into account when determining whether you intend to live in a house and take occupancy type into consideration because people are much less likely to default on the mortgage of a house they are living in.

Lenders usually stipulate that homeowners have 30 days after closing to occupy a primary residence. To verify the person moving in is actually the owner, the lender may call the house and ask to speak to the homeowner.The lender may also drive past the house looking for a rental sign in the yard.

Basically, the FHA does require your home to be owner-occupied if you use FHA financing. But, as you can see, there are several exceptions to the rule. Before you decide to do anything, always check with your lender.