Pennsylvania Installments Fixed Rate Promissory Note Secured by Commercial Real Estate

Understanding this form

The Pennsylvania Installments Fixed Rate Promissory Note Secured by Commercial Real Estate is a legal document that outlines a borrower's promise to repay a loan using commercial property as collateral. This form distinguishes itself by being specifically designed for loans secured with business real estate, requiring a separate deed of trust or mortgage in addition to the promissory note.

Key parts of this document

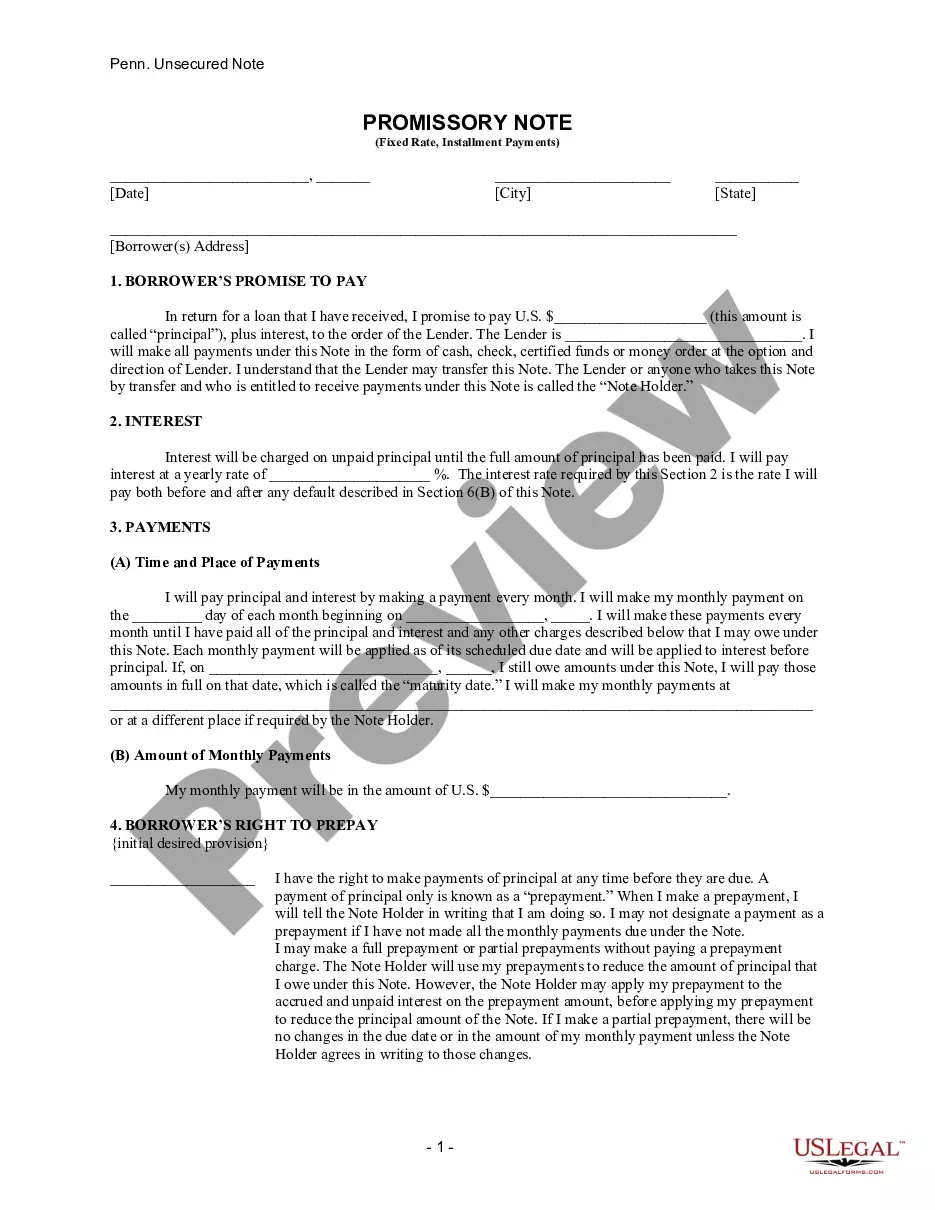

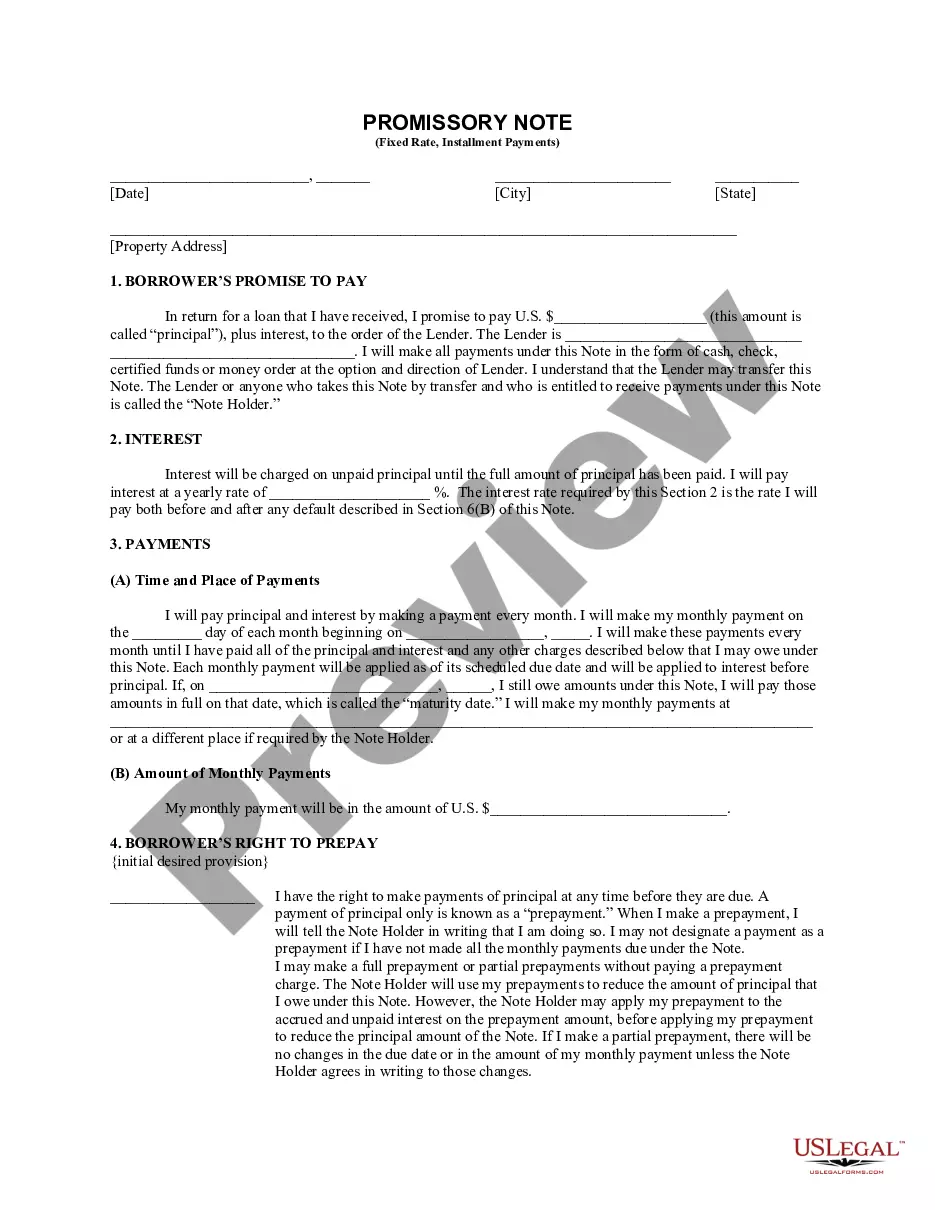

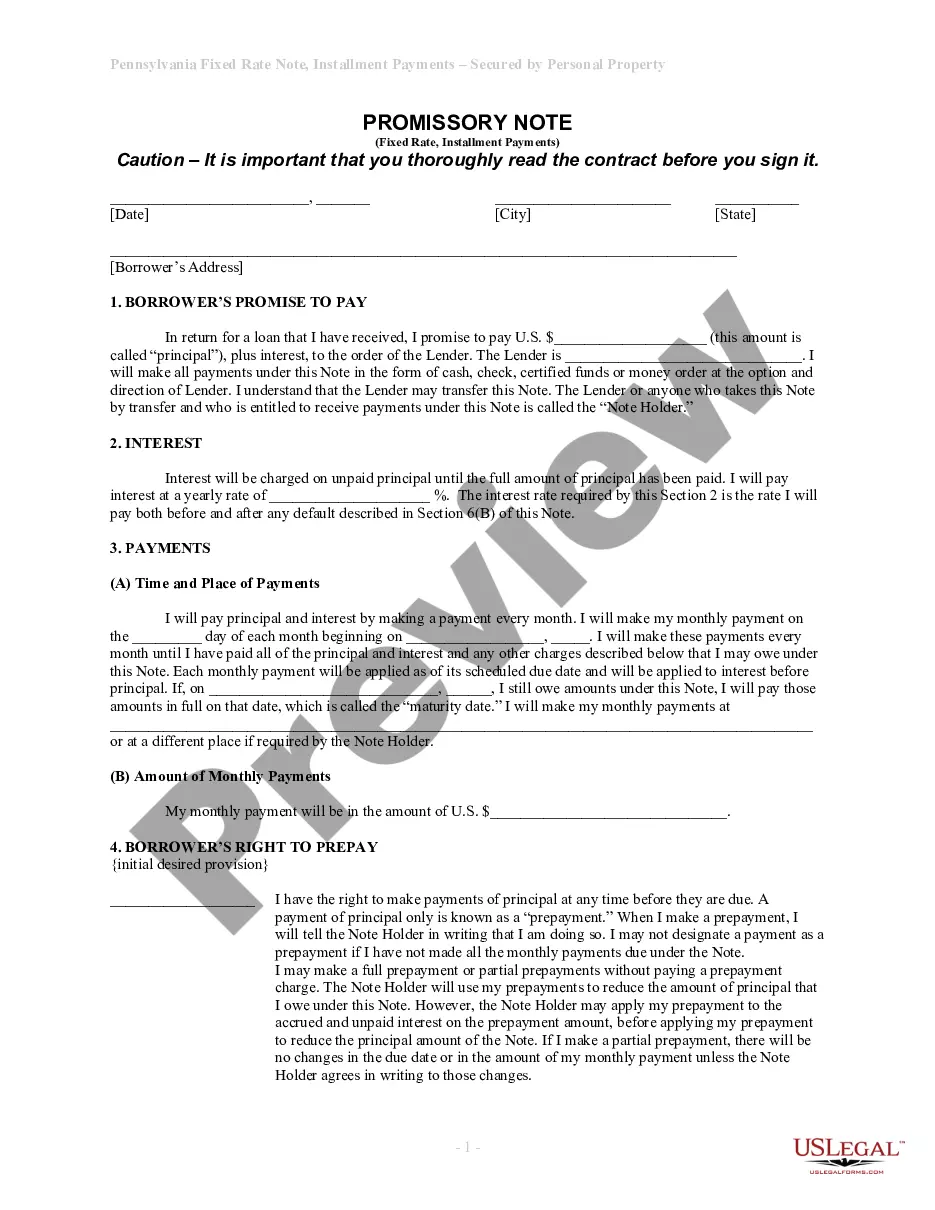

- Borrower's promise to pay a specific principal amount with interest.

- Details on the interest rate applied to the loan.

- Payment schedule outlining monthly payments and the maturity date.

- Prepayment rights that specify whether the borrower can repay the loan early without penalty.

- Consequences for late payments and the definition of default.

- Secured note provisions detailing the collateral used for the loan.

When to use this document

This form is typically used when a borrower seeks financing secured by commercial real estate. Scenarios include purchasing or refinancing a business property, securing loans for business expansion, or consolidating debts with a real estate-backed loan. It is useful for both lenders and borrowers who want to ensure clear terms related to payment and obligations.

Who should use this form

- Business owners seeking a loan to finance commercial real estate.

- Investors looking to secure funding against business property.

- Financial institutions lending money secured by commercial real estate.

- Borrowers needing a structured repayment plan for their business loans.

How to complete this form

- Identify the borrower by entering their full legal name and address.

- Specify the total loan amount and the interest rate in the appropriate sections.

- Fill in the payment schedule, including the date monthly payments begin and the amount of each payment.

- Decide on prepayment rights and initial the chosen option regarding payment before the maturity date.

- Sign the document and have it notarized to ensure legal validity.

Does this document require notarization?

Yes, this form must be notarized to be legally valid. The notarization provides an additional layer of security for both the borrower and lender, ensuring that all parties acknowledge and understand the terms outlined in the agreement. US Legal Forms offers integrated online notarization services, available 24/7, allowing for secure video calls with licensed notaries, all without the need to travel.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to specify the correct interest rate, which can lead to misunderstandings.

- Omitting the borrower's full name or address, which is crucial for legal identification.

- Not initialing the prepayment rights section, leading to confusion regarding future payments.

- Signing the document without notarization if required by local laws.

Why complete this form online

- Convenient access to a legally compliant document that can be downloaded and printed anytime.

- Editability allows you to customize fields according to the specific terms of your loan.

- Reliable and accurate, crafted by licensed attorneys to reflect current laws and standards.

- Provides peace of mind by ensuring the document covers all necessary legal requirements.

Looking for another form?

Form popularity

FAQ

This form creates a legally binding loan agreement in which the borrower promises to repay a fixed-rate loan in installments, with commercial real estate pledged as collateral. It sets the principal amount, interest rate, and payment schedule, and it addresses prepayment, late charges, and default remedies, making it suitable when the loan is secured by property.

Yes. In this form, the promissory note is designed to be secured by real property, giving the lender collateral protection beyond the borrower's promise to pay. The document includes a secured note provision describing how the collateral backs the loan, along with sections for principal, interest, payment terms, and default remedies.

By including a secured note provision that links the loan to the real property's collateral, and by specifying the principal, fixed interest rate, payment schedule, and default remedies. This structure shows how real estate serves as collateral to protect the lender.

This form shows a promissory note can be secured by commercial real estate through the secured note provision. The collateral protects the lender and works with the borrower's promise to pay, the interest terms, and the scheduled payments, with defined consequences for late payments or default.

Yes. The Pennsylvania Installments Fixed Rate Promissory Note Secured by Commercial Real Estate is designed to be secured by commercial property, with collateral backing the loan. The secured note provision describes how the collateral protects the lender, alongside standard terms like principal, interest, payment schedule, prepayment, and default consequences.

This form includes a secured note provision describing collateral protection and ties the loan to commercial real estate as collateral, whereas an unsecured promissory note lacks such collateral. It also sets a fixed-rate installment structure, along with prepayment rights and default remedies appropriate for property-backed financing.