North Carolina Eastern District Bankruptcy Guide and Forms Package for Chapters 7 or 13

Overview of this form

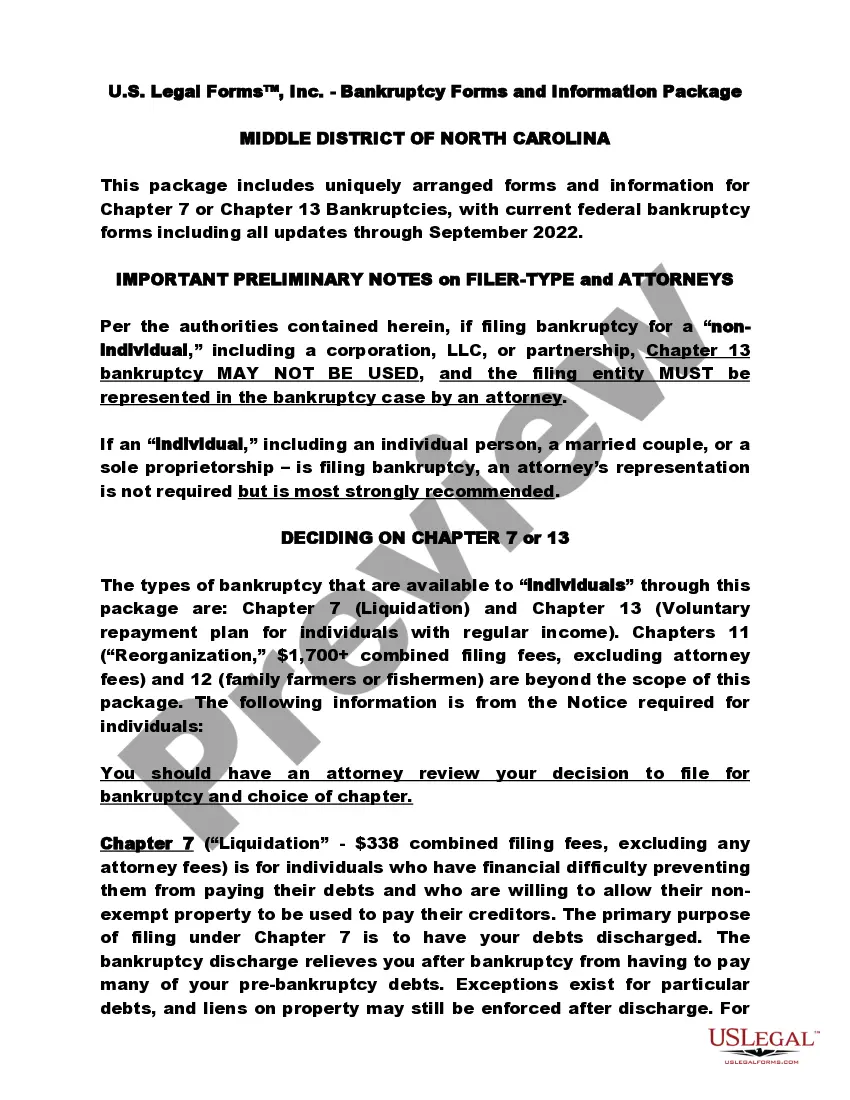

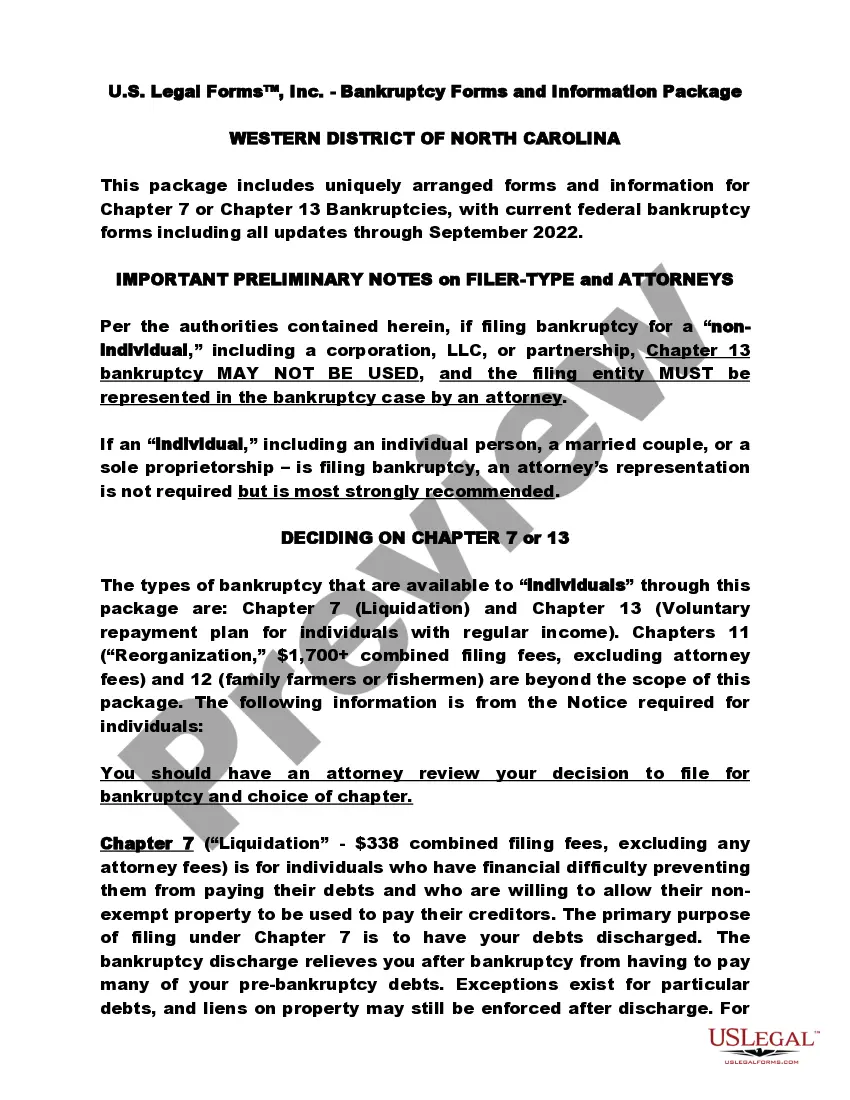

The North Carolina Eastern District Bankruptcy Guide and Forms Package for Chapters 7 or 13 provides a comprehensive set of legal forms and instructions for individuals considering filing for bankruptcy in North Carolina. This package is specially designed for both Chapter 7 (Liquidation) and Chapter 13 (Voluntary repayment). It is crucial to understand that while individuals can file without an attorney, legal representation is strongly recommended to navigate complex bankruptcy rules and procedures effectively.

Key components of this form

- Detailed instructions for completing bankruptcy forms.

- Forms required for Chapter 7 and Chapter 13 bankruptcies.

- Information on exemptions, property rights, and the bankruptcy process.

- Login instructions for accessing the package online.

- Clarification on eligibility for filing under each bankruptcy chapter.

- Guidance on the Means Test used in Chapter 7 filings.

Situations where this form applies

This form package is applicable when an individual in North Carolina is experiencing financial difficulty and is considering bankruptcy as a solution. Use this package if you are unsure about which chapter to file or need structured guidance on how to approach the bankruptcy process, particularly if you wish to pursue either a liquidation of debts under Chapter 7 or a repayment plan under Chapter 13.

Intended users of this form

- Individuals considering bankruptcy, including single filers and married couples.

- Sole proprietors with significant personal debt.

- People with regular income who wish to file for Chapter 13 repayment.

- Those seeking legal protection from creditors while discharging their debts.

- Individuals needing guidance on state-specific bankruptcy laws.

Completing this form step by step

- Determine your eligibility for Chapter 7 or Chapter 13 bankruptcy.

- Gather all financial documentation, including income, expenses, and debts.

- Complete the required forms as outlined in the package instructions.

- List any exempt property on the appropriate schedules, ensuring it follows state regulations.

- Submit your completed forms to the bankruptcy court along with the required fees.

- Be prepared for a hearing if applicable, and follow up on any additional documentation requests from the court.

Is notarization required?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to disclose all debts and assets accurately.

- Not understanding the eligibility criteria for Chapter 7 versus Chapter 13.

- Missing critical deadlines for filing and responding to court notices.

- Ignoring the requirements for the Means Test in Chapter 7 filings.

- Overlooking the exemptions you may qualify for in your bankruptcy filing.

Benefits of completing this form online

- Convenient access to all necessary forms in one package for streamlined filing.

- Edit and customize forms based on your specific financial situation.

- Reliable legal documents drafted with input from licensed attorneys.

- Step-by-step guidance helps ensure accuracy and completeness in your filing.

Legal use & context

- Filing for bankruptcy under Chapter 7 can lead to debt discharge but may require surrendering non-exempt assets.

- Chapter 13 allows individuals to create a repayment plan, making it a preferable option for those with regular income.

- Bankruptcy laws are designed to provide a fresh start but require adherence to complex rules and timelines.

Quick recap

- Understand your options between Chapter 7 and Chapter 13 bankruptcy.

- Ensure accurate completion of all required forms to prevent delays in processing.

- Consider seeking legal advice to navigate bankruptcy complexities effectively.

- Be aware of state-specific regulations and filing requirements in North Carolina.

Looking for another form?

Form popularity

FAQ

There is no minimum amount of debt you must have in order to file for bankruptcy relief. While the amount of your debt is an important factor to consider, there are other more important factors to take into account in determining if a bankruptcy filing is in your best interest.

Your credit will suffer when you file a Chapter 13 case, but it will drop from your credit report years before a Chapter 7 case would. Your credit report will reflect your decision to file bankruptcy for years after you file, so there's no escaping the reality that filing bankruptcy will negatively affect your credit.

Disadvantages of Filing for Chapter 13 Bankruptcy Be aware that it can take up 5 five years for you to repay your debts under a Chapter 13 plan, and debts must be paid out of your disposable income.A Chapter 13 bankruptcy can remain on your credit report for up to 10 years, and you will lose all your credit cards.

Loss of credit cards. Immediate impact on your credit score. Difficultly obtaining a mortgage or loan. Loss of property and real estate. Denial of tax refunds. Job and housing stigma. Non-Dischargeable debts.

Though bankruptcy will indeed remain on a credit score for up to 10 years, this does not mean that your credit score will be ruined forever. In fact, with the right support, information, and guidance, you can take steps towards recovering your credit score and living life debt-free - once and for all!

Get Your Filing Fee The court filing fee for a Chapter 7 bankruptcy in North Carolina is $338. You should bring the fee with you when you go to file your case, ideally as a cashier's check or money order, payable to "Clerk, U.S. Bankruptcy Court".

Key Takeaways. Chapter 7 bankruptcy doesn't require a repayment plan but does require you to liquidate or sell nonexempt assets to pay back creditors.Chapter 13 bankruptcy eliminates qualified debt through a repayment plan over a three- or five-year period.

For many debtors, Chapter 7 bankruptcy is a better option than Chapter 13 bankruptcy.For instance, Chapter 7 is quicker, many filers can keep all or most of their property, and filers don't pay creditors through a three- to five-year Chapter 13 repayment plan.

A Chapter 13 bankruptcy involves repaying some or all of your debt over a three- to- five-year period, while a Chapter 7 bankruptcy involves wiping out most of your debts without paying them back.In that way, a Chapter 13 may be better for your credit than a Chapter 7.