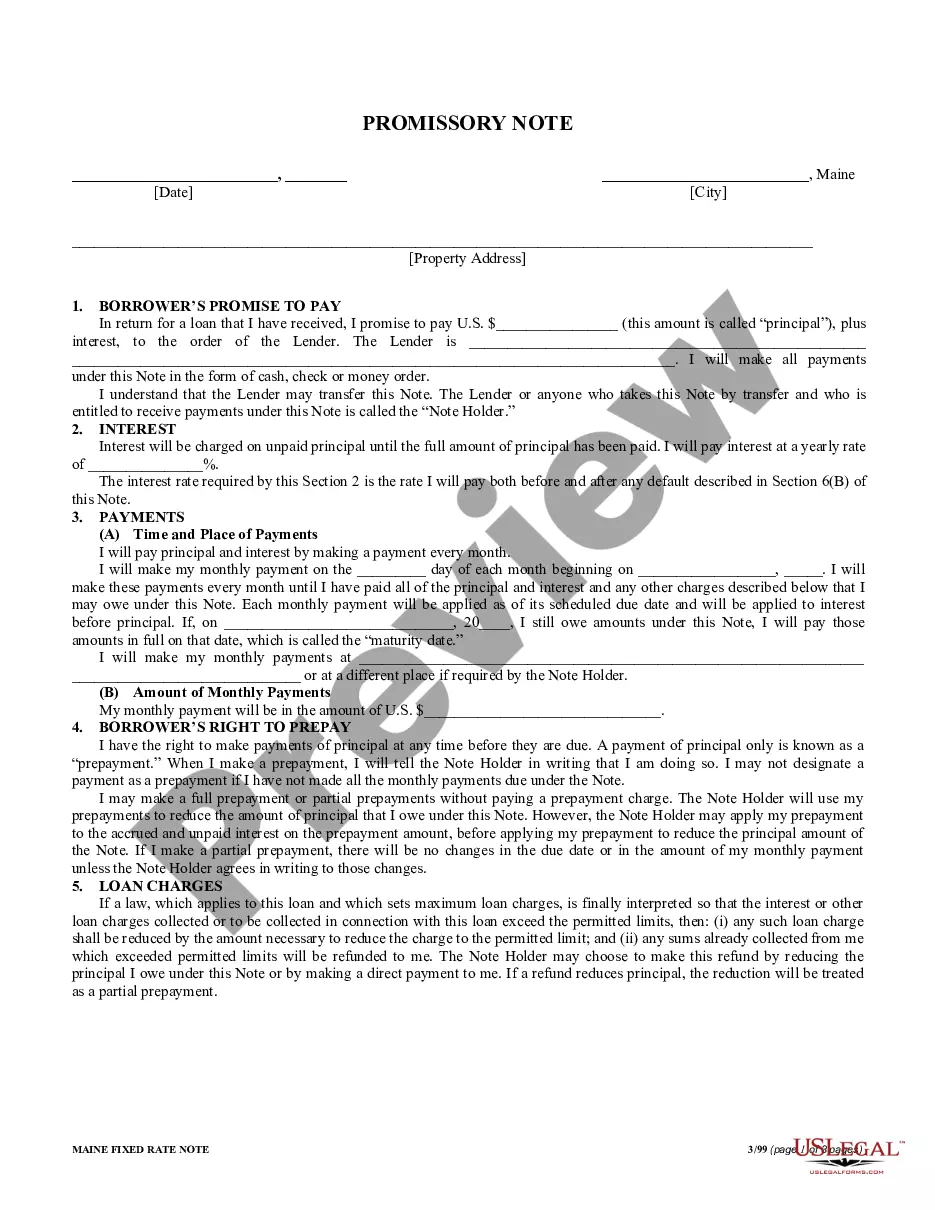

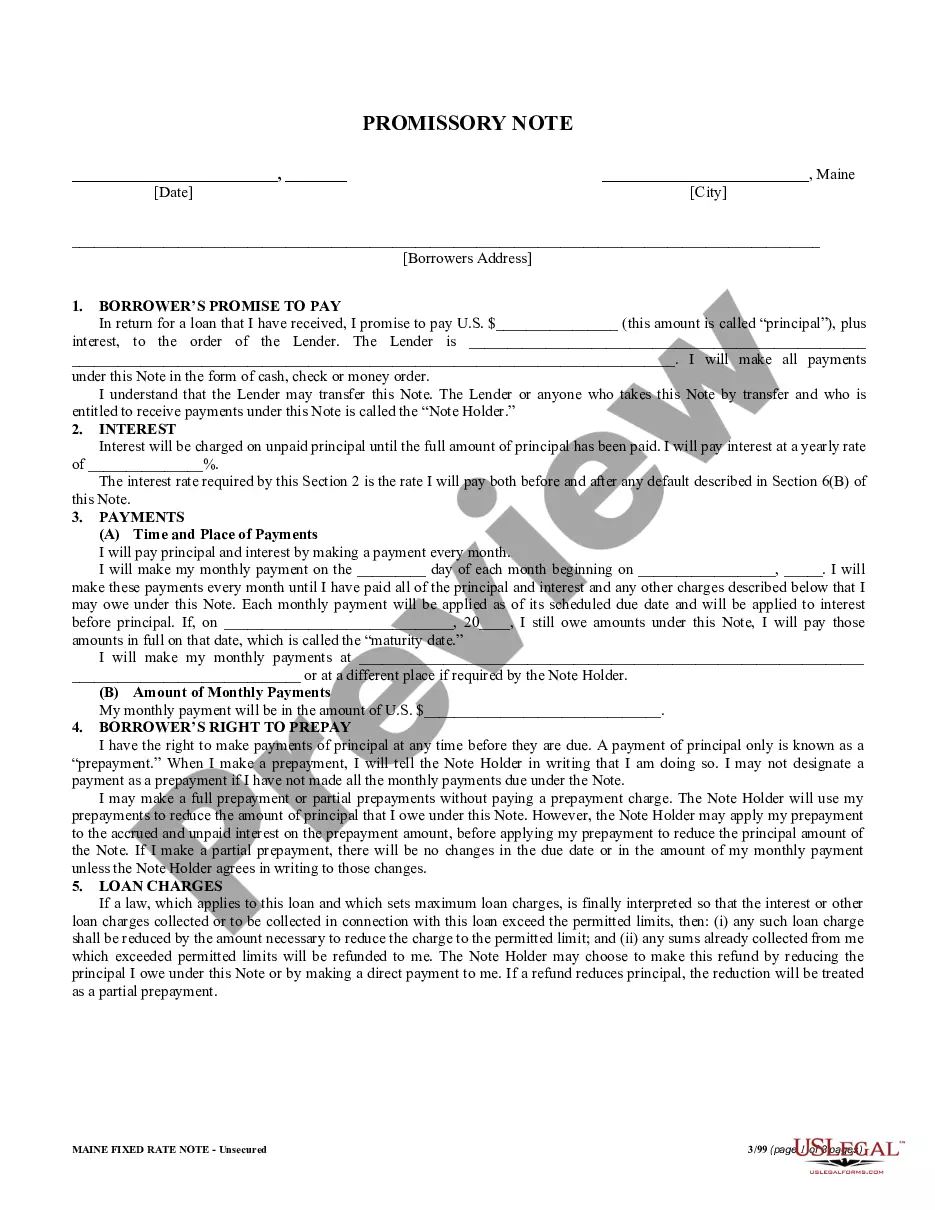

Maine Installments Fixed Rate Promissory Note Secured by Commercial Real Estate

What this document covers

The Maine Installments Fixed Rate Promissory Note Secured by Commercial Real Estate is a legal document that outlines a borrower's promise to repay a loan, using commercial property as collateral. This form is essential for securing financing, ensuring both parties have a clear agreement regarding the terms of the loan, including interest rates and repayment schedules. It differs from personal promissory notes as it specifically involves commercial property, making it necessary for business transactions.

What’s included in this form

- Borrower's promise to pay the principal amount and interest to the lender.

- Details of the interest rate and calculation of interest on unpaid principal.

- Payment schedule specifying the amount and frequency of payments.

- Borrower's rights regarding prepayment of the loan.

- Provisions for late payment charges and default notices.

- Requirements related to the security interest in the commercial property.

When this form is needed

This form should be used when a borrower wishes to secure a loan for business purposes using commercial real estate as collateral. It is suitable in scenarios such as purchasing commercial properties, refinancing an existing loan, or acquiring funds for business expansion. This note provides legal clarity and protection for both the lender and borrower during the financing process.

Intended users of this form

- Businesses looking to secure a loan for commercial purposes.

- Individuals who intend to purchase or refinance commercial real estate.

- Lenders providing financing against commercial property as collateral.

How to prepare this document

- Identify the borrower(s) and lender, including their full addresses.

- Specify the loan amount (principal) and the annual interest rate.

- Fill in the payment schedule, including the start date and the amount of each monthly payment.

- Indicate the borrower's rights regarding prepayment of the loan.

- Include any necessary signatures and ensure notarization if required.

Is notarization required?

Yes, this form must be notarized to be legally valid. US Legal Forms offers integrated online notarization services, available 24/7 through secure video calls, ensuring your document complies with legal requirements without the need for travel.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to specify the interest rate clearly, leading to misunderstandings.

- Not including the correct payment schedule or amounts.

- Neglecting to discuss rights regarding prepayment with the lender.

- Omitting the borrower's or lender's signatures or notarization if needed.

Advantages of online completion

- Convenient access to the form that can be completed from anywhere.

- Editable formats to tailor the document to specific needs.

- Reliability of documents created with input from licensed attorneys.

- Instant download and printing options available.

Key takeaways

- The Maine Installments Fixed Rate Promissory Note secures a loan against commercial real estate.

- Clear terms help avoid disputes between borrowers and lenders.

- Proper completion of the form ensures legal enforceability.

- Notarization enhances the validity of the agreement.

Looking for another form?

Form popularity

FAQ

Secured or unsecured? Generally, promissory notes are unsecured which means it is more like a formal IOU. However, lenders can request some security for the loan. For personal secured promissory notes, a house or car is often used as collateral.

Promissory notes are ideal for individuals who do not qualify for traditional mortgages because they allow them to purchase a home by using the seller as the source of the loan and the purchased home as the source of the collateral.

Types of Property that can be used as collateral. Speak to them in person. Draft a Demand / Notice Letter. Write and send a Follow Up Letter. Enlisting a Professional Collection Agency. Filing a petition or complaint in court. Selling the Promissory Note. Final Tips.

Commercial Promissory note A commercial promissory note is used when borrowing money from a commercial lender such as a bank or loan agency. In the event the borrower is unable to make required payments, the lender may demand full payment of the loan including interest.

The lender holds the promissory note while the loan is being repaid, then the note is marked as paid and returned to the borrower when the loan is satisfied. Promissory notes aren't the same as mortgages, but the two often go hand in hand when someone is buying a home.

Unlike a mortgage or deed of trust, the promissory note isn't recorded in the county land records. The lender holds the promissory note while the loan is outstanding. When the loan is paid off, the note is marked as "paid in full" and returned to the borrower.

"A promissory note is enforceable through an ordinary breach of contract claim." In other words, it's not required that the loan be secured; an unsecured loan is still enforceable as long as the promissory note is fully completed. Lender and borrower information.

In general, under the Securities Acts, promissory notes are defined as securities, but notes with a maturity of 9 months or less are not securities.The US Supreme Court in Reves recognizes that most notes are, in fact, not securities.

To secure a promissory note means that you identify some specific property and attach it to the note. Then, if the borrower defaults on the loan, you will be able to repossess the collateral as compensation for the loan.