Indiana Northern District Bankruptcy Guide and Forms Package for Chapters 7 or 13

About this form

The Indiana Northern District Bankruptcy Guide and Forms Package for Chapters 7 or 13 provides essential legal documents and instructions for individuals seeking bankruptcy relief. This package is designed specifically for Chapter 7 (Liquidation) and Chapter 13 (Voluntary Repayment Plan) bankruptcies, setting it apart from other bankruptcy resources by offering tailored guidance and forms based on state-specific requirements.

Key parts of this document

- Comprehensive instructions for filing under Chapter 7 and Chapter 13.

- Official forms required for Chapter 7 and Chapter 13 bankruptcy submissions.

- Specific disclosures about required documentation and filing fees.

- Cautions regarding eligibility and attorney representation.

- Exempt property listings to protect certain assets during bankruptcy.

Situations where this form applies

This form package is necessary when an individual in Indiana is unable to pay their debts and needs to file for bankruptcy under the applicable chapters. It is particularly useful when deciding whether to liquidate assets under Chapter 7 or to set up a repayment plan through Chapter 13. Users should consult the instructions carefully to determine the best bankruptcy route based on their financial situation.

Who should use this form

- Individuals experiencing financial hardship and considering bankruptcy.

- Married couples filing a joint bankruptcy case.

- Sole proprietors seeking debt relief through personal bankruptcy.

- Any individual needing detailed instructions and forms for Chapter 7 or Chapter 13 filings.

How to prepare this document

- Determine your eligibility for Chapter 7 or Chapter 13 bankruptcy based on your financial circumstances.

- Gather required documents, including income statements and a list of debts, to support your filing.

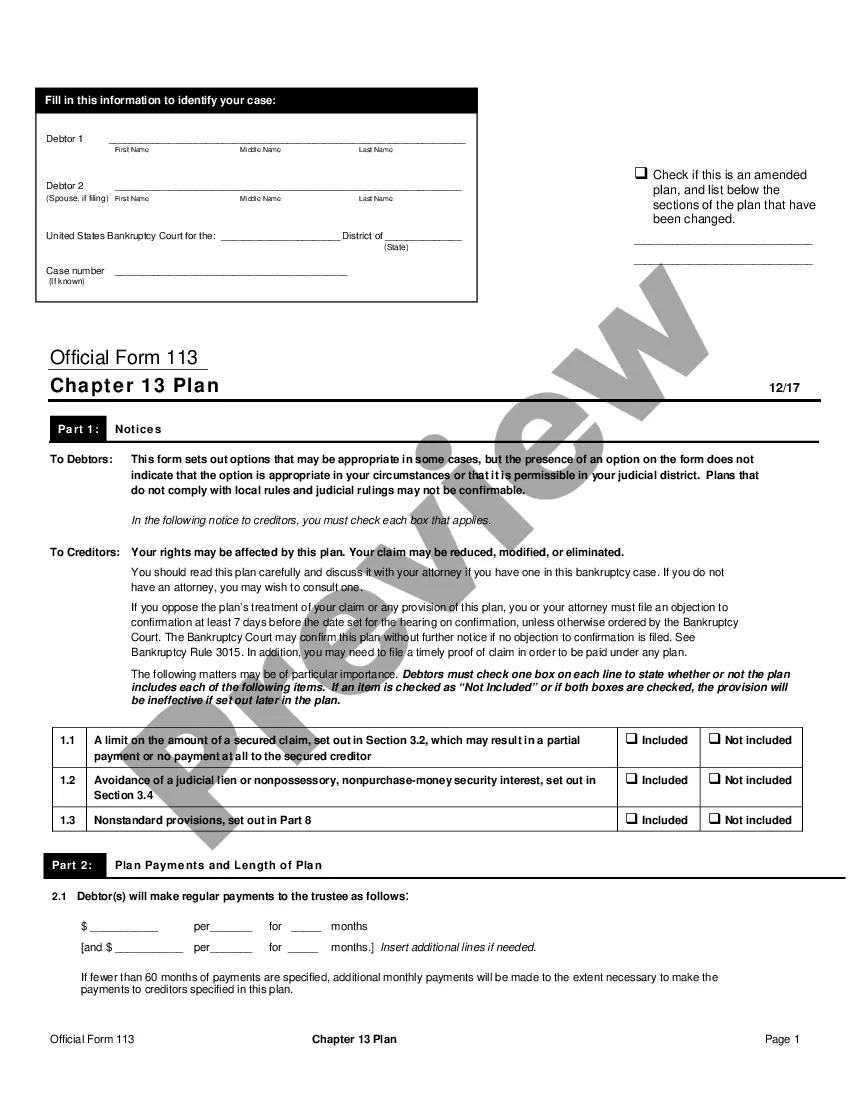

- Fill out the Chapter 7 Statement of Current Monthly Income or Chapter 13 repayment plan forms as needed.

- List any exempt property on Schedule C to protect certain assets.

- Review all forms for accuracy and submit them to the appropriate Indiana Bankruptcy Court.

Notarization guidance

This form does not typically require notarization unless specified by local law. Users should verify local requirements for any additional documentation that may need notarization.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to disclose all debts and income accurately.

- Neglecting to list exempt property, which may lead to asset loss.

- Using the wrong forms or omitting necessary forms in the submission.

- Not consulting an attorney when required or recommended.

Advantages of online completion

- Immediate access to up-to-date legal forms and instructions specific to Indiana.

- Time-saving process with the ability to download and print forms instantly.

- Editability allows users to customize their forms easily, reducing the chances of error.

Summary of main points

- This package is essential for Indiana residents filing for bankruptcy under Chapters 7 or 13.

- Proper completion of the forms and understanding exemptions are vital for effective bankruptcy filing.

- Consulting with an attorney is highly recommended to navigate complex legal requirements.

Looking for another form?

Form popularity

FAQ

Analyze your debt. Determine your property exemptions. Make sure you are eligible. Redeem or reaffirm secured debts. Fill out the bankruptcy forms. Take a credit counseling course. File the forms. Pay the filing fee or request a fee waiver.

Avoid Transferring Assets Before Filing for Chapter 7 Bankruptcy. Avoid Favoring Creditors Before a Bankruptcy Filing. Avoid Making Credit Card Purchases Before a Chapter 7 Filing. Avoid Depositing Unusual Amounts Before Filing Bankruptcy.

Advise you on whether to file a bankruptcy petition. Advise you under which chapter to file. Advise you on whether your debts can be discharged. Advise you on whether or not you will be able to keep your home, car, or other property after you file. Advise you of the tax consequences of filing.

File at the wrong time. use retirement funds unnecessarily. prepare bankruptcy paperwork carelessly or incorrectly. purchase luxury goods and services on credit or take cash advances. sell or transfer property for less than it's worth. pay only your favorite creditors.

There is no minimum amount of debt you must have in order to file for bankruptcy relief. While the amount of your debt is an important factor to consider, there are other more important factors to take into account in determining if a bankruptcy filing is in your best interest.

Stop making payments on debts that will get wiped out in bankruptcy and pay your attorney instead. borrow the fees from a friend, family member, or even your employer. retain a bankruptcy lawyer who will handle creditor calls while you pay fees over time. file on your own.

In general, you can engage in a certain amount of exemption planning before filing your case, but it must be reasonable and in good faith. For example, if you have too much cash in your bank account, you can typically spend it on food, rent, gas, car maintenance, or other necessities before filing for bankruptcy.

If your annual income, as calculated on line 12b, is less than $84,952, you may qualify to file Chapter 7 bankruptcy. If it's greater than $84,952, you'll have to continue to Form 122A-2, which we'll review in the next section. It should be noted that every state has different median income calculations.

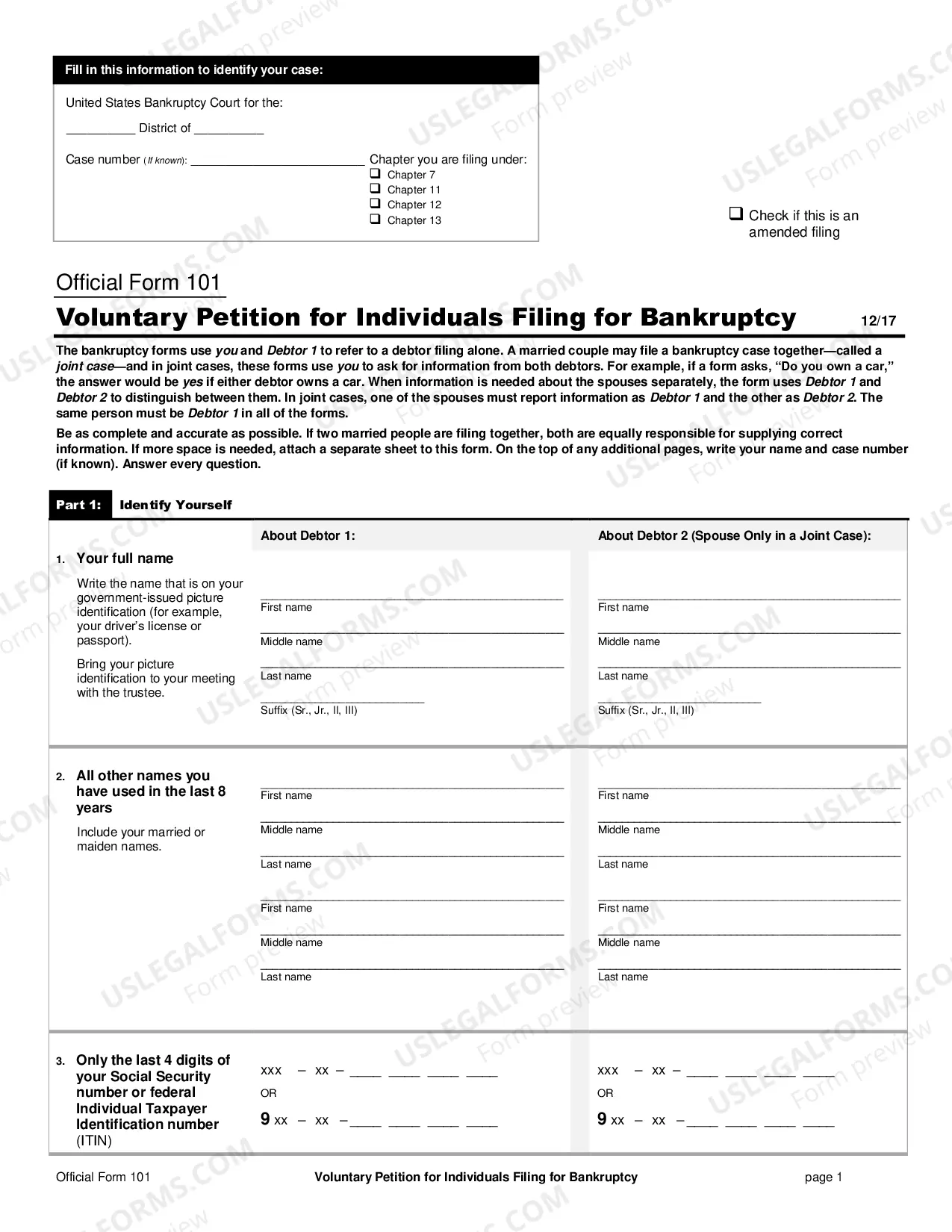

Identifying Information. The Voluntary Petition for Individuals Filing for Bankruptcy form acts as the cover sheet for your paperwork. Your Property. Your Exempt Property. Your Collateralized Debt. Your Other Debt. Your Contracts and Leases. Your Codebtors. Your Income.