Gift Real Grantor Blank With A Trust

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Virginia Deed Of Gift?

- Log into your US Legal Forms account if you're a returning user. Download the relevant form template by hitting the Download button, ensuring you have an active subscription.

- For first-time users, browse through the Preview mode and form descriptions to select the correct form that aligns with your needs and jurisdiction.

- If the form does not meet your criteria, utilize the Search feature to find an alternative template that suits you better.

- Once satisfied with your choice, click the Buy Now button and choose your desired subscription plan. You will need to create an account to access all resources.

- Complete your purchase by providing credit card information or using PayPal for your subscription.

- Download the form to your device for further completion and ensure you can access it later in the My Forms section of your profile.

By following these steps, you can easily create the necessary legal documentation to facilitate a gift with confidence.

US Legal Forms ensures a user-friendly experience, empowering you to manage your legal needs effectively. Start your journey today and explore our vast library of over 85,000 forms!

Form popularity

FAQ

Yes, you can file Form 709 separately from your annual tax return. This allows you to specifically address gifts, such as a gift real grantor blank with a trust, without intertwining it with your regular income taxes. Always ensure that you meet the deadlines for both filings to avoid complications.

To report a gift to a trust on IRS Form 709, you need to complete the form accurately, specifying the value of the gift. When dealing with a gift real grantor blank with a trust, it's essential to provide detailed information about the trust and the gift amount. Accurate reporting ensures transparency and can protect you from any future tax issues.

Distributions from a trust might be considered gifts, but it largely depends on the circumstances. If the trust was set up correctly with regard to the gift real grantor blank with a trust, distributions are typically not classified as gifts for tax purposes. To clarify your situation, you should seek advice from a tax expert or estate planner.

Payouts from a trust can be taxable depending on various factors. When you receive income from a trust, that income may be subject to taxes. However, the principal amount, especially if it relates to the gift real grantor blank with a trust, generally does not incur tax. It’s vital to consult with a tax professional to understand your specific situation.

Trusts can involve gifts, especially when assets are placed into the trust for beneficiaries. However, the trust is not a gift in itself; it is a legal structure that facilitates the management and distribution of gifts. Using a gift real grantor blank with a trust allows you to maintain control and provide for loved ones over time, balancing gifting and asset management.

A trust fund can be considered a gift if assets are transferred into the trust without expecting anything in return. However, the trust itself is a separate legal entity that manages these assets. When you utilize a gift real grantor blank with a trust, you can establish a clear framework for these transactions, making your intentions explicit.

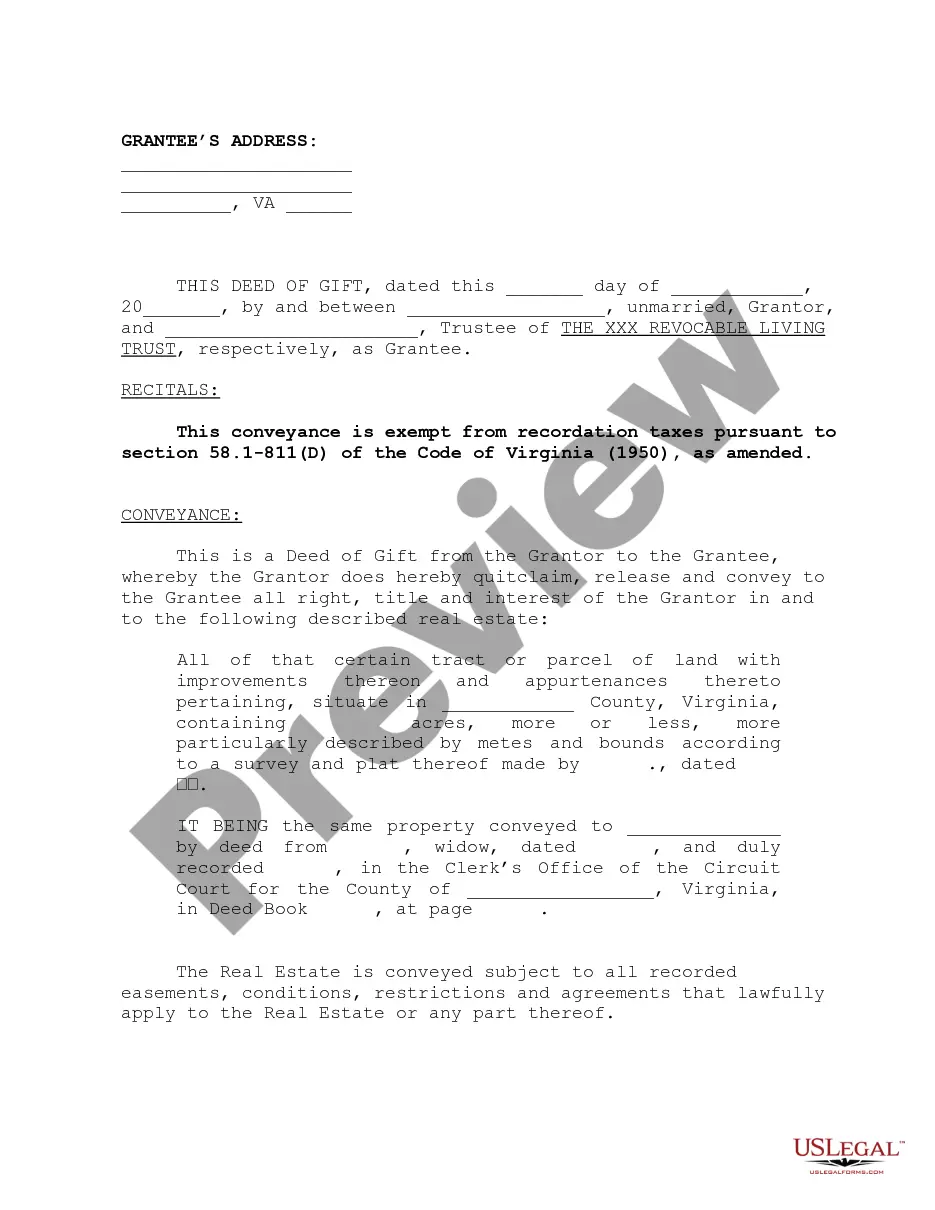

The grantor of a trust is the individual who creates the trust and contributes assets to it. This person outlines the terms and conditions for how the trust operates and who benefits. If you're working with a gift real grantor blank with a trust, you will take on the role of the grantor, giving you control over your assets.

A trust is a legal entity that holds and manages assets, while a gift is a transfer of property or funds without expecting anything in return. When establishing a gift real grantor blank with a trust, you can combine these concepts, as the trust can facilitate the management of gifted assets. Understanding this distinction helps you make informed decisions for your estate planning.

One major mistake is not clearly defining the trust's purpose and beneficiaries. Parents often overlook the need for detailed instructions on how the trust should be managed and distributed. By understanding how to structure a gift real grantor blank with a trust, you can avoid confusion and ensure your wishes are honored.

Yes, form 709 must be filed if you make a gift exceeding the annual exclusion amount. This form reports gifts made during the year and helps determine your lifetime gift tax exemption. Filling it out properly ensures compliance with IRS regulations when utilizing a gift real grantor blank with a trust.