Qualified Debt With Income Ratio

Description

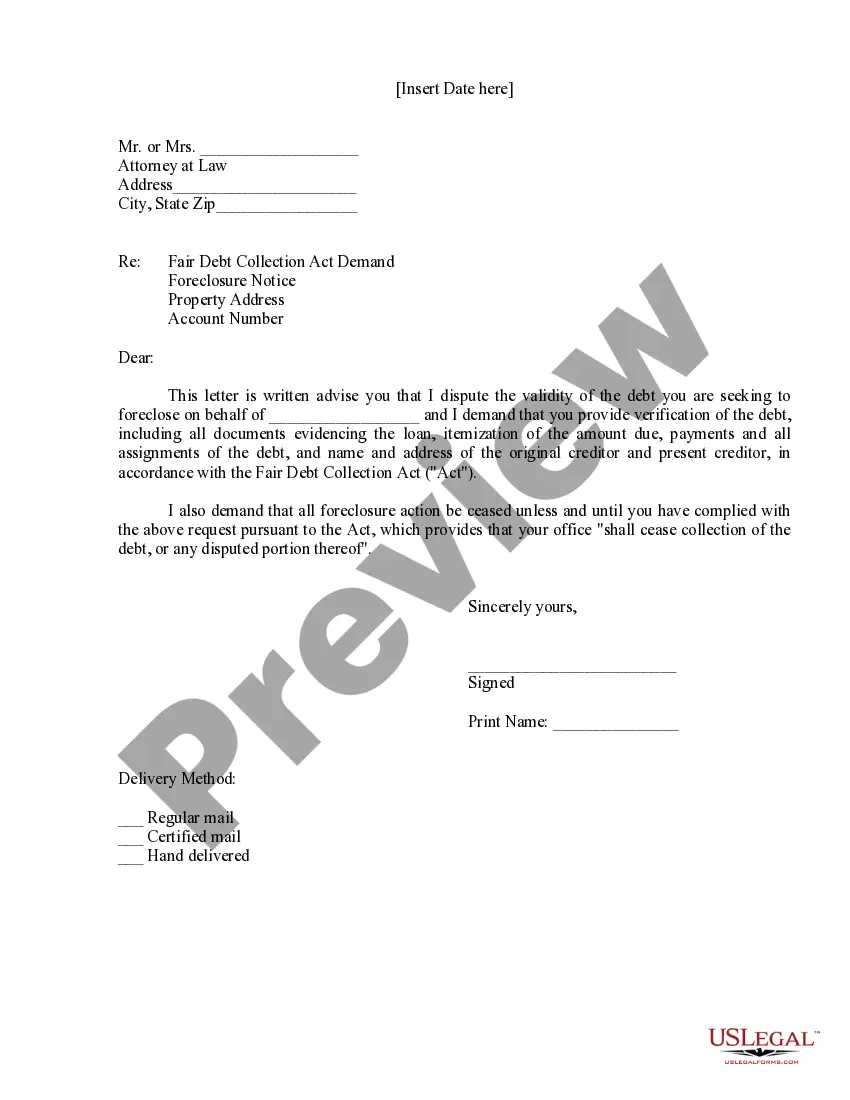

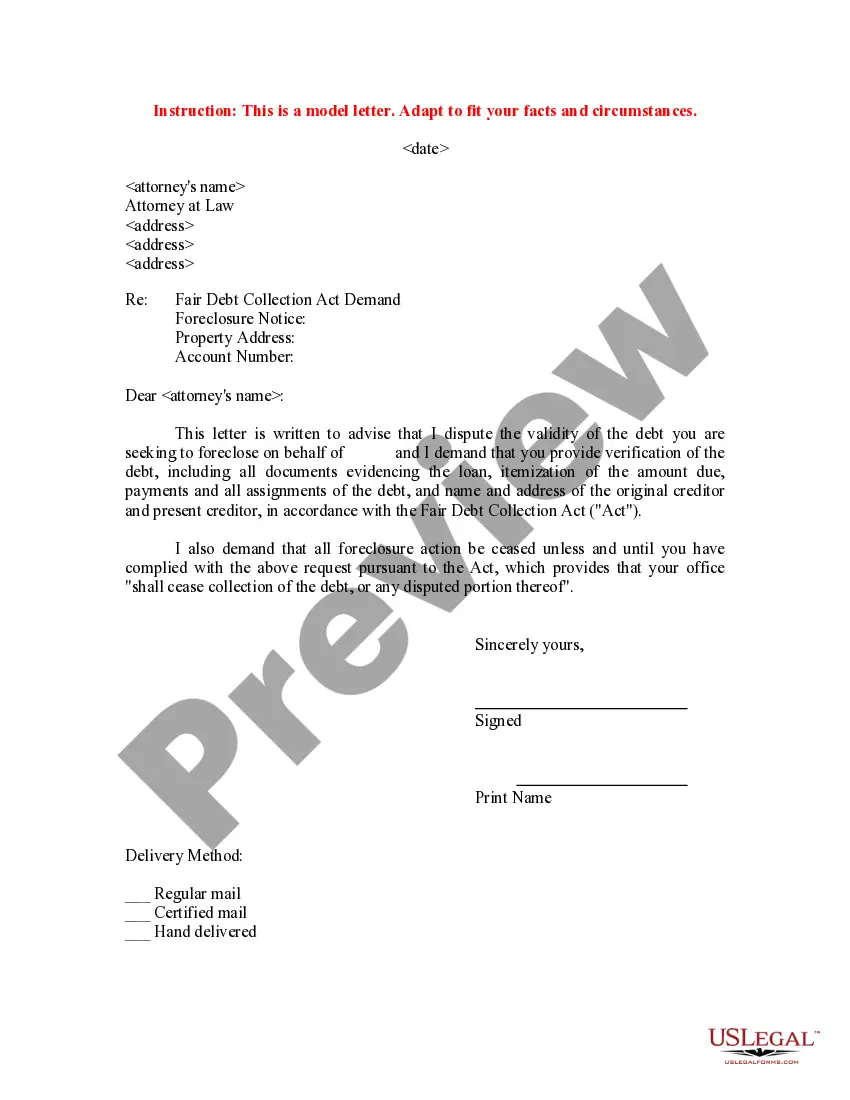

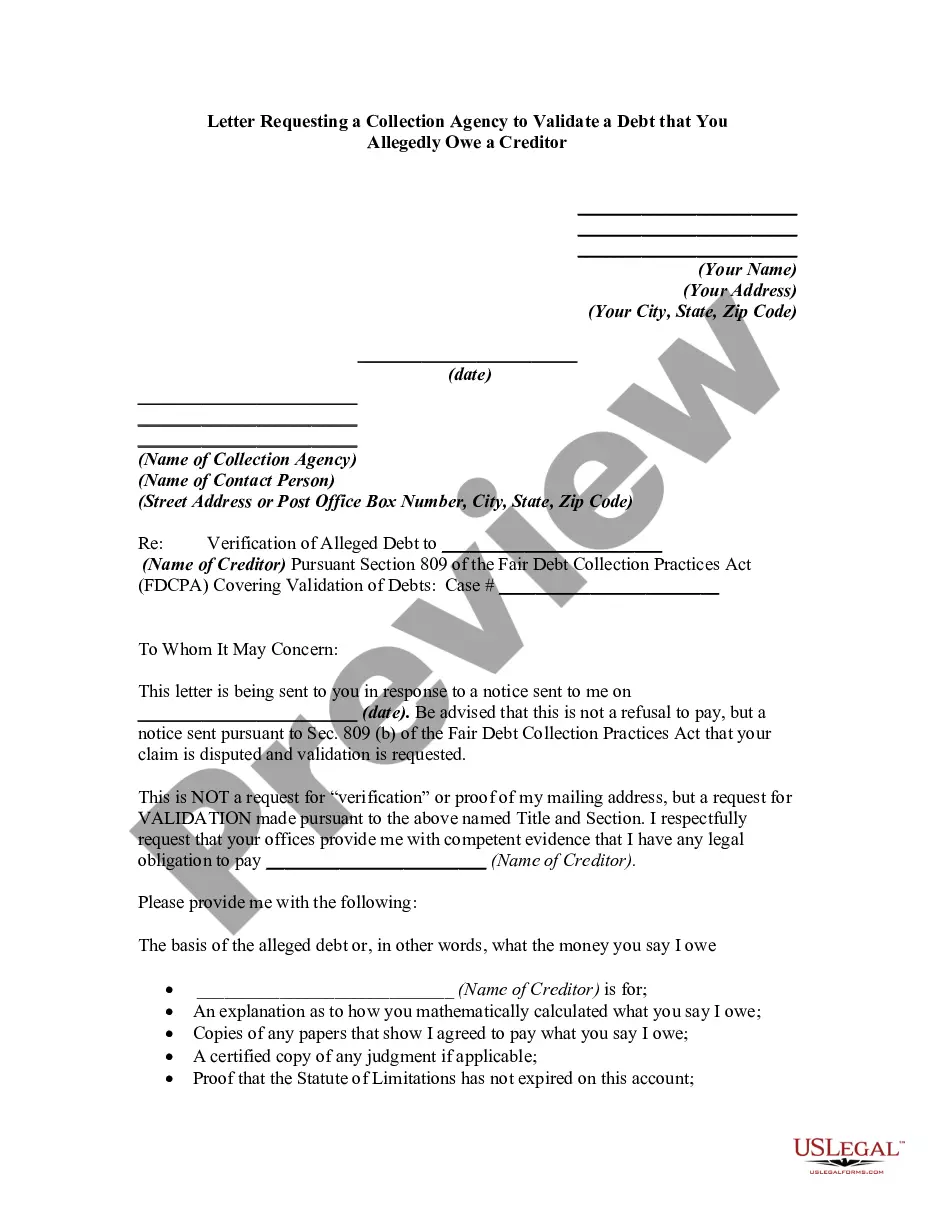

How to fill out Qualified Written RESPA Request To Dispute Or Validate Debt?

Acquiring legal document samples that comply with federal and state regulations is essential, and the internet provides numerous options to select from.

However, what’s the purpose of spending time searching for the properly drafted Qualified Debt With Income Ratio sample online if the US Legal Forms online library already has such templates gathered in one location.

US Legal Forms is the largest online legal repository with over 85,000 fillable templates created by lawyers for any business and personal circumstance. They are easy to navigate, with all documents categorized by state and intended use. Our experts stay updated on legislative changes, ensuring you can always trust that your documents are current and compliant when obtaining a Qualified Debt With Income Ratio from our site.

All documents you find through US Legal Forms are reusable. To redownload and complete previously saved forms, access the My documents section in your account. Take advantage of the most comprehensive and user-friendly legal document service!

- Review the template using the Preview option or through the text outline to ensure it satisfies your needs.

- Search for an alternative sample using the search feature at the top of the page if necessary.

- Click Buy Now once you’ve found the correct form and select a subscription option.

- Create an account or sign in and process your payment through PayPal or a credit card.

- Choose the most suitable format for your Qualified Debt With Income Ratio and download it.

Form popularity

FAQ

In order to exclude non-mortgage or mortgage debts from the borrower's DTI ratio, the lender must obtain the most recent 12 months' cancelled checks (or bank statements) from the other party making the payments that document a 12-month payment history with no delinquent payments.

How to get a loan with a high debt-to-income ratio Try a more forgiving program. Different programs come with varying DTI limits. ... Restructure your debts. Sometimes, you can reduce your ratios by refinancing or restructuring debt. ... Pay down the right accounts. ... Cash-out refinancing. ... Get a lower mortgage rate.

How do I calculate my debt-to-income ratio? To calculate your DTI, you add up all your monthly debt payments and divide them by your gross monthly income. Your gross monthly income is generally the amount of money you have earned before your taxes and other deductions are taken out.

Front-end DTI only includes housing-related expenses. This is calculated using your current monthly mortgage or rent payment, including property taxes and homeowners insurance as well as any applicable homeowners association dues.

35% or less: Looking Good - Relative to your income, your debt is at a manageable level. You most likely have money left over for saving or spending after you've paid your bills. Lenders generally view a lower DTI as favorable.