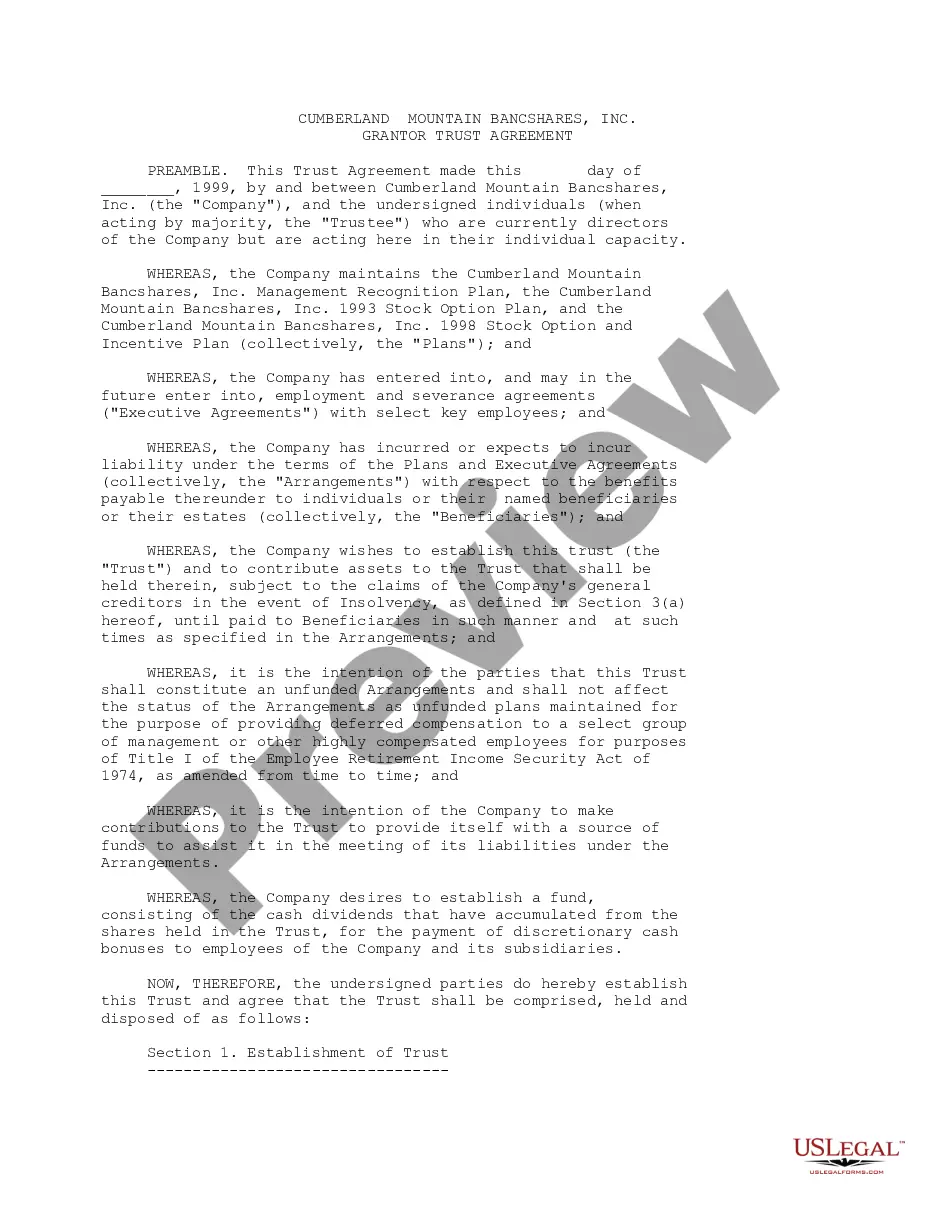

Grantor Trust Agreement Foreign Beneficiary

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

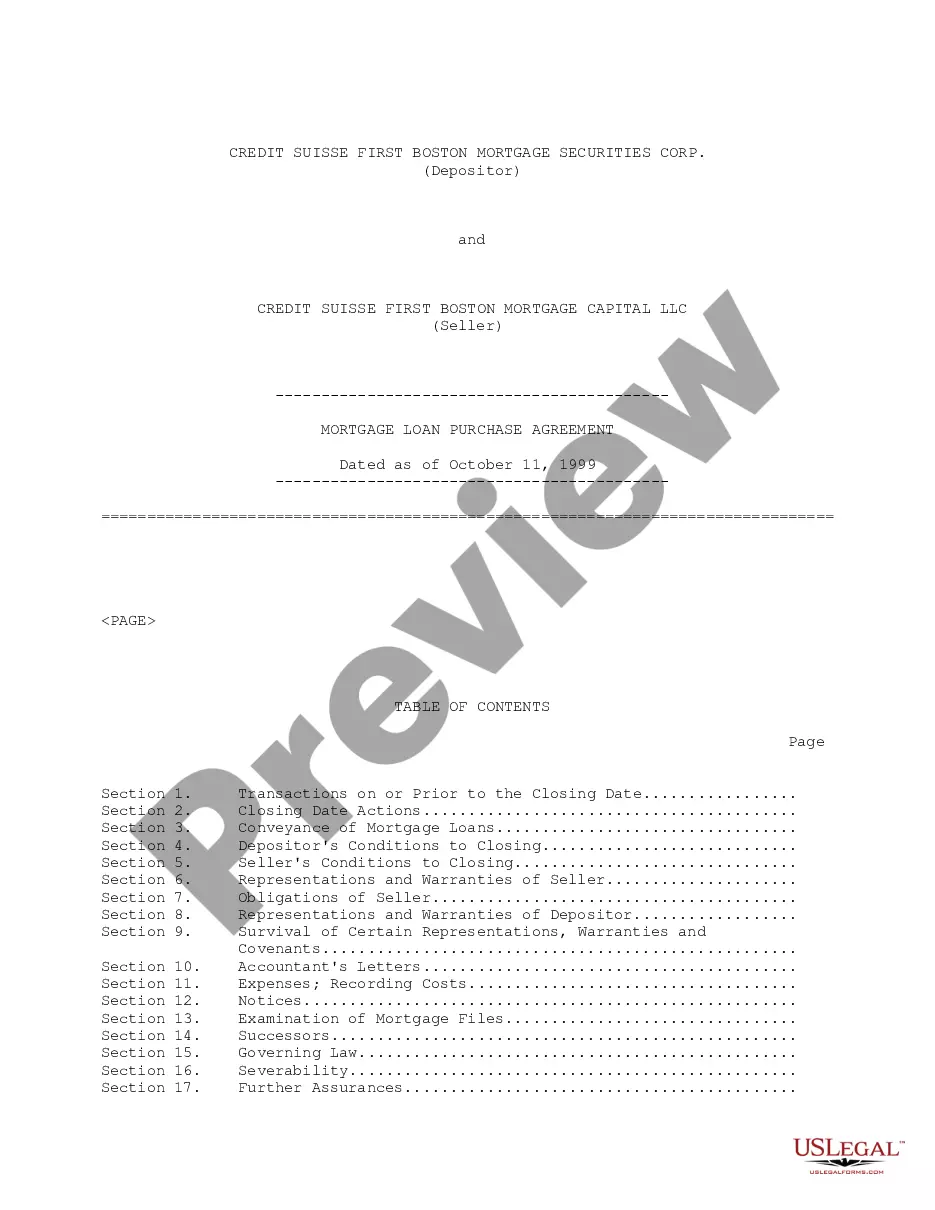

How to fill out Grantor Trust Agreement Between Credit Suisse First Boston Mortgage Securities Corp., Washington Mutual Bank FA And Bank One, National Assoc.?

Acquiring legal forms that comply with federal and local laws is essential, and the internet provides countless choices to choose from.

However, what is the purpose of spending time searching for the suitable Grantor Trust Agreement Foreign Beneficiary template online if the US Legal Forms digital library already has those forms conveniently gathered in one location.

US Legal Forms is the premier online legal resource featuring over 85,000 editable templates created by attorneys for any professional and personal circumstance.

Utilize the Preview feature or the text outline to evaluate the template to confirm it meets your requirements.

- They are easy to navigate, with all documents categorized by state and intended use.

- Our experts stay informed on legal updates, so you can always trust that your form is current and compliant when obtaining a Grantor Trust Agreement Foreign Beneficiary from our platform.

- Acquiring a Grantor Trust Agreement Foreign Beneficiary is swift and straightforward for both existing and new users.

- If you already possess an account with an active subscription, Log In and download the document sample you need in your desired format.

- If you are unfamiliar with our site, follow the steps outlined below.

Form popularity

FAQ

A foreign grantor trust is considered both a foreign trust and a grantor trust. Neither the trust nor the settlor is subject to U.S. income tax on non-U.S. trust income while the settlor is alive unless the trust holds U.S. situs assets at the settlor's death.

Interest income earned by the trust is deductible if distributed to a foreign beneficiary but because the beneficiary is a nonresident alien, he will not be subject to U.S. income tax on the distribution. Therefore, the income is not subject to withholding tax (see Rev. Rul.

In addition to the withholding requirement, naming a beneficiary who resides in a foreign country may allow the foreign country to tax the property and accounts of the trust. In most cases, a foreign person is subject to US tax on its US source income.

A Foreign Grantor Trust is a common type of trust that the grantor controls on behalf of the beneficiary. This is in comparison to a non-grantor trust, in which the original grantor may no longer have control over the trust (direct or indirect), absent some very creative planning.

Form 3520 must be filed by the due date (including extensions) of the individual's Form 1040. The US owner must attach to a copy of the ?Foreign Grantor Trust Owner Statement? received from the Trustee to Form 3520.