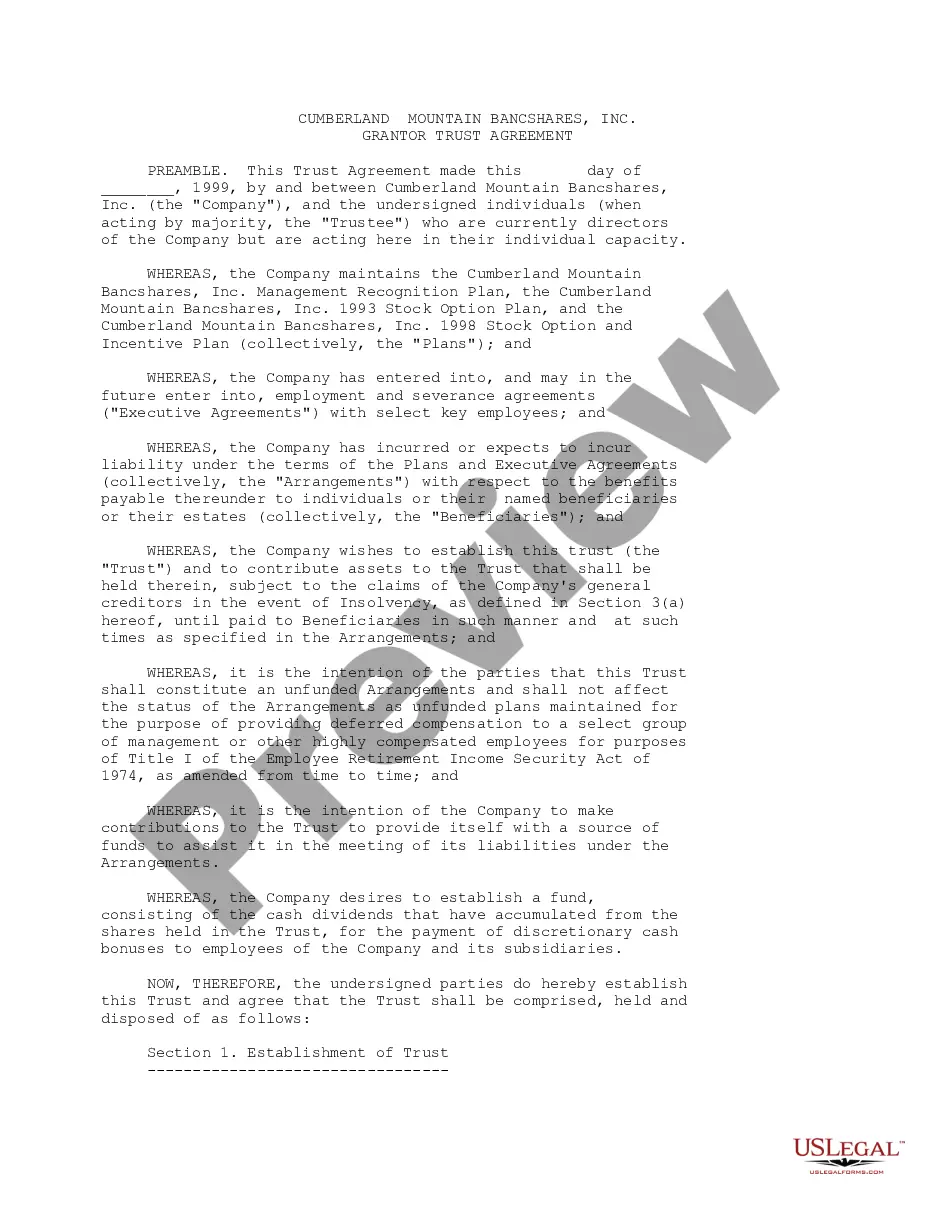

Grantor Trust Agreement Foreign

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

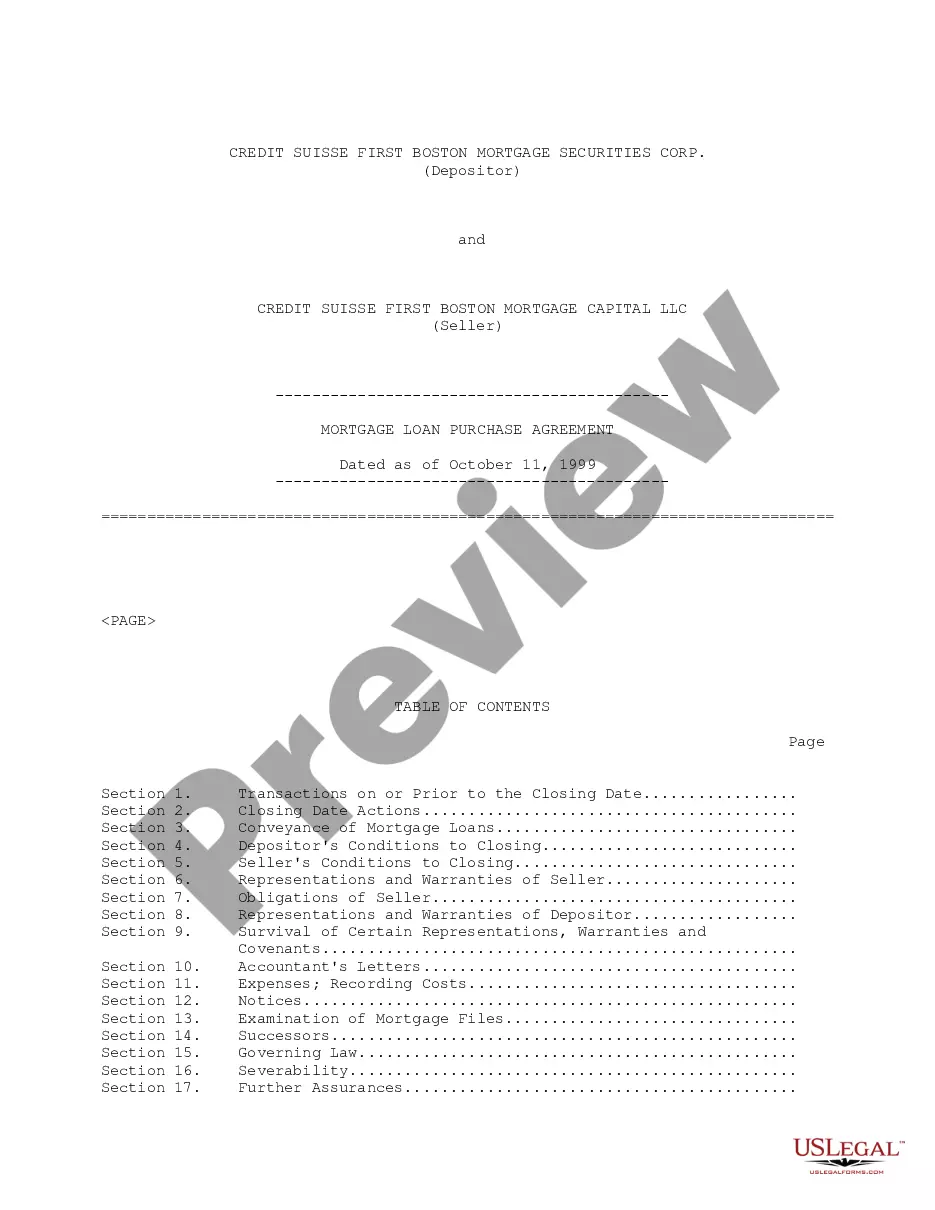

How to fill out Grantor Trust Agreement Between Credit Suisse First Boston Mortgage Securities Corp., Washington Mutual Bank FA And Bank One, National Assoc.?

It’s clear that you cannot transform into a legal specialist instantly, nor can you swiftly learn how to formulate a Grantor Trust Agreement Foreign without possessing a specialized expertise.

Creating legal documents is a lengthy process that necessitates specific training and abilities. So why not delegate the formulation of the Grantor Trust Agreement Foreign to the experts.

With US Legal Forms, one of the largest legal document repositories, you can obtain everything from court paperwork to templates for internal business communication.

If you require additional forms, initiate your search again.

Create a free account and choose a subscription plan to purchase the document. Select Buy now. Once the transaction is completed, you can receive the Grantor Trust Agreement Foreign, fill it out, print it, and deliver it physically or via mail to the necessary individuals or entities.

- We understand how crucial compliance and adherence to federal and state regulations are.

- That’s why all templates on our website are location-specific and current.

- Here’s how to start using our platform to acquire the document you need within minutes.

- Identify the document you require using the search bar located at the top of the page.

- Explore it (if this option is available) and review the supporting description to determine if the Grantor Trust Agreement Foreign aligns with your needs.

Form popularity

FAQ

A foreign trust is considered to be a grantor trust if it is revocable. It is also considered a grantor trust if it is irrevocable, but the settlor and the settlor's spouse are the only ones receiving distributions during the life of the settlor.

The primary IRS reporting vehicle for a foreign grantor trust is a Form 3520-A.

A trust that isn't a domestic trust is treated as a foreign trust. If you are the trustee of a foreign trust, file Form 1040-NR instead of Form 1041. Also, a foreign trust with a U.S. owner generally must file Form 3520-A, Annual Information Return of Foreign Trust With a U.S. Owner.

The main form is the Form 3520-A ? which is used when a US person is an owner of a foreign trust. The other form is Form 3520, which is used when a person has ownership of a foreign trust, engages in certain transactions with the foreign trust, or receives a distribution from the foreign trust.

A foreign trust is also considered a grantor trust for US income tax purposes when a US grantor makes a gratuitous transfer to a foreign trust which has one or more US beneficiaries or potential US beneficiaries of any portion of the trust.