Property Exempt Form For Hotels

Description

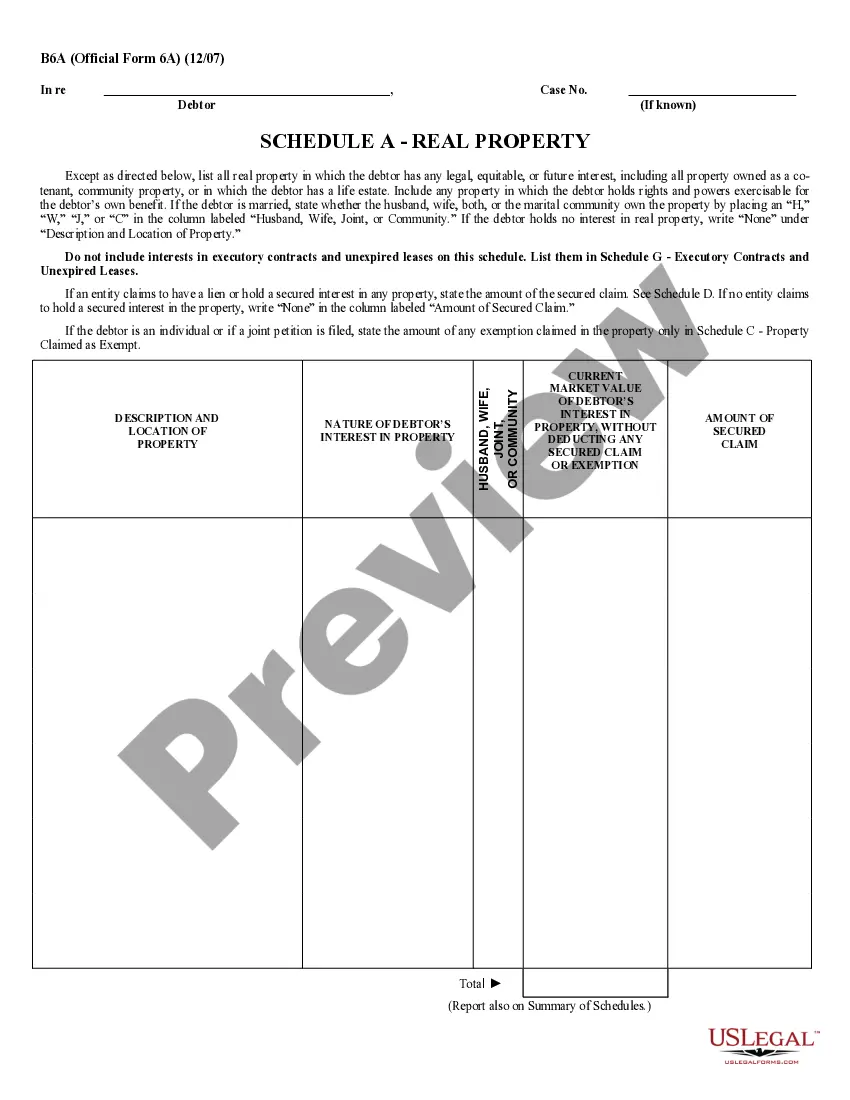

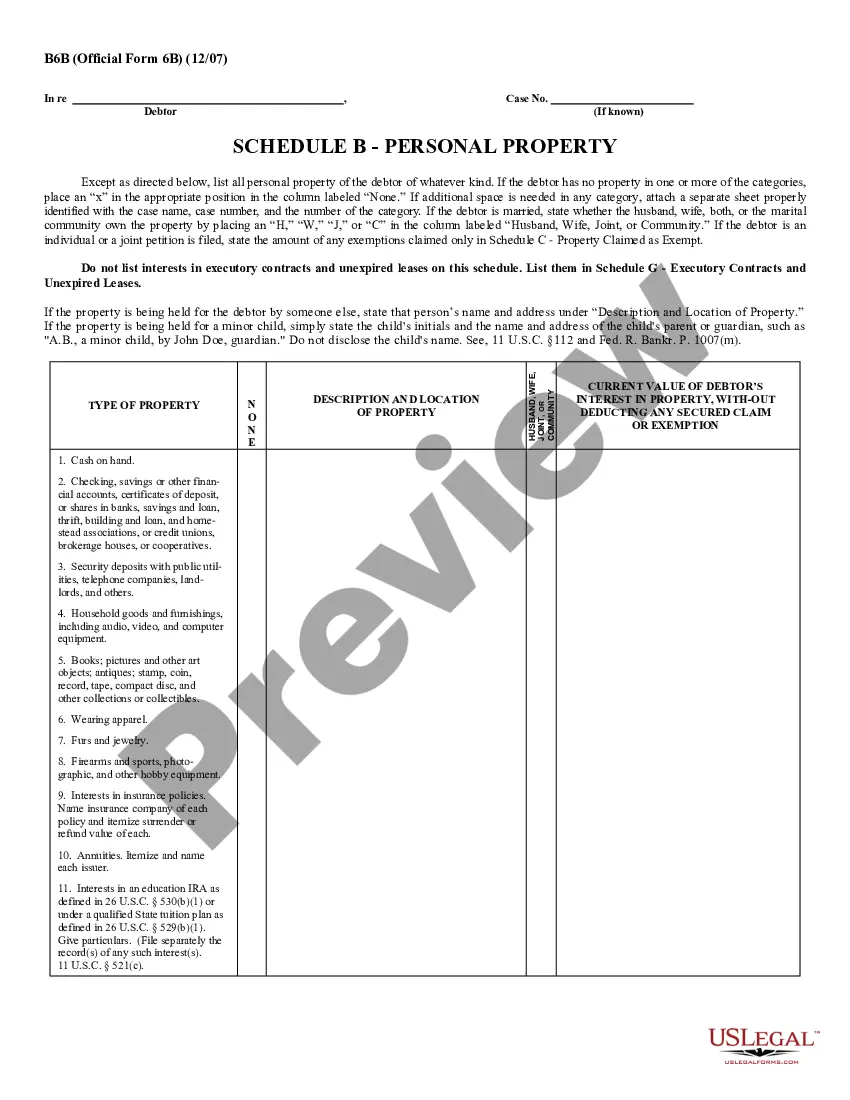

How to fill out Property Claimed As Exempt - Schedule C - Form 6C - Post 2005?

Getting a go-to place to access the most recent and relevant legal samples is half the struggle of working with bureaucracy. Discovering the right legal documents needs precision and attention to detail, which is why it is very important to take samples of Property Exempt Form For Hotels only from trustworthy sources, like US Legal Forms. A wrong template will waste your time and hold off the situation you are in. With US Legal Forms, you have very little to be concerned about. You may access and see all the information regarding the document’s use and relevance for the circumstances and in your state or county.

Take the listed steps to finish your Property Exempt Form For Hotels:

- Make use of the library navigation or search field to find your template.

- Open the form’s information to see if it matches the requirements of your state and county.

- Open the form preview, if there is one, to make sure the form is the one you are interested in.

- Resume the search and find the appropriate template if the Property Exempt Form For Hotels does not match your requirements.

- When you are positive regarding the form’s relevance, download it.

- If you are a registered customer, click Log in to authenticate and gain access to your selected forms in My Forms.

- If you do not have an account yet, click Buy now to obtain the form.

- Pick the pricing plan that fits your requirements.

- Proceed to the registration to complete your purchase.

- Complete your purchase by selecting a payment method (bank card or PayPal).

- Pick the file format for downloading Property Exempt Form For Hotels.

- Once you have the form on your device, you may change it using the editor or print it and finish it manually.

Remove the hassle that accompanies your legal documentation. Check out the comprehensive US Legal Forms library to find legal samples, examine their relevance to your circumstances, and download them on the spot.

Form popularity

FAQ

The stay is exempt from PA hotel occupancy taxes if the federal government pays for the room directly at the time of the stay. The stay is also exempt from PA hotel occupancy taxes if the employee pays for the room at the time of stay and is later reimbursed by the government.

Guests who occupy a hotel room for 30 or more consecutive days with no payment interruption are considered permanent residents and are exempt from hotel tax.

The Transient Occupancy Tax (TOT) is a tax of 12% of the rent charged to transient guests in hotels/motels, including properties rented through home sharing services like Airbnb, located in the unincorporated areas of Los Angeles County. The TOT is commonly known as a ?bed tax?.

Renting the room Give the completed Form ST-129 to the operator of the hotel or motel upon check in or when you are checking out. You must also provide the operator with proper identification. Sign and date the exemption certificate.

Any person who has a written agreement with the operator, entered into within the first thirty (30) days of the person's occupancy, which states the person will stay for more than thirty (30) consecutive calendar days is exempt from the TOT, for the first 30 days of the person's stay.