Acuerdos Prenupciales Formato

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

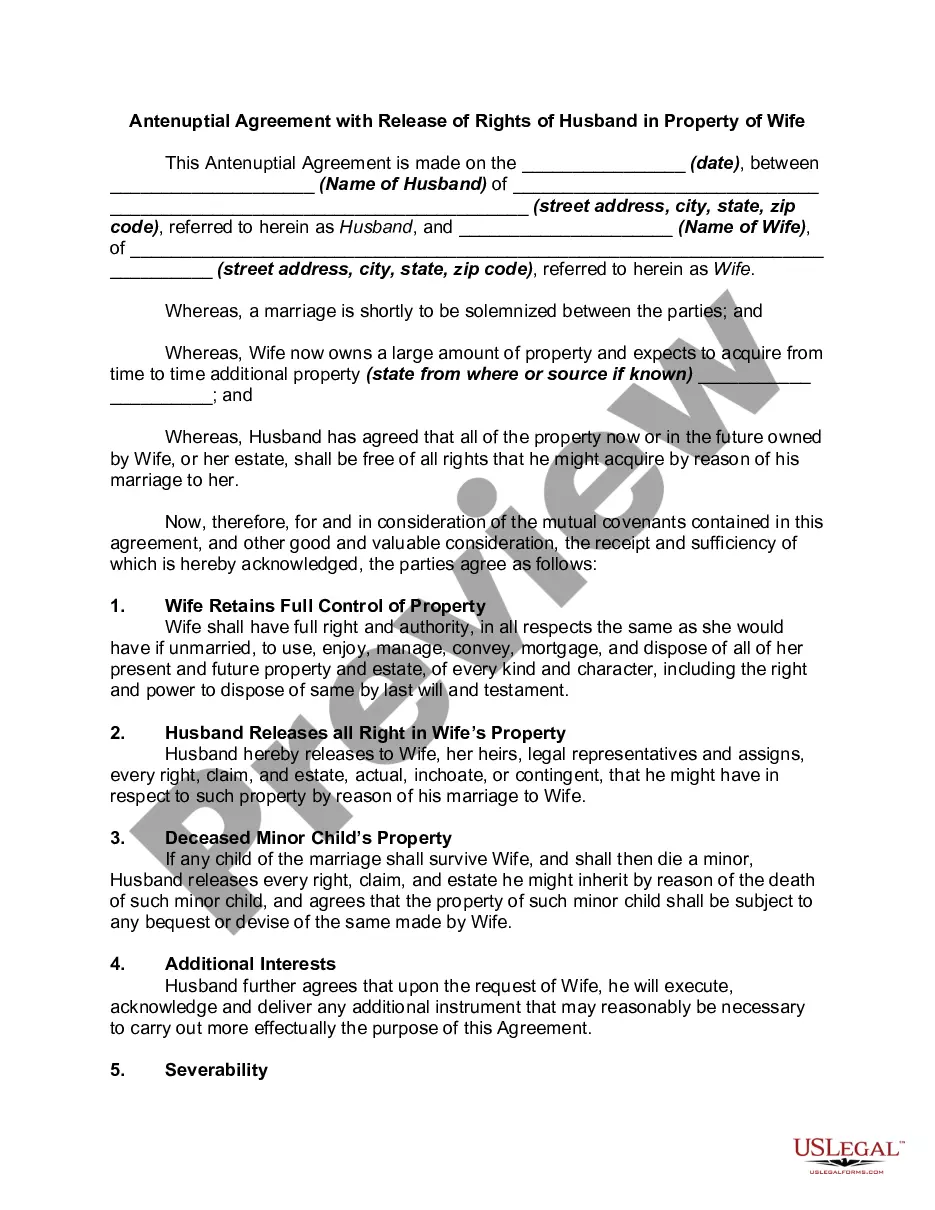

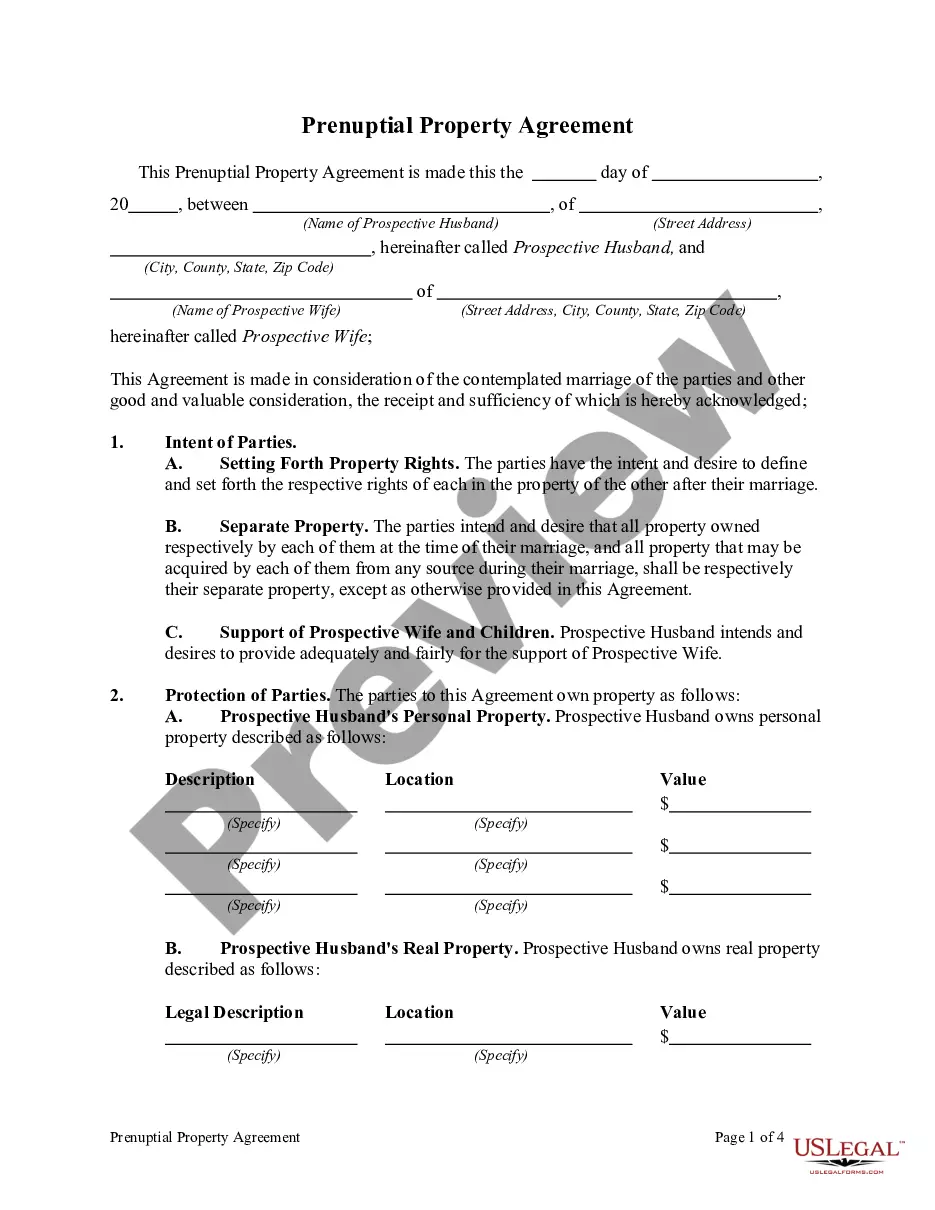

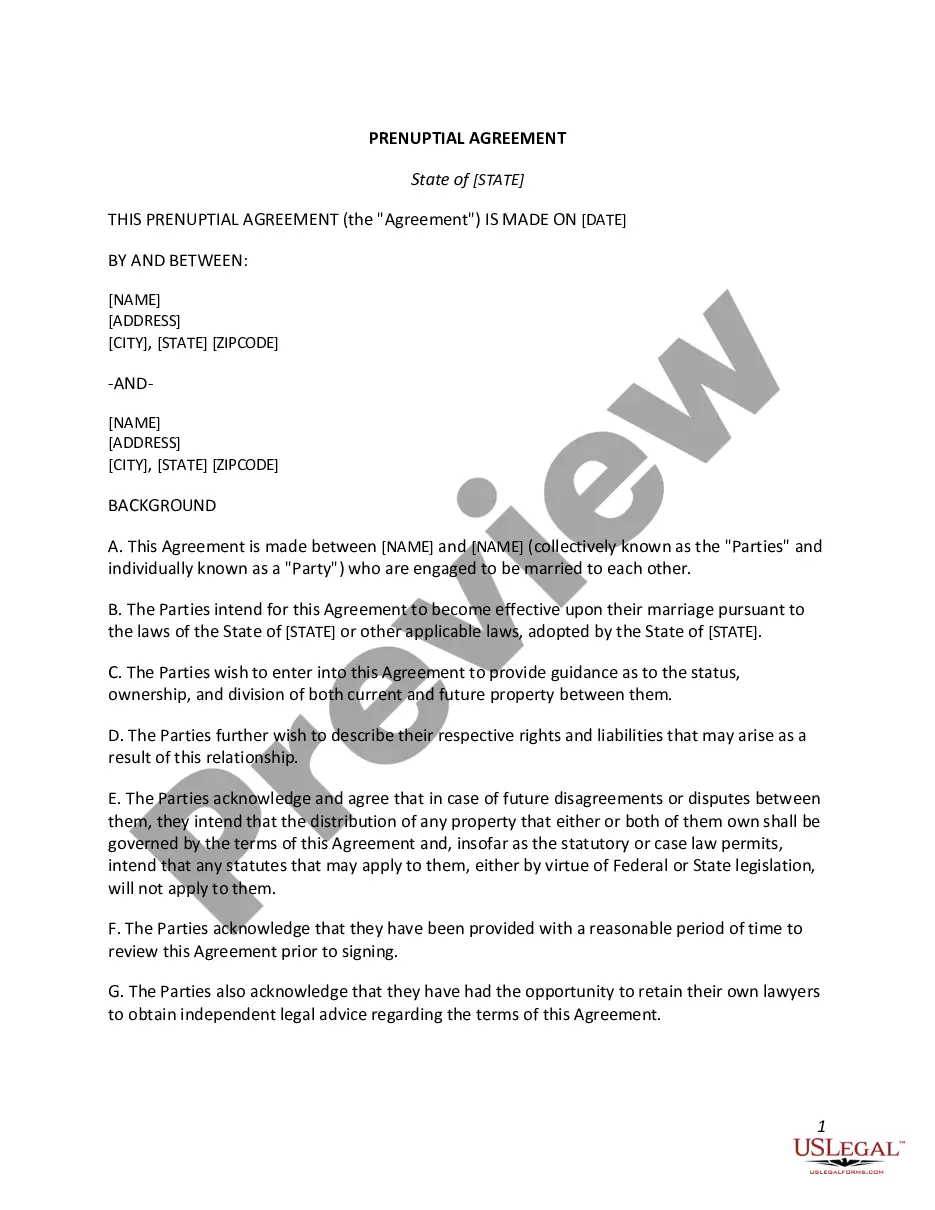

How to fill out Prenuptial Agreements - General Comments On The Negotiating, Drafting And Execution Of Prenuptial Agreements?

Locating a reliable resource to obtain the latest and suitable legal templates is a significant part of navigating bureaucracy. Securing the appropriate legal paperwork requires accuracy and meticulousness, which is why it is crucial to source Acuerdos Prenupciales Formato samples solely from reputable providers, such as US Legal Forms. An incorrect template could waste your time and hinder your ongoing situation. With US Legal Forms, your concerns are minimized. You can access and review all the details concerning the document’s utility and pertinence for your situation and within your state or county.

Follow the outlined steps to complete your Acuerdos Prenupciales Formato.

Eliminate the hassle associated with your legal paperwork. Investigate the vast US Legal Forms database where you can find legal templates, assess their relevance to your circumstances, and download them promptly.

- Use the library navigation or search bar to locate your template.

- Examine the form’s information to ensure it meets the requirements of your state and county.

- View the form preview, if available, to confirm that the template complies with your search.

- Return to the search and look for the correct document if the Acuerdos Prenupciales Formato does not satisfy your needs.

- If you are certain about the form’s applicability, download it.

- When you are an authorized user, click Log in to verify and access your chosen templates in My documents.

- If you do not have an account yet, click Buy now to acquire the template.

- Select the pricing option that best suits your needs.

- Proceed to the registration to finalize your purchase.

- Complete your purchase by choosing a payment method (credit card or PayPal).

- Select the document format for downloading Acuerdos Prenupciales Formato.

- Once the form is on your device, you can modify it with the editor or print it and fill it out manually.

Form popularity

FAQ

Creating a prenup involves several steps, including discussing finances with your partner and deciding on the terms you both agree on. Start by outlining your financial situation and consider the objectives of your agreement. Using Acuerdos prenupciales formato can streamline the drafting process, providing templates and ideas to structure your prenup. Finally, make sure both parties seek independent legal advice to validate the document.

If you owe money to someone, the person is called a creditor, and what you owe them is called a debt. The creditor generally has 3 years (4 years if the debt is owed for the sale of goods) from the date the debt becomes due to ask the court to order you to pay. A court order to pay a debt is known as a judgment.

Harassment of the debtor by the creditor ? More than 40 percent of all reported FDCPA violations involved incessant phone calls in an attempt to harass the debtor.

The Maryland Fair Debt Collection Act prohibits debt collectors and creditors from engaging in deceptive, threatening, or other abusive collection behavior. In Maryland, the federal Fair Debt Collection Practices Act (FDCPA) and state law regulate debt collectors.

Debt collectors engaging in harassment (usually with repeated calls) or using abusive language. Debt collectors threatening to contact a third party about your debt (such as a friend, family member, or employer) or otherwise improperly share information about your debt publicly.

The FDCPA prohibits debt collection companies from using abusive, unfair, or deceptive practices to collect debts from you.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take.

Here's how to remove paid collections from your credit report?or at least try to do so: Send a letter to the debt collection agency or ask via phone for this option. If the agency agrees, get the agreement in writing. Pay the debt. Follow up to make sure the debt is removed from your report.

If you feel that your rights under the Fair Debt Collections Practices Act (FDCPA) have been violated, you have the right to sue the debt collection agency. You must file within one year from the date that your rights were violated. Keep records of all contact that you have with a debt collection agency.