Limited Liability For Companies

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

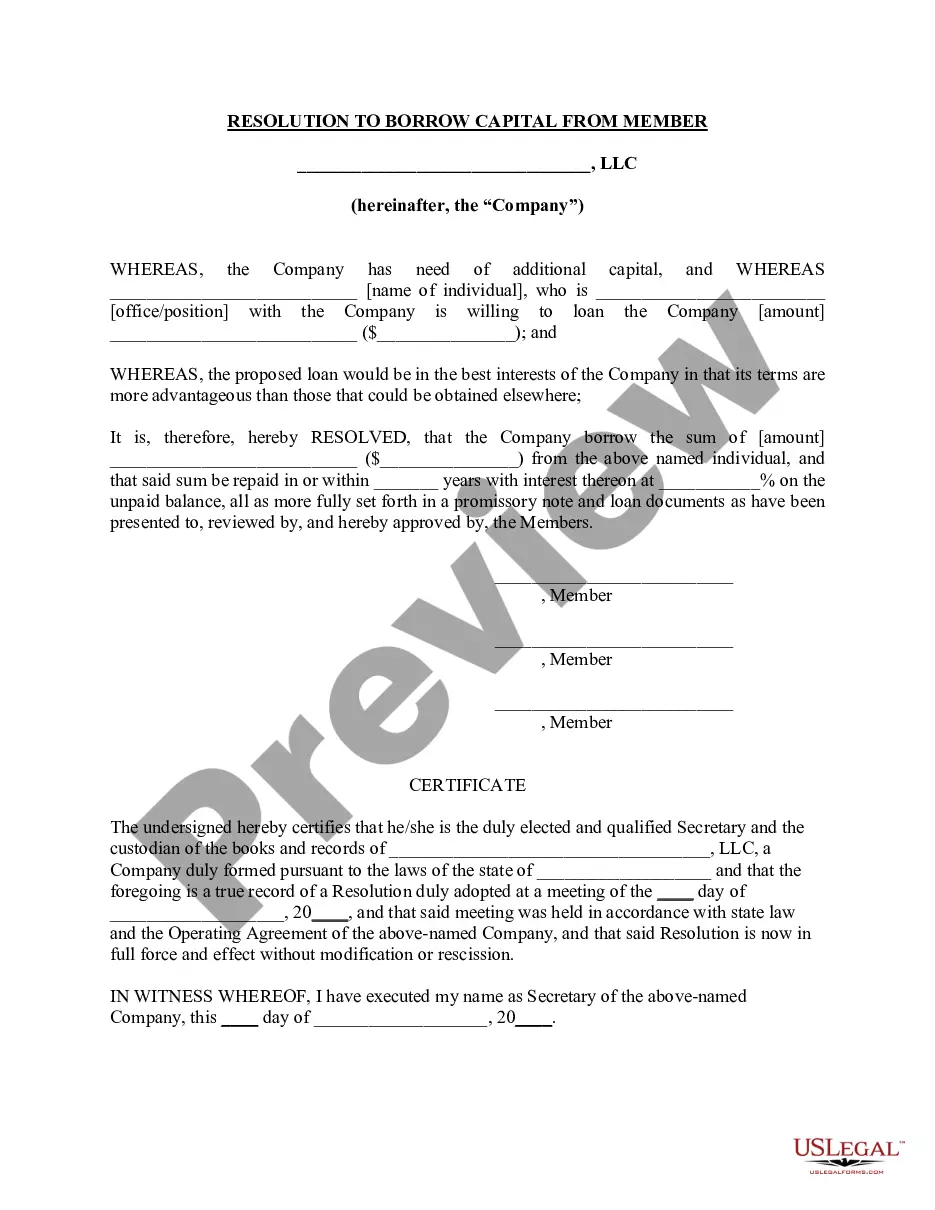

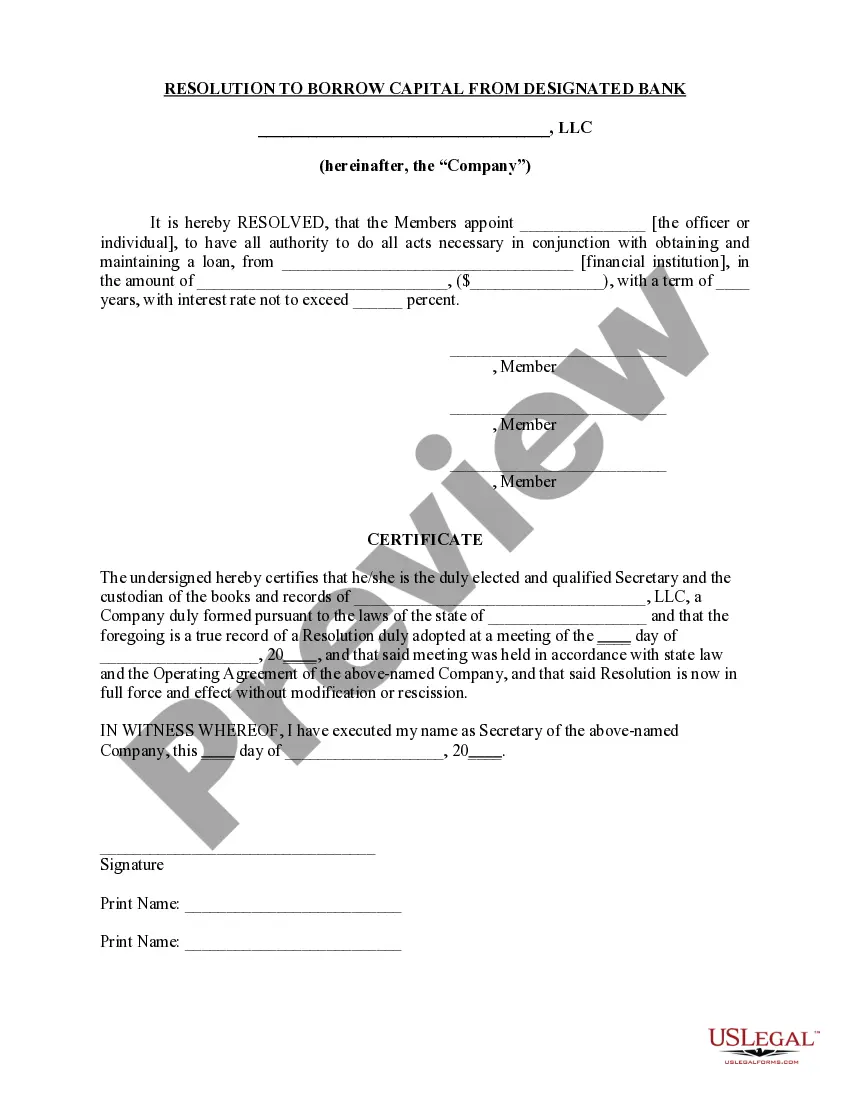

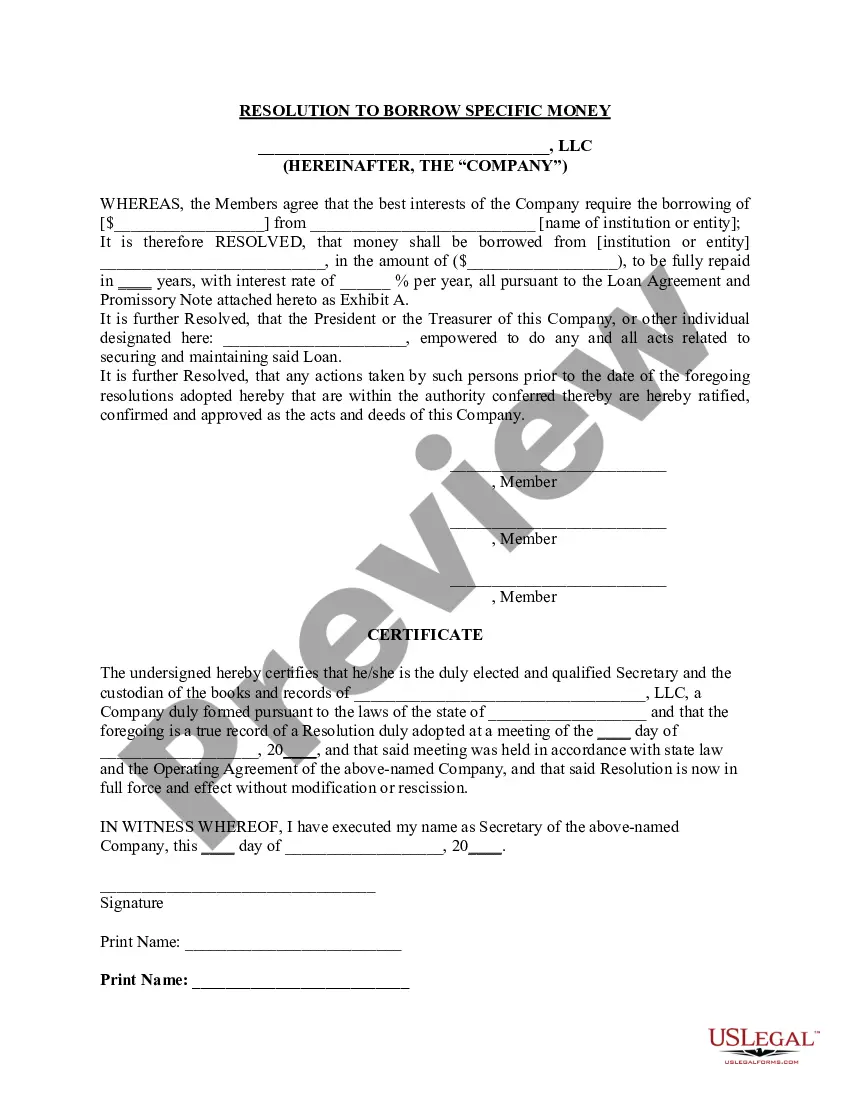

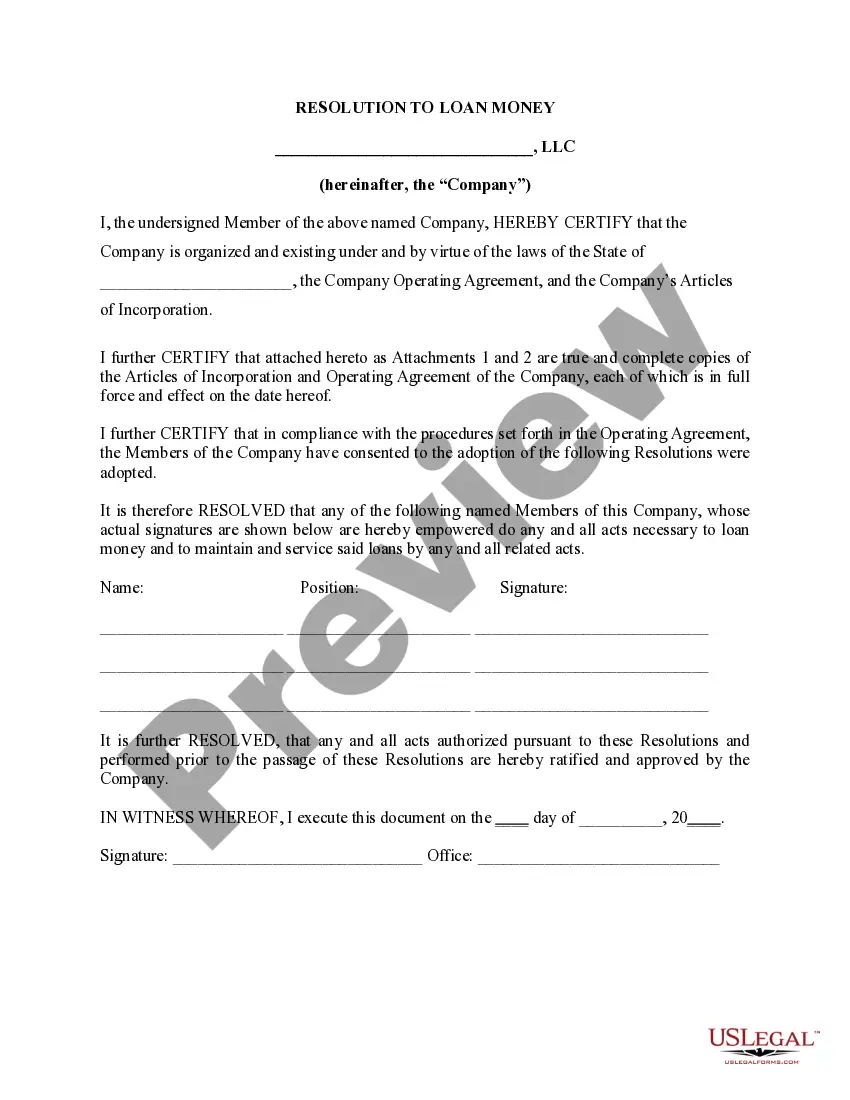

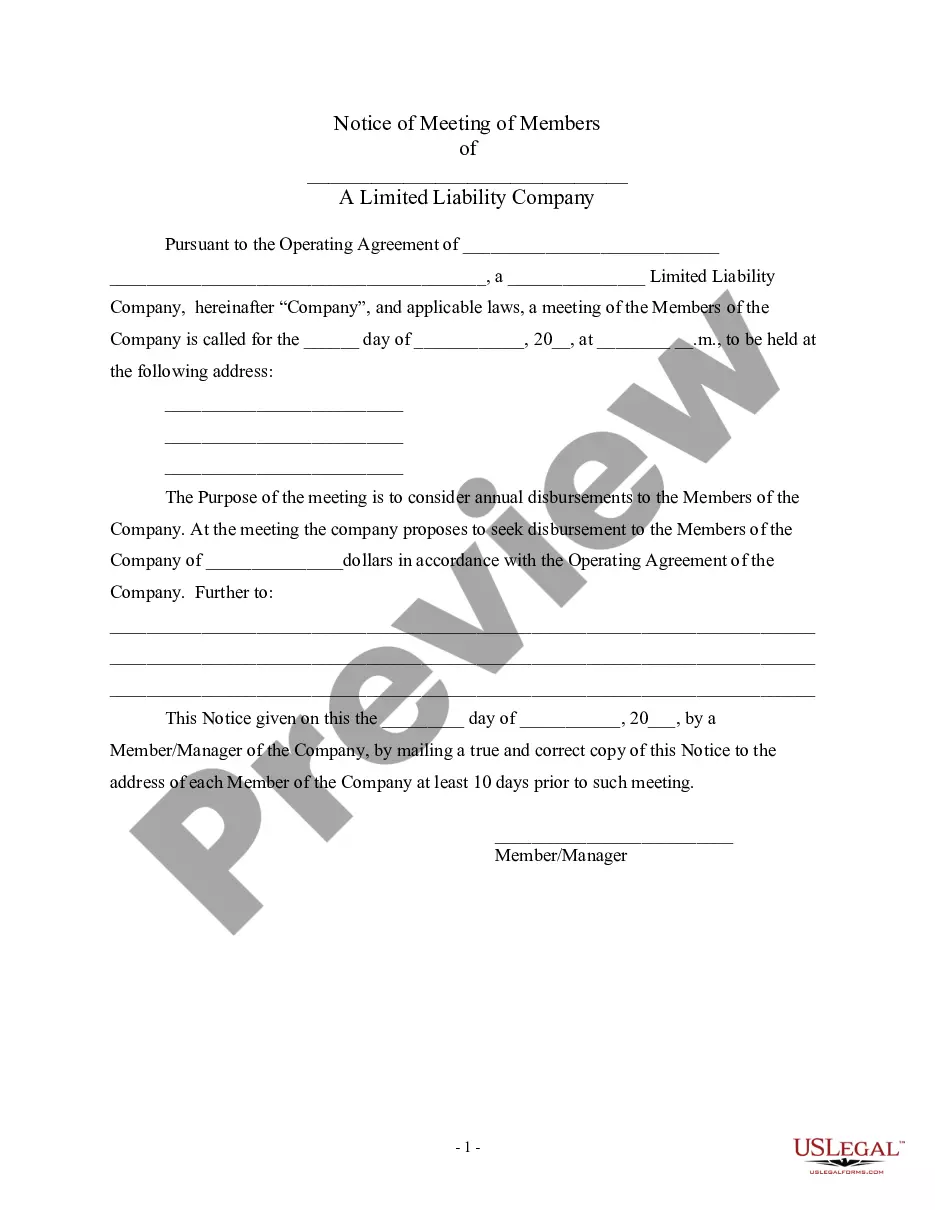

How to fill out Resolution Of Meeting Of LLC Members To Borrow Money?

- If you are a returning user, log in to your account to download your desired form template by clicking the Download button, ensuring your subscription is active.

- For first-time users, start by previewing the form and description to confirm it fits your needs and complies with local regulations.

- If you encounter any discrepancies or need a different form, utilize the Search function to find an appropriate template.

- Once you find the correct document, click on the Buy Now button and select your preferred subscription plan, creating an account if necessary.

- Complete your purchase by providing your payment information using a credit card or PayPal.

- Finally, download your form to save it on your device, and access it anytime via the My documents section in your profile.

Utilizing the robust library of over 85,000 legal forms, US Legal Forms empowers you to efficiently complete legal documents with confidence.

Don’t wait to secure your legal needs—visit US Legal Forms today and experience the simplicity of accessing tailored legal solutions.

Form popularity

FAQ

Corporations have limited liability because they are recognized as separate legal entities. This means that the corporation itself holds the responsibility for its debts and liabilities, not the individual owners or shareholders. As a result, when a corporation encounters legal or financial trouble, the personal assets of shareholders remain protected, which exemplifies the concept of limited liability for companies.

To determine if a company has limited liability status, you can look for certain designations in its name, such as 'LLC' or 'Inc.' Additionally, you can access the state’s business registry, which typically provides information about the company's structure. Understanding whether a company exhibits limited liability for companies is important for assessing financial risk.

An example of limited liability in a corporation is a shareholder's protection from losing personal assets if the corporation faces bankruptcy. If the corporation incurs debts or lawsuits, only the corporation's assets are at risk, not the shareholders'. This principle of limited liability for companies ensures that investors can participate without personal financial risk.

A key benefit of a limited liability company is its flexibility in management and taxation. Unlike a corporation, an LLC can choose its tax structure, allowing for pass-through taxation without double taxation. Additionally, limited liability for companies protects members' personal assets from business debts, providing peace of mind and financial security.

Limited liability companies typically file IRS Form 1065, which is an informational return for partnerships. This form reports the income, deductions, gains, and losses from the LLC's operations. However, if your LLC chooses to be taxed as a corporation, you would need to file Form 1120 instead. Understanding your tax obligations under limited liability for companies is essential for compliance.

Choosing between an LLC and an LP depends on your business goals and structure. An LLC offers limited liability for all its members, while an LP includes both general and limited partners, with varying levels of liability. If you prioritize personal asset protection, an LLC may be the better choice. However, if you seek to attract investors with different levels of involvement, an LP might suit your needs.

While limited liability for companies offers benefits, an LLC can have drawbacks, such as self-employment taxes. Owners often face higher tax liabilities compared to traditional corporations. Additionally, the limited liability may not protect owners from personal guarantees on loans. Understanding these aspects can help you make informed decisions when choosing a business structure.

Limited liability for companies protects owners from being personally responsible for the company's debts. This means that personal assets remain safe even if the business faces financial issues. It encourages investment and entrepreneurship because individuals can take business risks without the fear of losing their homes or savings. Overall, this structure enhances the attractiveness of starting a business.

Yes, you can file your LLC as a separate entity from your personal finances. This separation is a key benefit of forming an LLC, as it creates limited liability for companies. By doing so, you better protect your personal assets from business liabilities, making it a wise decision for many entrepreneurs.

Failing to file taxes for your LLC can lead to penalties, interest, and potential legal complications. If your business generates income, the IRS expects you to report that on your taxes, even if your LLC is inactive. It's essential to manage your obligations carefully to maintain your limited liability for companies.