Defined Benefit Plan Form Withdrawal Rules

Description

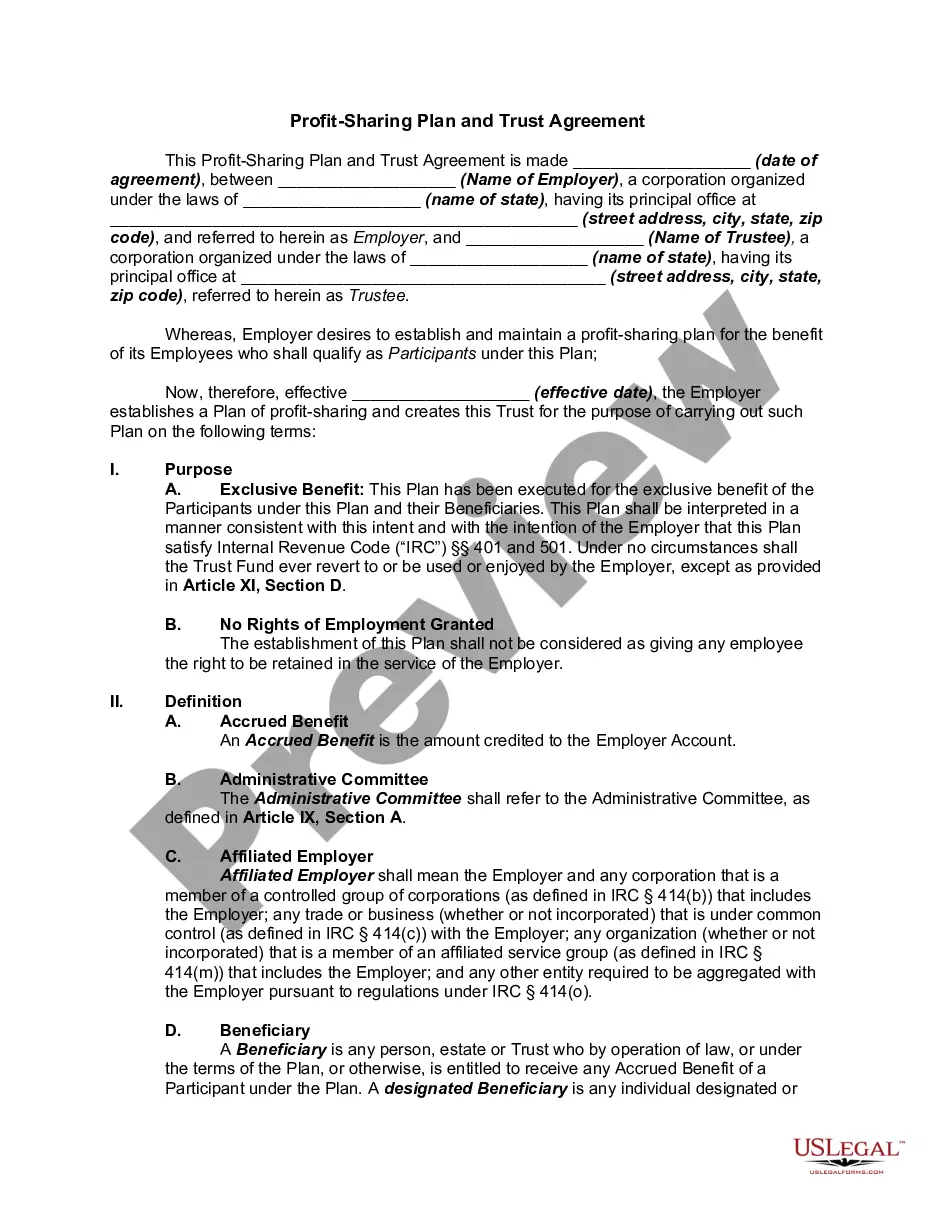

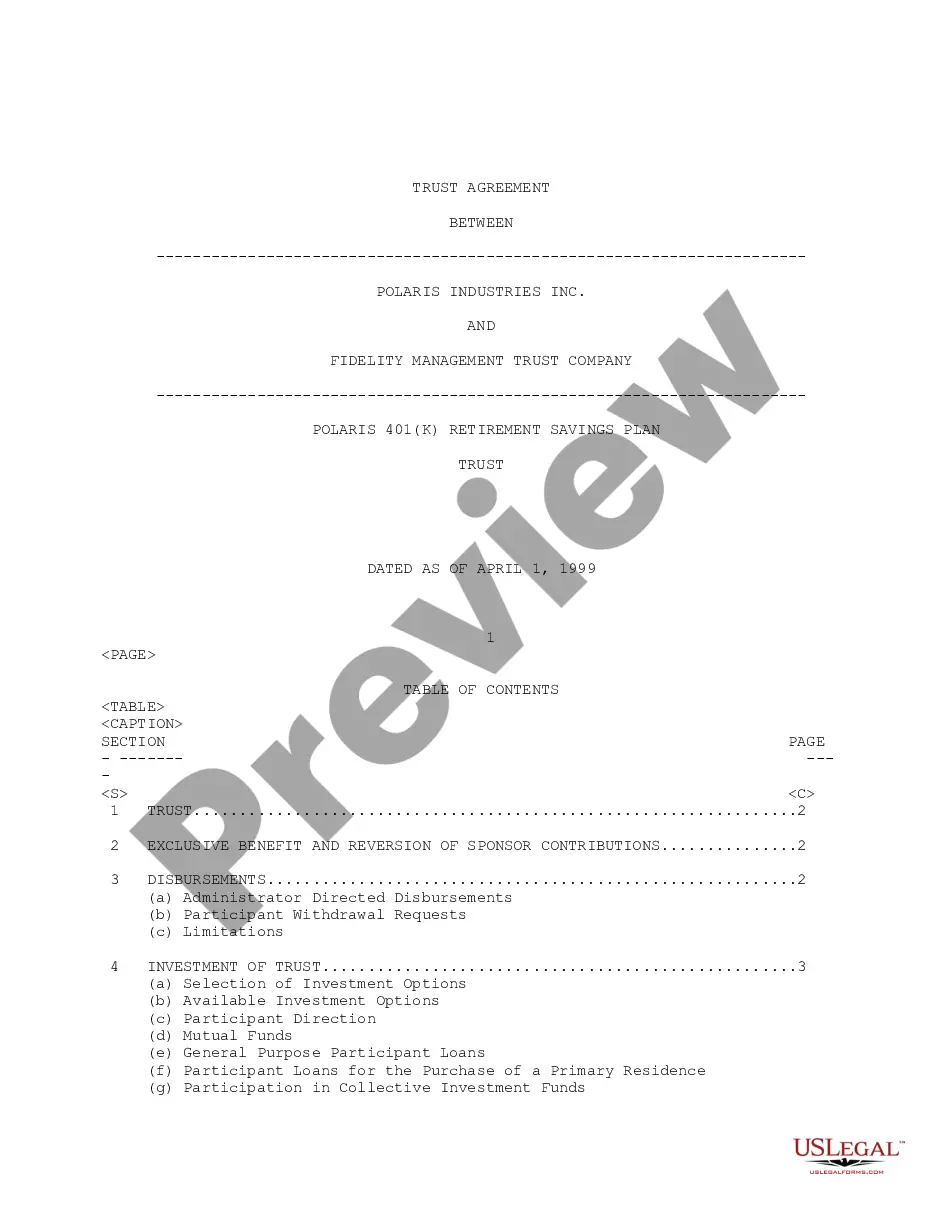

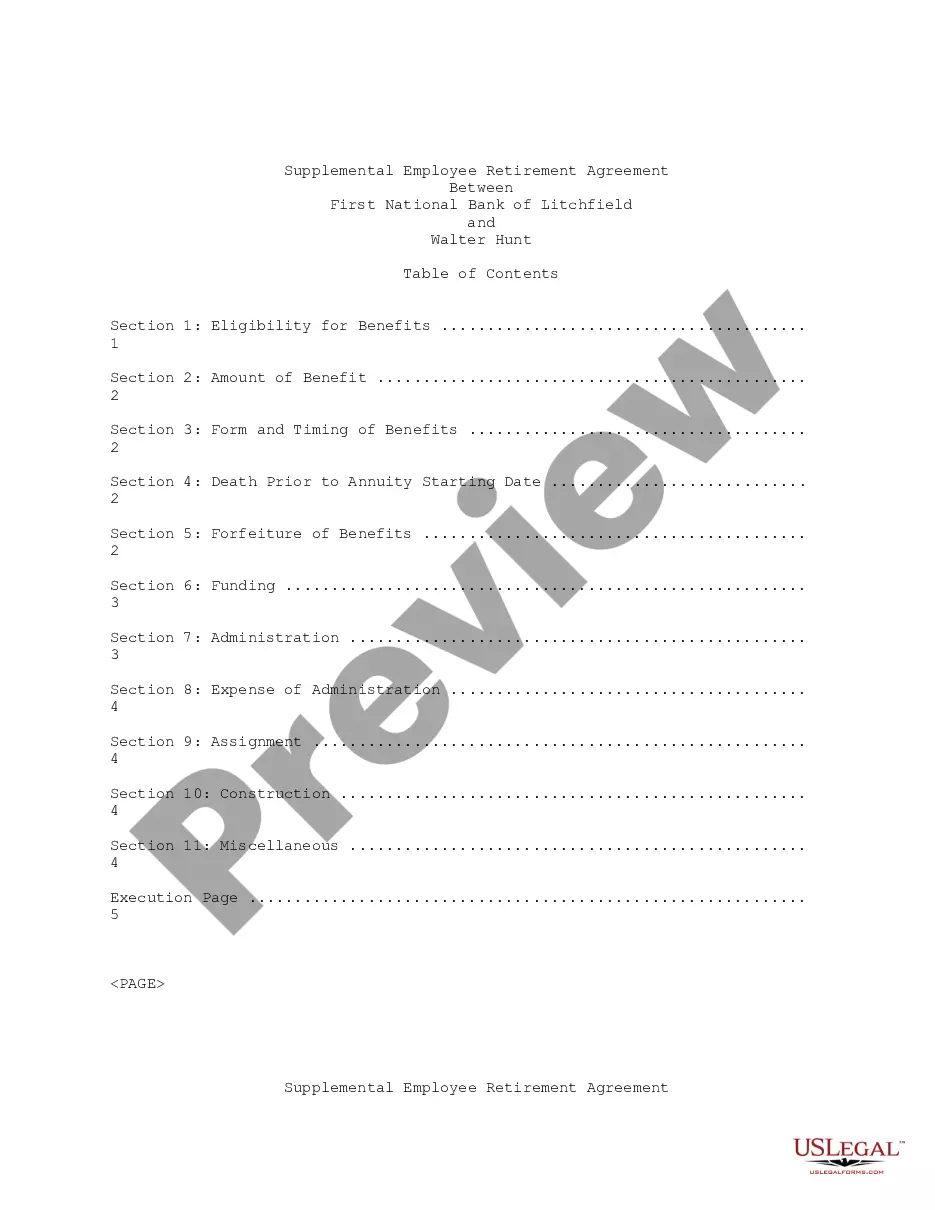

How to fill out Defined-Benefit Pension Plan And Trust Agreement?

It’s obvious that you can’t become a legal professional immediately, nor can you figure out how to quickly prepare Defined Benefit Plan Form Withdrawal Rules without having a specialized background. Creating legal documents is a long venture requiring a certain training and skills. So why not leave the creation of the Defined Benefit Plan Form Withdrawal Rules to the pros?

With US Legal Forms, one of the most extensive legal template libraries, you can find anything from court paperwork to templates for in-office communication. We understand how crucial compliance and adherence to federal and state laws and regulations are. That’s why, on our platform, all templates are location specific and up to date.

Here’s start off with our platform and get the document you need in mere minutes:

- Discover the form you need with the search bar at the top of the page.

- Preview it (if this option provided) and check the supporting description to determine whether Defined Benefit Plan Form Withdrawal Rules is what you’re searching for.

- Start your search again if you need any other template.

- Set up a free account and select a subscription option to purchase the template.

- Choose Buy now. Once the payment is complete, you can download the Defined Benefit Plan Form Withdrawal Rules, fill it out, print it, and send or mail it to the designated individuals or organizations.

You can re-access your documents from the My Forms tab at any time. If you’re an existing client, you can simply log in, and find and download the template from the same tab.

Regardless of the purpose of your paperwork-whether it’s financial and legal, or personal-our platform has you covered. Try US Legal Forms now!

Form popularity

FAQ

A defined benefit plan generally must make RMDs by distributing the participant's entire interest in periodic annuity payments as calculated by the plan's formula for: the participant's life, the joint lives of the participant and beneficiary, or. a "period certain" (see Treas.

In-service withdrawals Generally, a defined benefit plan may not make in-service distributions to a participant before age 59 1/2.

Withdrawing from a DCPP You can't withdraw the money in a DCPP before you retire. The earliest retirement age depends on the plan provisions and is 10 years before the normal retirement age under the plan. If the normal retirement age is 65, the earliest you can retire from the plan is age 55.

Roth IRAs do not require RMDs for the original account owner. Starting in 2024, investors with a Roth 401(k) or Roth 403(b) will also be free from RMDs. Failure to take your RMD triggers a 25% penalty on the amount not distributed.

Defined Benefit Plan Distributions In general, benefits are not paid until the Plan's specified retirement age. This often is age 62 or 65. However, many small Plans allow the participant to "cash out" their benefit, regardless of age, by electing a lump sum distribution in lieu of annual lifetime payments.