Grantor Retained Annuity Trust Withholding

Description

Form popularity

FAQ

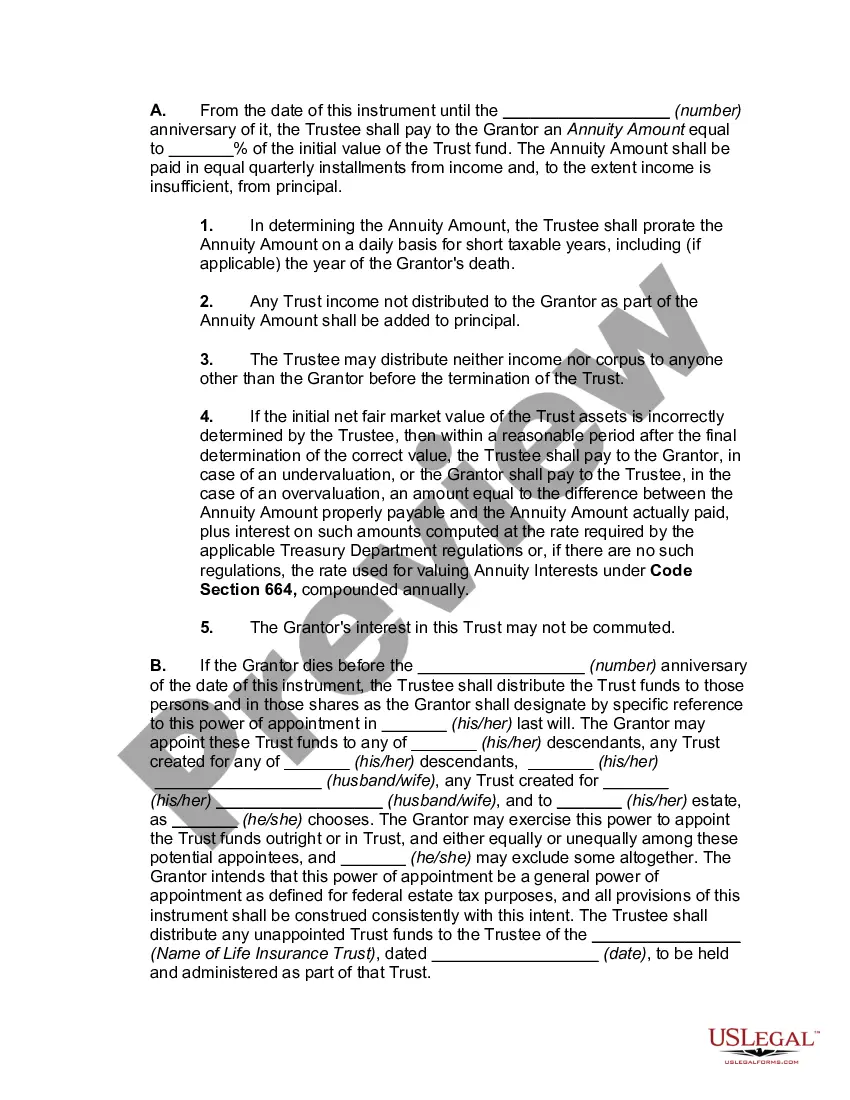

At the end of a GRAT term, the remaining assets in the trust are typically distributed to the beneficiaries without incurring additional gift tax, provided the GRAT adhered to IRS guidelines. This is beneficial as it allows you to transfer wealth while optimizing your tax situation. The grantor may also need to reassess estate plans, considering implications related to grantor retained annuity trust withholding. For assistance in planning and executing these complex steps, turn to USLegalForms for clear, simple solutions.

At the conclusion of the annuity period in a Grantor Retained Annuity Trust (GRAT), the remaining assets are transferred to the beneficiaries as outlined in the trust agreement. This transfer can result in significant tax benefits, especially if the trust has successfully minimized the taxable value of assets during its term. It's crucial to ensure that all requirements regarding grantor retained annuity trust withholding are met. USLegalForms offers guidance to support you through the processes involved when an annuity ends.

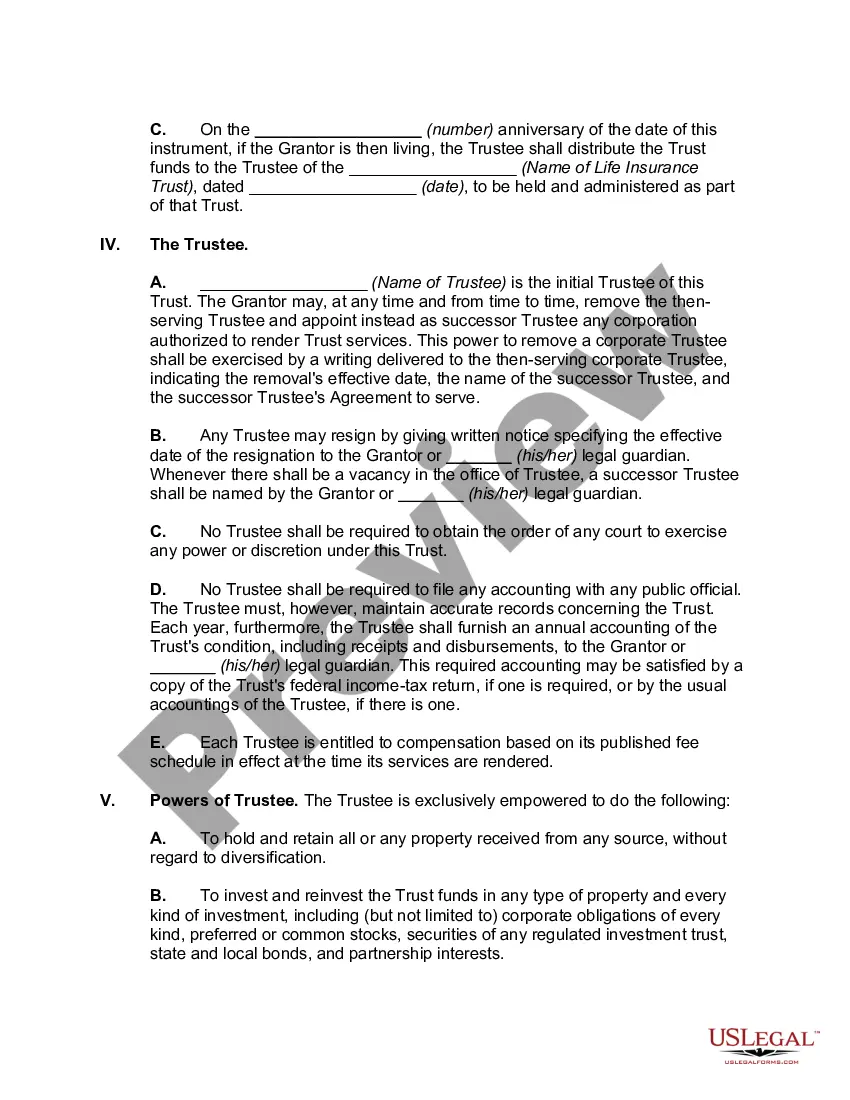

When a Grantor Retained Annuity Trust (GRAT) fails, it does not fulfill its intended purpose of transferring wealth to beneficiaries while minimizing gift taxes. This failure typically occurs if the annuity payments do not meet requirements set by the IRS, causing the trust to lose its tax benefits. Consequently, the assets revert back to the grantor's estate, which can lead to unintended tax implications. To navigate these complexities, consider using USLegalForms, which provides resources and tools to help manage your GRAT effectively.

In a grantor retained annuity trust, the grantor generally pays taxes on income generated by the trust assets. This is because the grantor retains certain control rights, deeming the trust as a grantor trust for tax purposes. Through strategic planning, you can navigate the complexities of grantor retained annuity trust withholding effectively.

Usually, the responsibility for paying taxes on trust income falls to the trust itself or the beneficiaries receiving distributions. If the trust is a grantor trust, the grantor is liable for the income taxes, which includes situations involving grantor retained annuity trust withholding. It's essential to understand how tax obligations are structured in your trust.

A primary difference is that a grantor retained annuity trust allows the grantor to receive annuity payments during the trust term, which is not the case with an irrevocable trust. Once assets are placed in an irrevocable trust, the grantor relinquishes control and cannot make changes. This distinction influences how grantor retained annuity trust withholding is approached.

As mentioned earlier, a grantor retained annuity trust allows the grantor to fund the trust while keeping the right to receive annuity payments for a designated term. Upon completion of this term, remaining assets are transferred to beneficiaries, establishing a way to pass wealth while minimizing taxes. Efficient management of grantor retained annuity trust withholding is key to maximizing benefits.

Typically, the annuitant is responsible for paying taxes on the income generated by the annuity payments. However, it's crucial to note that the grantor can also retain tax obligations, especially if they are considered the owner of the trust for tax purposes. This creates important implications for grantor retained annuity trust withholding.

Yes, a grantor retained annuity trust involves a gift element, which is determined by the value of the annuity payments compared to the assets transferred into the trust. If the value of the assets exceeds the present value of the annuity payments, the excess is treated as a gift. This is an essential aspect to consider regarding grantor retained annuity trust withholding.

One main disadvantage of a GRAT is that if the grantor passes away before the trust term ends, the assets are included in their estate, potentially subjecting it to estate taxes. Additionally, the grantor cannot access the principal amount in the trust once it's established, which may limit financial flexibility. Understanding these factors helps in managing grantor retained annuity trust withholding effectively.