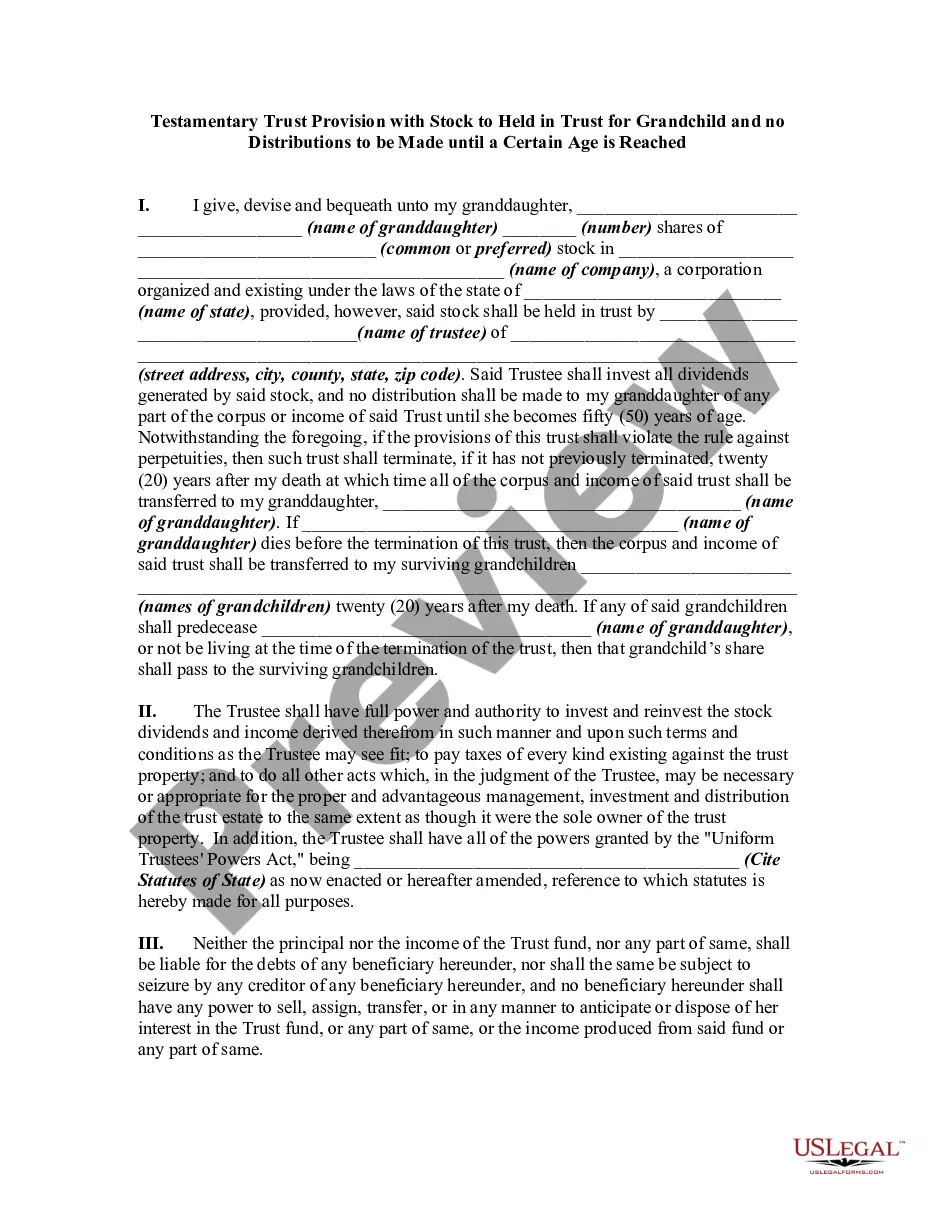

What Is The Testamentary Trust

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Testamentary Trust Provision For The Establishment Of A Trust For A Charitable Institution For The Care And Treatment Of Disabled Children?

- If you’re a returning user, log in to your account to access your templates, making sure your subscription is active. If it’s not, consider renewing it according to your payment plan.

- For first-time users, start by browsing the extensive collection of legal forms. Use the Preview mode to verify that your selected document aligns with your specific needs and local jurisdiction criteria.

- If necessary, search for alternative templates using the Search tab. Confirm that the document you choose meets all required criteria before proceeding.

- Purchase the selected document by clicking the Buy Now button. You will need to create an account to unlock the full range of documents.

- Complete your purchase by entering your payment details, whether through credit card or PayPal for a seamless transaction.

- Download the form directly to your device. You can later access it from the My Forms section in your account.

In conclusion, US Legal Forms offers a vast library, empowering users with over 85,000 forms that are easy to fill and edit. Plus, access to expert assistance ensures every document is completed accurately, saving you time and stress.

Take control of your legal documentation today – explore US Legal Forms to find the testamentary trust you need!

Form popularity

FAQ

Beneficiaries of a testamentary trust are individuals or organizations you designate to receive trust assets after your passing. Typically, these beneficiaries include family members, such as children or spouses, but you can also include charities or friends. The trust terms dictate how and when the beneficiaries receive their assets. By clearly specifying your beneficiaries in the will, you ensure proper management of your estate in line with your wishes.

While a testamentary trust offers several benefits, it also has disadvantages. One major drawback is that it must go through probate, which can delay asset distribution and incur additional costs. Additionally, a testamentary trust does not take effect until your death, limiting immediate asset protection. Being aware of these factors is crucial when deciding if this type of trust is right for you.

To establish a testamentary trust, you first need a valid will that includes provisions for the trust. You should detail the trust's terms, including the trustee's responsibilities and the beneficiaries. Once your will is executed and you pass away, the trust is created automatically. Utilizing a platform like US Legal Forms can simplify the process of drafting your will and trust documents.

A testamentary trust is created through a will and becomes active after the testator passes away. For example, you might set up a testamentary trust to manage your assets for your children's education. This type of trust allows you to specify how and when your assets are distributed, ensuring your wishes are honored. Understanding the specifics of a testamentary trust helps you make informed decisions about your estate.

The key document required for a testamentary trust is a valid will that outlines your estate plan. You must also include detailed descriptions of the assets and a list of beneficiaries. Additionally, you may need financial records and any necessary legal forms to clarify your intentions. Resources like USLegalForms can assist in organizing these documents to facilitate a smooth process.

Yes, a testamentary trust is typically required to file a tax return for any income generated by its assets. This requirement depends on the trust's income level and local tax laws. Since the trust only becomes active after your death, it may be necessary for the appointed trustee to be familiar with tax regulations. Knowing what a testamentary trust involves can prepare you for these obligations.

To establish a testamentary trust, you need a legally valid will that outlines your wishes. This document should detail the assets to be placed in the trust and the responsibilities of the trustee. You may also need additional documents, such as financial statements and beneficiary information, to fully prepare. Using platforms like USLegalForms can help you gather and create these necessary documents efficiently.

Many parents overlook the importance of clearly defining the terms of the trust fund. This can lead to confusion among beneficiaries regarding how and when distributions occur. Another common mistake is failing to choose an appropriate trustee who can manage the trust effectively. By understanding what a testamentary trust entails, you can avoid these pitfalls and ensure your intentions are honored.

Setting up a testamentary trust involves creating a will that outlines your intentions. You specify the terms of the trust within your will and name the trustee who will manage it. After your death, the trust will become active, distributing assets according to your wishes. For guidance through this process, consider using services like USLegalForms to ensure your documents are precise and comprehensive.

While a testamentary trust can provide benefits, it also has drawbacks. One major disadvantage is that it may go through probate, which can delay distribution to beneficiaries. Additionally, the costs to establish and manage the trust can impact the overall value of the estate. Understanding these aspects is important when considering what a testamentary trust can do for your estate planning.