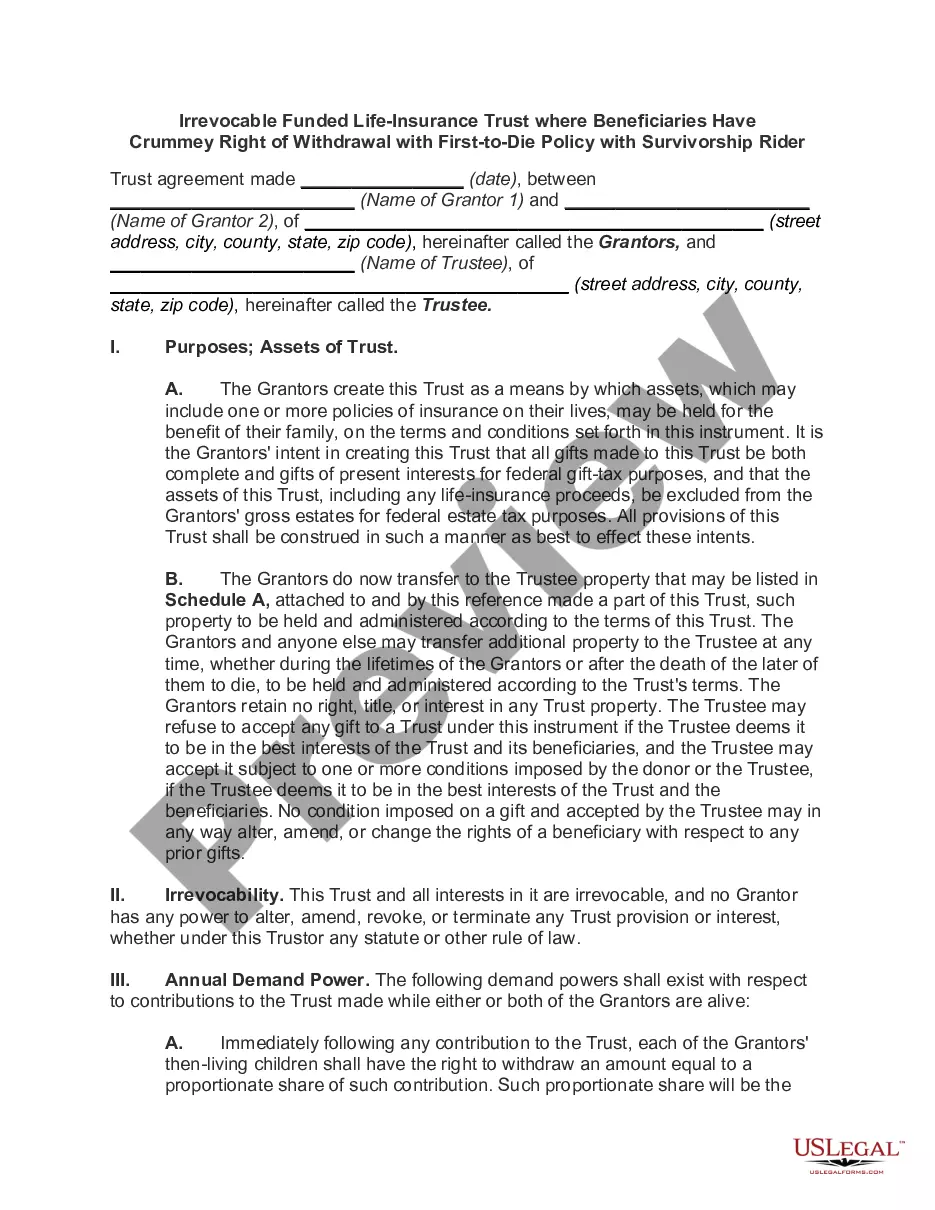

Irrevocable Beneficiary Life Insurance

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Irrevocable Life Insurance Trust - Beneficiaries Have Crummey Right Of Withdrawal?

- Begin by logging into your existing US Legal Forms account to access your downloaded document templates. Verify your subscription's validity and renew if necessary.

- If this is your first time, start by reviewing the document previews and descriptions to ensure you select the appropriate form that aligns with your requirements and local regulations.

- If you need to search for alternative templates, utilize the Search tab at the top to find the exact document you require.

- Once you locate the correct form, click on the Buy Now button and select your preferred subscription plan. You'll need to register for an account to gain access to the extensive resource library.

- Proceed with your payment using your credit card or PayPal, completing the transaction for your chosen subscription.

- Finally, download your form directly to your device, enabling you to complete and access it anytime from the My Forms menu in your profile.

In conclusion, US Legal Forms not only simplifies the document acquisition process but also ensures that individuals and lawyers have access to a vast array of meticulously crafted legal forms. Take charge of your legal documentation today for peace of mind.

Visit US Legal Forms now to explore your options and safeguard your future!

Form popularity

FAQ

The 3 year rule operates primarily within estate planning frameworks. It requires that any transfers made within three years of an individual’s death be considered part of their estate for tax purposes. This means that to avoid additional taxes on life insurance proceeds, it’s crucial to plan ahead and understand how irrevocable beneficiary life insurance fits into your overall strategy. Engaging with knowledgeable platforms like uslegalforms can assist you in navigating these complex rules.

While an irrevocable insurance trust can be beneficial, it also comes with drawbacks. Once established, you cannot change or revoke the trust without following specific legal protocols, which may require beneficiary consent. Additionally, if you need to access funds or change the trust's terms, it can be complicated. Understanding these potential disadvantages will help you make an informed decision regarding irrevocable beneficiary life insurance.

The 3 year rule for irrevocable trusts is similar to that of life insurance. It states that if you transfer assets into an irrevocable trust, they may be included in your estate if you die within three years of the transfer. This rule emphasizes the importance of effective estate planning, particularly when setting up irrevocable beneficiary life insurance within a trust structure. By adhering to this timeline, you can help manage your estate for your beneficiaries effectively.

The 3 year look back rule refers to a period during which life insurance policies can be evaluated for estate tax purposes. If a policyholder transfers ownership of their life insurance policy within three years of their death, the policy may still be included in their taxable estate. Thus, it is important to understand this rule when planning your estate and considering irrevocable beneficiary life insurance options. Planning with awareness of this timeline can help ensure your wishes are honored.

Designating an irrevocable beneficiary for life insurance has significant effects. Once you name someone as an irrevocable beneficiary, you cannot change this designation without their consent. This means that the beneficiary has guaranteed rights to the policy's proceeds, ensuring they receive the benefits regardless of changes in your circumstances. Understanding these effects is crucial when considering irrevocable beneficiary life insurance.

An irrevocable beneficiary has the right to receive policy benefits upon the insured's death, and they must give consent for any changes to the policy. This rights structure allows the irrevocable beneficiary to feel secure in their entitlements, protecting their interest in the policy. If you’re considering making someone an irrevocable beneficiary, ensure their rights align with your intentions.

An irrevocable beneficiary on a life insurance policy is an individual or entity designated to receive benefits that cannot be changed without their approval. This decision provides a stable financial safety net for the beneficiary, ensuring their entitlements are protected. Understanding this can help you navigate your life insurance choices effectively.

The primary difference lies in the ability to change the designation. A revocable beneficiary can be altered by the policyholder at any time, while an irrevocable beneficiary requires their consent for any changes. This difference significantly influences future financial planning and the assurance level for the beneficiaries.

A revocable beneficiary can be changed at the discretion of the policyholder, unlike a regular beneficiary who simply receives benefits upon death. The term 'beneficiary' encompasses anyone designated to receive benefits, while 'revocable beneficiary' specifically refers to those who can be easily removed or replaced. So, all revocable beneficiaries are beneficiaries, but not all beneficiaries are revocable.

A beneficiary can be changed at any time by the policyholder, while an irrevocable beneficiary cannot be altered without their agreement. This distinction provides assurance to the irrevocable beneficiary regarding their future claim to the life insurance benefit. It’s crucial to understand this difference when you choose your beneficiary.