Equipment Lease Leasing With Negative Equity

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

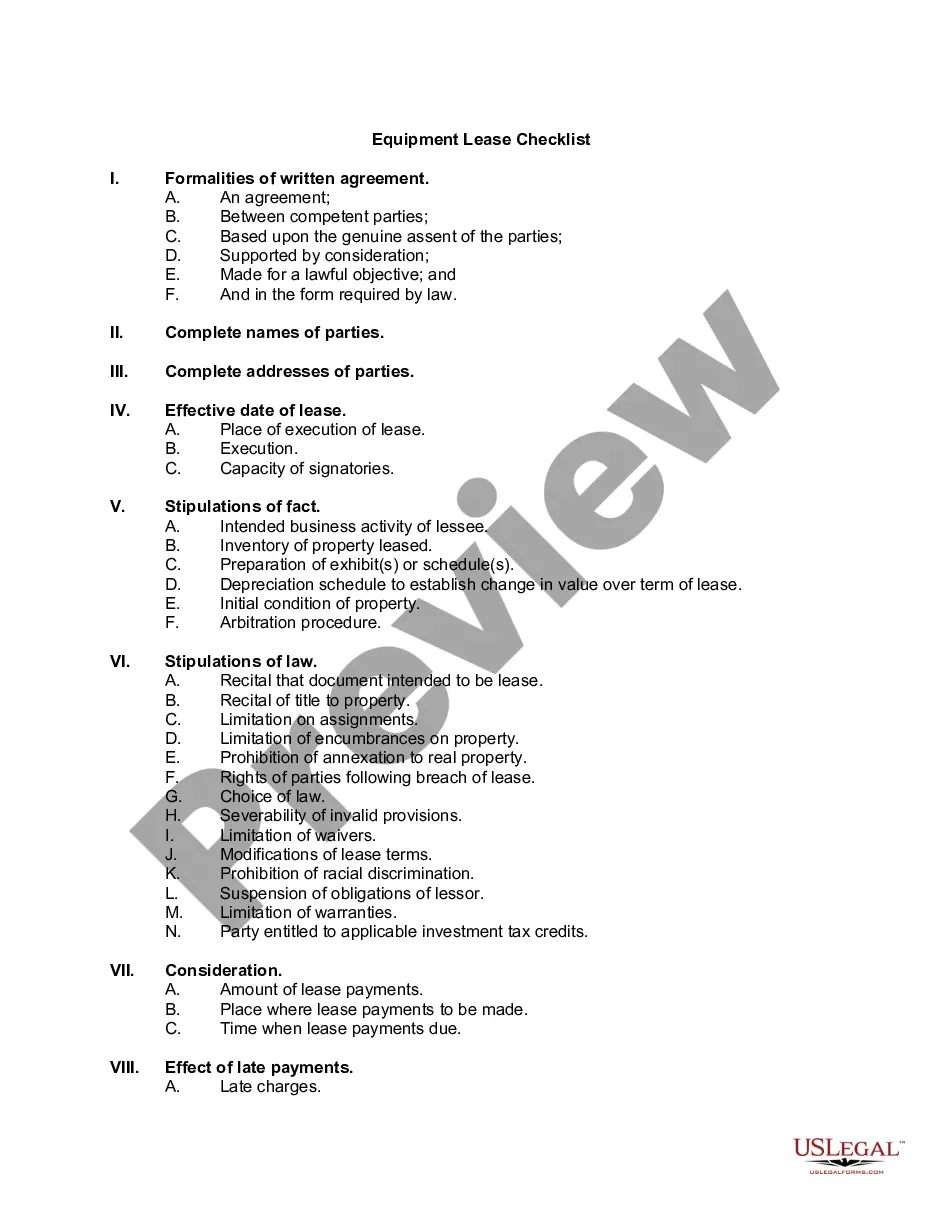

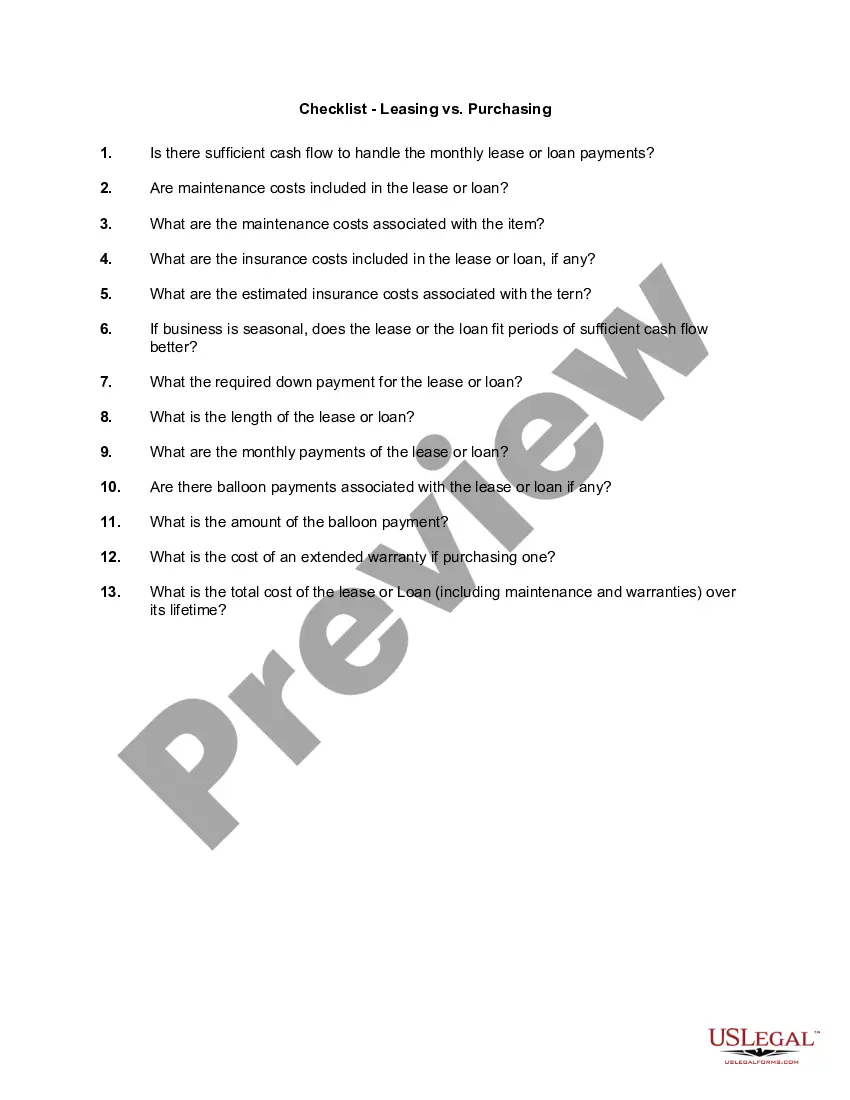

How to fill out Checklist - Leasing Vs. Purchasing Equipment?

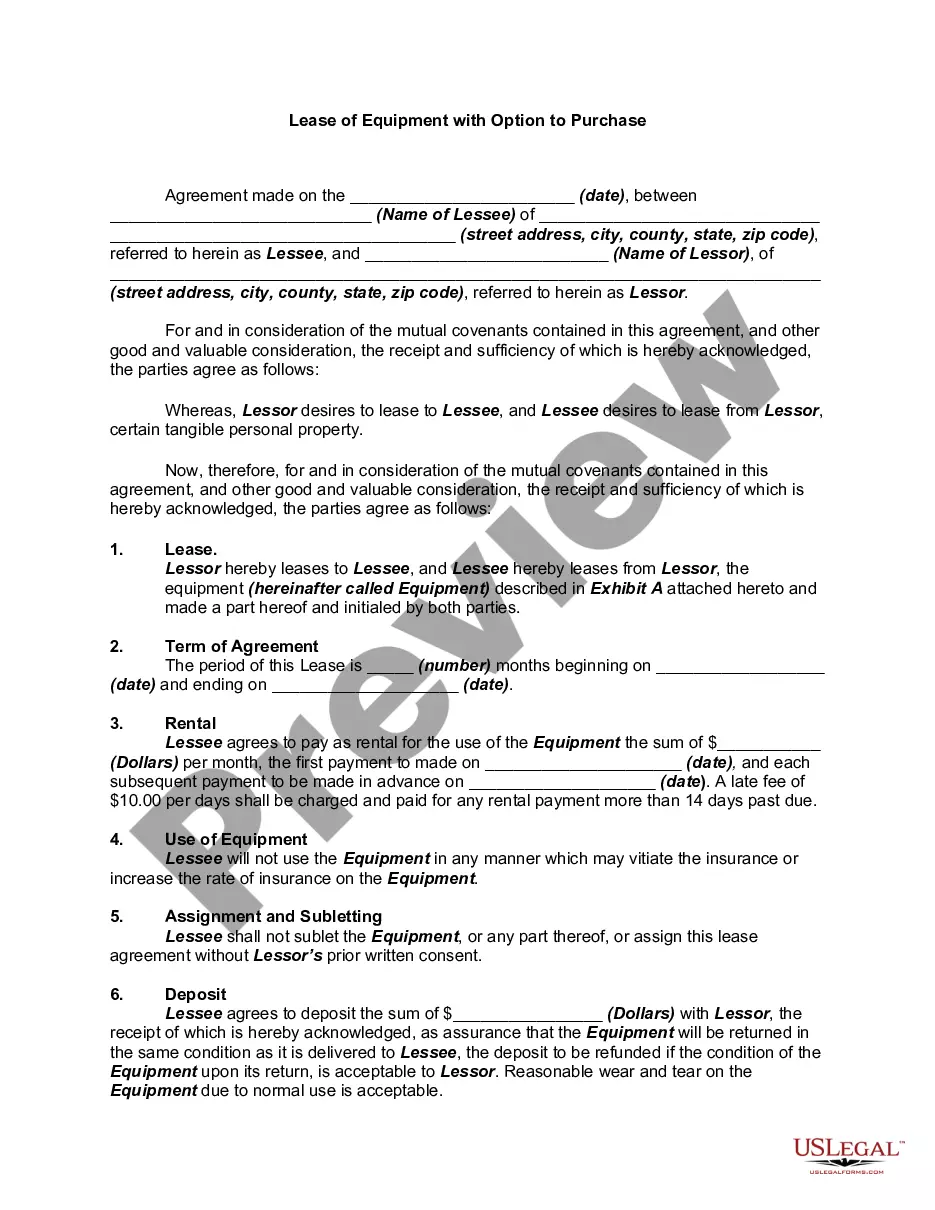

The Equipment Lease Agreement with Negative Equity presented on this page is a versatile formal template created by expert attorneys in accordance with federal and state regulations.

For over 25 years, US Legal Forms has offered individuals, companies, and legal practitioners more than 85,000 validated, state-specific documents for any business and personal situation. It’s the fastest, most straightforward, and most reliable method to acquire the documents you require, as the service ensures the utmost level of data security and anti-virus protection.

Subscribe to US Legal Forms to have authenticated legal templates for all of life's situations readily available.

- Search for the document you require and examine it.

- Choose the pricing plan that works for you and set up an account.

- Select the format you prefer for your Equipment Lease Agreement with Negative Equity (PDF, Word, RTF) and download the document to your device.

- Print the template to fill it out manually or utilize an online multifunctional PDF editor to swiftly and accurately complete and sign your form with an electronic signature.

- Access the same document again whenever necessary.

Form popularity

FAQ

A lease will be recorded on the balance sheet as a right-of-use (ROU) asset and lease liability. The lease liability is the payment obligation over the term of the lease contract, while the ROU asset represents the control of the asset under the lease contract.

If you lease your equipment instead of purchasing it, you can't depreciate the equipment. However, you will generally be able to deduct the lease payments you make, at the time that you make them, which can result in a larger tax benefit than you'd get if you bought the equipment outright.

The equipment account in the balance sheet is debited by the present value of the minimum lease payments, and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year.

The lessor reports the lease as a leased asset on the balance sheet and individual lease payments as income on the income and cash flow statements. The lessee reports the lease as both an asset and a liability on the balance sheet due to their stake as a potential owner of the asset and their required payment.