Promissory Notes For Sale With Interest

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Promissory Note In Connection With A Sale And Purchase Of A Mobile Home?

Utilizing legal document examples that comply with federal and local regulations is essential, and the internet provides numerous choices.

However, why squander time hunting for the appropriate Promissory Notes For Sale With Interest template online when the US Legal Forms digital library already consolidates such documents in one location.

US Legal Forms is the largest online legal repository featuring over 85,000 fillable templates crafted by attorneys for any professional and personal circumstance.

Review the template using the Preview function or through the text outline to ensure it fulfills your needs.

- They are user-friendly with all documents categorized by state and intended use.

- Our specialists stay updated with legal changes, ensuring your documents are current and compliant when acquiring a Promissory Notes For Sale With Interest from our site.

- Acquiring a Promissory Notes For Sale With Interest is straightforward and quick for both existing and new users.

- If you already have an account with an active subscription, Log In and download the template you need in the preferred format.

- If you are new to our site, follow the steps outlined below.

Form popularity

FAQ

When you record interest on a promissory note, you must calculate the interest based on the agreed-upon rate and the outstanding balance. You can create a simple journal entry that reflects the interest expense and increases your liability. For example, if you issue promissory notes for sale with interest, ensure you maintain clear documentation for accurate accounting.

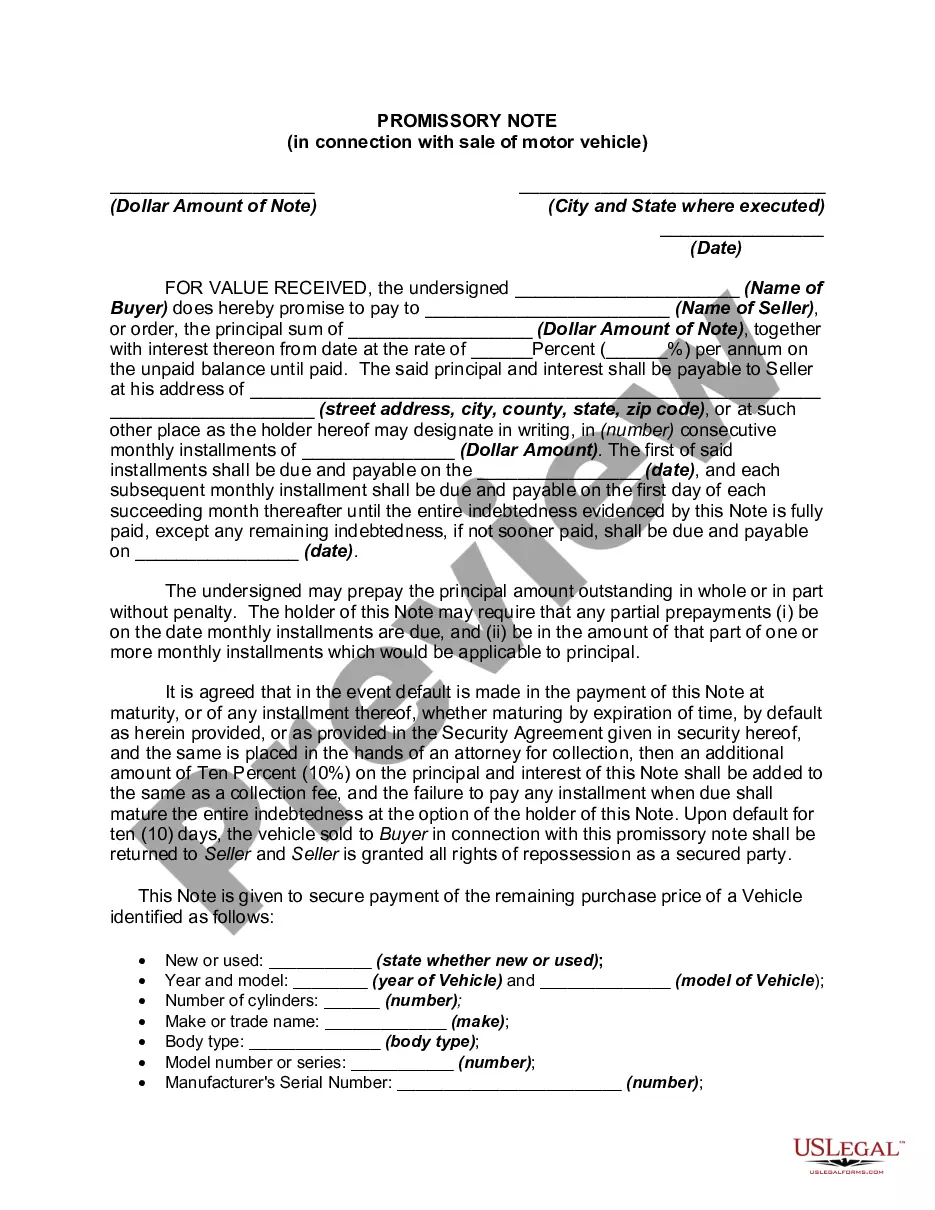

A promissory note is a financial and legal instrument through which one party agrees (or promises) to pay another party a sum of money that's comprised of two pieces: principal and interest.

Interest rate: A promissory note typically includes the amount of interest that a borrower will agree to pay the lender as a fee for granting them the loan. Interest may be charged as an incremental fixed rate percentage of the unpaid balance of the loan, or a variable rate that changes with time.

Next, calculate the interest charge for one year by multiplying the principal by the interest rate. In our example that math would yield $5,000 X 0.07 = $350. This is the annual interest charge for the note.

The borrower records the note by debiting the cash account and crediting the notes payable account. The rest of the notes payable formula includes that interest due to date is accrued at the end of each financial period by debiting the interest expense account and crediting the interest payable liability account.

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.