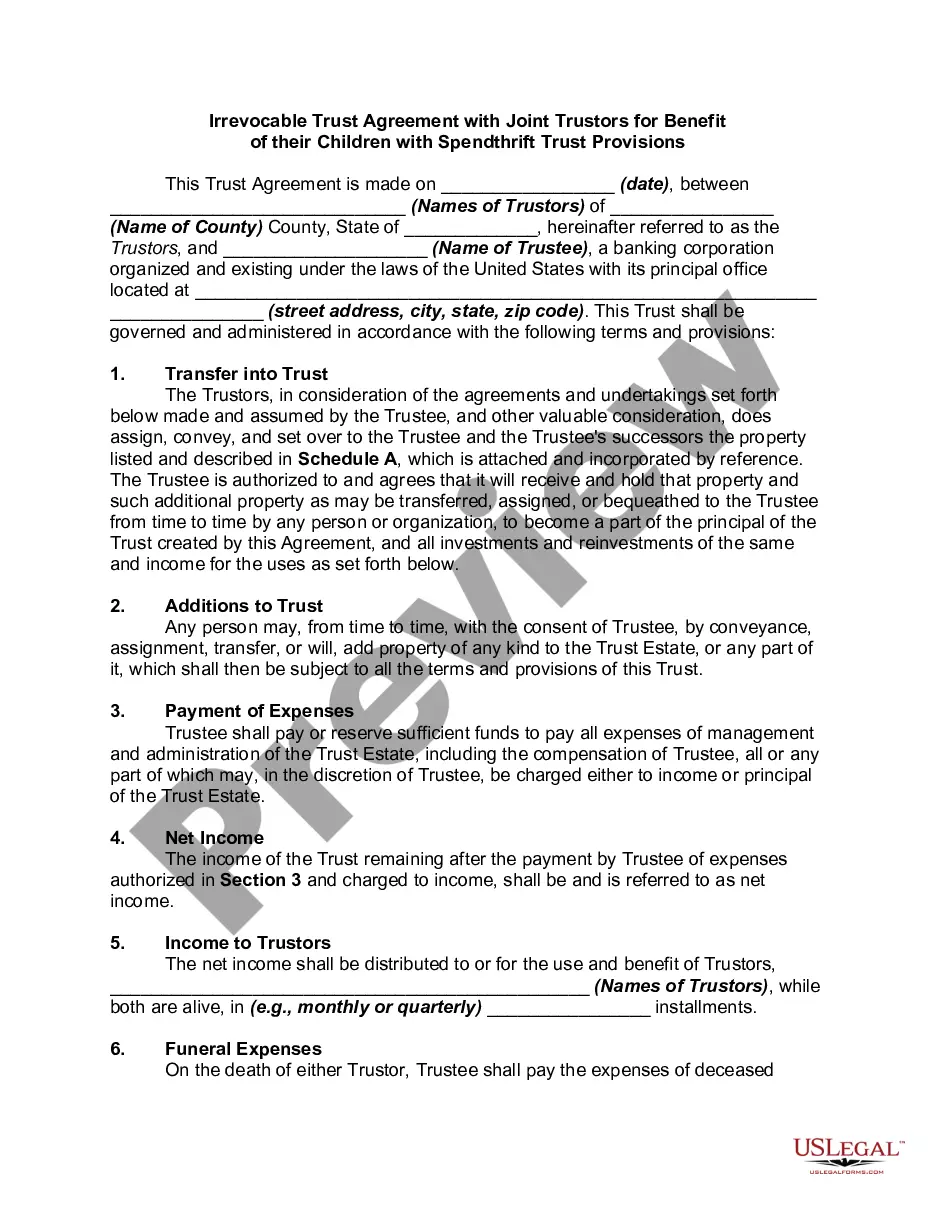

Irrevocable Spendthrift Trust Form With Irs Code 643

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Irrevocable Trust Agreement For Benefit Of Trustor's Children And Grandchildren With Spendthrift Trust Provisions?

Managing legal documentation and procedures can be a labor-intensive addition to your day.

Irrevocable Spendthrift Trust Form With Irs Code 643 and similar documents typically necessitate that you seek them out and comprehend how to fill them out proficiently.

Thus, if you are addressing financial, legal, or personal matters, having an extensive and user-friendly online directory of forms readily accessible will greatly assist you.

US Legal Forms is the premier online source of legal templates, showcasing over 85,000 state-specific forms and a variety of resources to help you complete your documents effortlessly.

Simply Log In to your account, locate Irrevocable Spendthrift Trust Form With Irs Code 643, and retrieve it instantly from the My documents section. You can also access forms you have saved previously.

- Explore the array of relevant documents accessible with just one click.

- US Legal Forms offers state- and county-specific forms available for download at any time.

- Secure your document management processes by utilizing a superior service that enables you to prepare any form in just a few minutes without any extra or concealed charges.

Form popularity

FAQ

Items of gross income constituting extraordinary dividends or taxable stock dividends which the fiduciary, acting in good faith, determines to be allocable to corpus under the terms of the governing instrument and applicable local law shall not be considered income.

Gains from the sale or exchange of capital assets shall be excluded to the extent that such gains are allocated to corpus and are not (A) paid, credited, or required to be distributed to any beneficiary during the taxable year, or (B) paid, permanently set aside, or to be used for the purposes specified in section 642( ...

IRS Form for Irrevocable Trust The legal name of the trust, the Trustee name and address must be given to the IRS. Next, the Trustee should file the Form 1041 ? ?U.S. Income Tax Return for Estates and Trusts? with the IRS ? if the Irrevocable Trust has more than $600 in taxable income generated annually.

2 ? changes that. Unless the assets are included in the taxable estate of the original owner (or "grantor"), the basis doesn't reset. To get the stepup in basis, the assets in the irrevocable trust now must be included in the taxable estate at the time of the grantor's death.

Two or more trusts will be treated as one trust if they have substantially the same grantor(s) and substantially the same primary beneficiary(ies), and if their principal purpose is tax avoidance (IRC § 643(f)). For purposes of the multiple trust rules, a married couple is treated as one person.