Mortgage Loan Form Template For Child

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

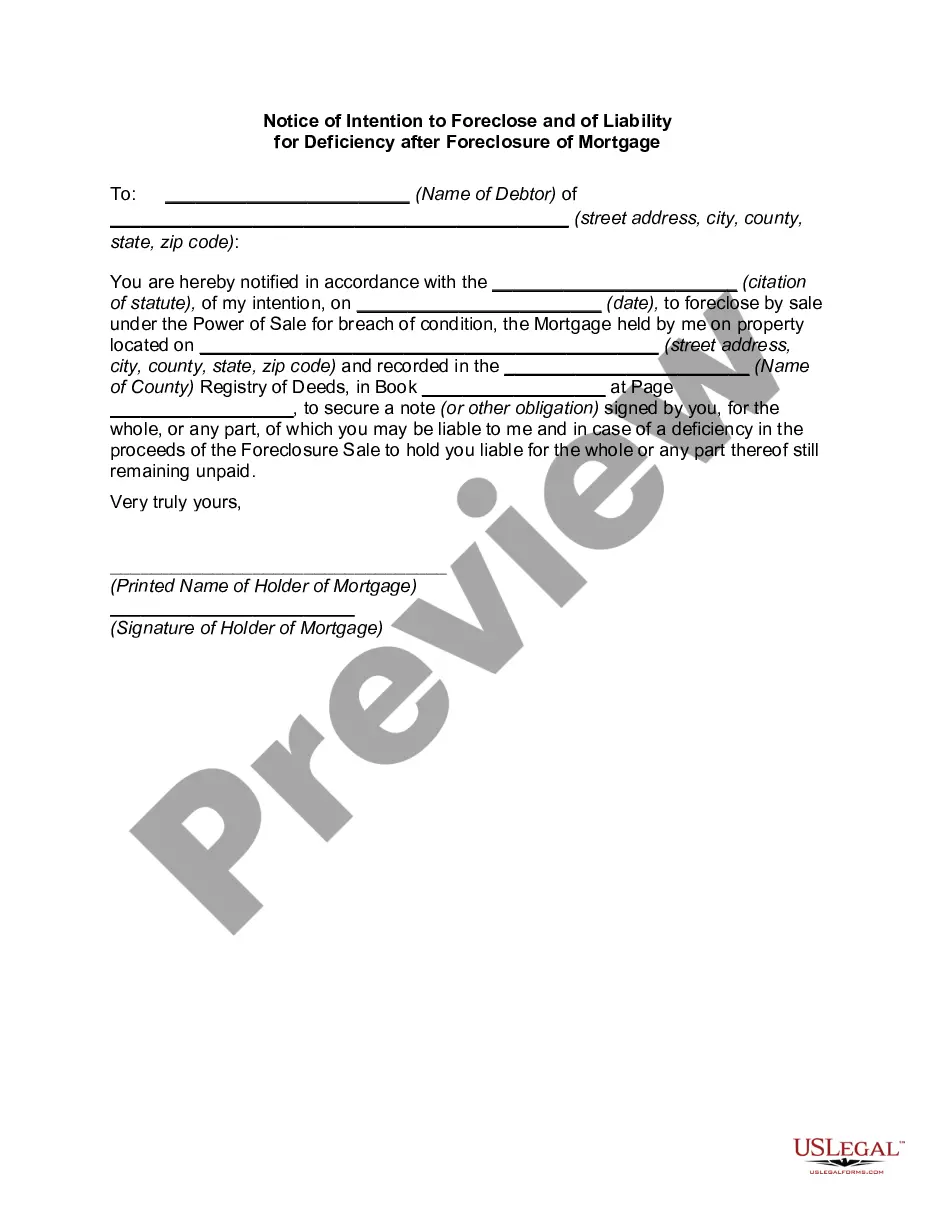

How to fill out Notice Of Intent To Foreclose - Mortgage Loan Default?

Creating legal documents from the ground up can often be overwhelming.

Certain situations may require extensive research and significant financial investment.

If you’re seeking a simpler and more cost-effective method of producing a Mortgage Loan Form Template For Child or any other documents without unnecessary hurdles, US Legal Forms is always available for you.

Our digital collection of over 85,000 current legal documents encompasses nearly every aspect of your financial, legal, and personal needs. With just a few clicks, you can swiftly access state- and county-specific forms meticulously prepared by our legal experts.

Examine the document preview and details to confirm that you have located the form you require. Ensure that the form you select adheres to the laws and regulations of your state and county. Select the appropriate subscription option to purchase the Mortgage Loan Form Template For Child. Download the form, then fill it out, sign, and print it. US Legal Forms has a strong reputation and over 25 years of expertise. Join us today and simplify the process of form completion!

- Utilize our platform whenever you require dependable and trustworthy services where you can efficiently find and obtain the Mortgage Loan Form Template For Child.

- If you’re already familiar with our offerings and have set up an account, simply Log In, select the form, and download it instantly or re-download it at any time later in the My documents section.

- Not yet registered? No problem. It takes minimal time to establish and navigate the library.

- Before proceeding to download the Mortgage Loan Form Template For Child, consider these recommendations.

Form popularity

FAQ

The 3 7 3 rule in mortgage means that your lender must provide you with a Loan Estimate within three business days of receiving your application. Then, they must give you a Closing Disclosure three days before you finalize your loan. This rule aims to ensure that you have enough time to review your mortgage loan form template for child and make informed decisions before proceeding. This clarity helps you avoid surprises and plan your finances better.

To be thorough, a promissory note should include a core group of details: Total amount of money being loaned. Date of the loan. How the loan was delivered (cash, check, direct deposit) The name and address of the person loaning the money. The name and address of the person borrowing the money.

For small loans under $10,000, the answer is simple ? no. The IRS isn't concerned with most personal loans to your son, daughter, stepchild, or other immediate family member. They also don't care how often loans are handed out, whether interest is charged, or if you get paid back.

The $100,000 De Minimis Exception If the total sum of lending is less than $100,000, the IRS allows you to charge interest based on the lesser of either the AFR rate or the borrower's net investment income for the year. If their investment income was $1,000 or less, the IRS allows them to charge no interest.

What should be in a personal loan contract? Names and addresses of the lender and the borrower. Information about the loan co-borrower or cosigner, if it's a joint personal loan. Loan amount and the method for disbursement (lump sum, installments, etc.) Date the loan was provided. Expected repayment date.

How to make a family loan agreement The amount borrowed and how it will be used. Repayment terms, including payment amounts, frequency and when the loan will be repaid in full. The loan's interest rate. ... If the loan can be repaid early without penalty, and how much interest will be saved by early repayment.