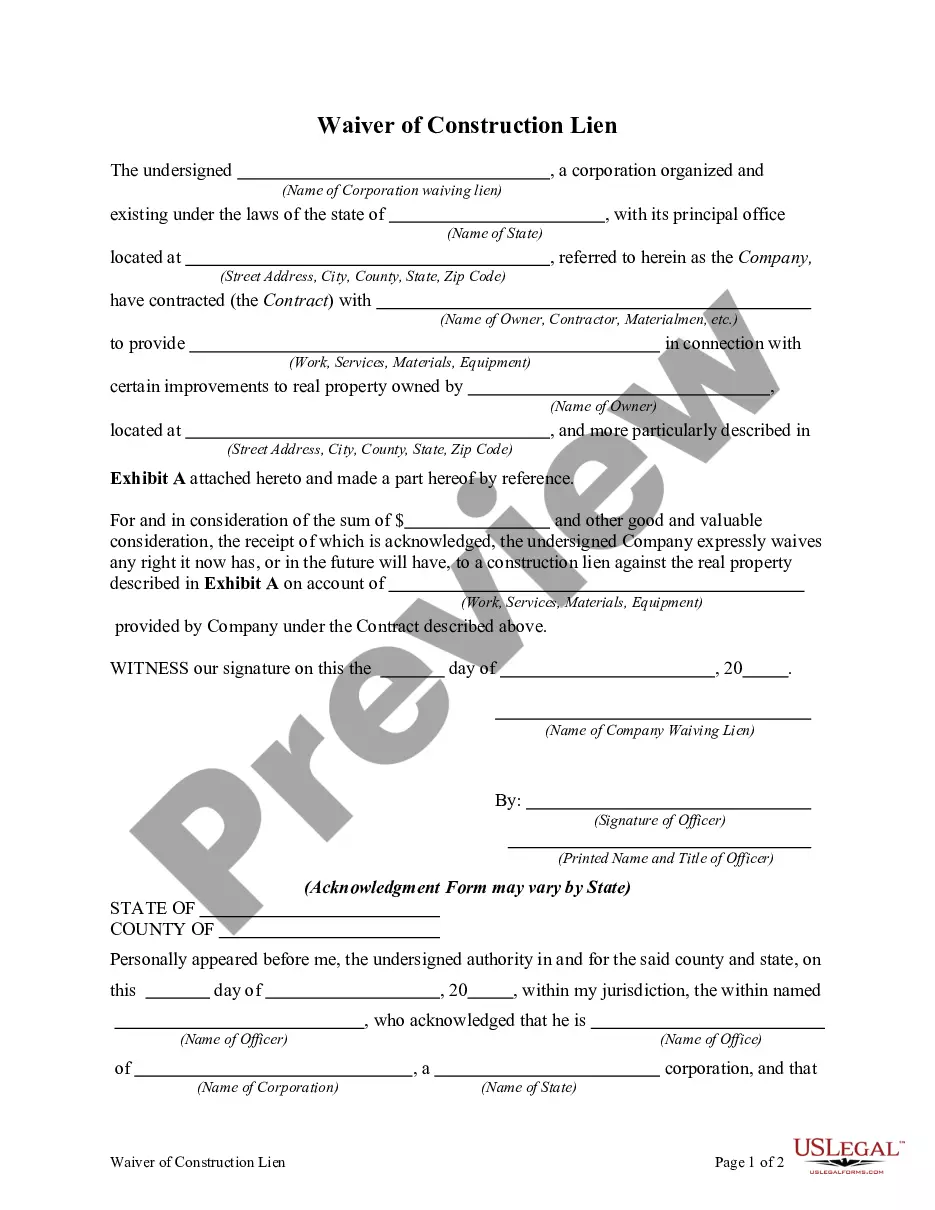

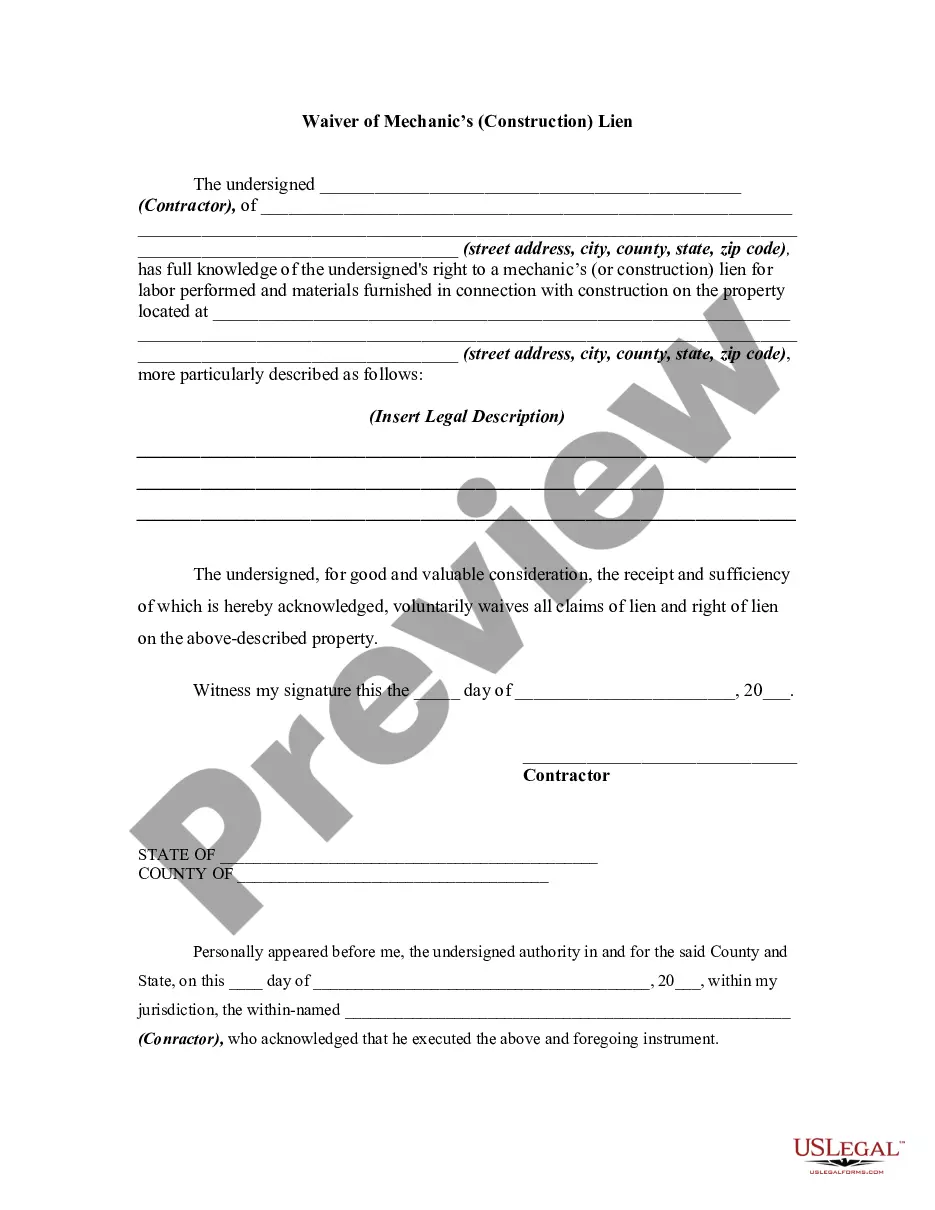

Sba Release Of Lien Without Contract

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Waiver And Release Of Lien By Contractor?

It’s no secret that you can’t become a legal expert immediately, nor can you grasp how to quickly prepare Sba Release Of Lien Without Contract without having a specialized background. Putting together legal forms is a time-consuming venture requiring a specific education and skills. So why not leave the creation of the Sba Release Of Lien Without Contract to the professionals?

With US Legal Forms, one of the most extensive legal template libraries, you can find anything from court documents to templates for internal corporate communication. We understand how crucial compliance and adherence to federal and state laws and regulations are. That’s why, on our website, all forms are location specific and up to date.

Here’s start off with our website and obtain the form you need in mere minutes:

- Find the form you need with the search bar at the top of the page.

- Preview it (if this option provided) and check the supporting description to determine whether Sba Release Of Lien Without Contract is what you’re looking for.

- Start your search again if you need any other template.

- Register for a free account and select a subscription plan to buy the template.

- Pick Buy now. As soon as the payment is through, you can get the Sba Release Of Lien Without Contract, complete it, print it, and send or send it by post to the designated people or organizations.

You can re-gain access to your documents from the My Forms tab at any time. If you’re an existing client, you can simply log in, and find and download the template from the same tab.

No matter the purpose of your paperwork-be it financial and legal, or personal-our website has you covered. Try US Legal Forms now!

Form popularity

FAQ

Smaller loans like this don't require collateral or a personal guarantee, which means there's not much the SBA can do if a business closes. The government may seize federally held assets like income tax refunds, but they will not be able to seize your personal funds or assets owned by the business.

You'll need to submit an offer in compromise to the SBA and provide evidence that you are unable to repay your loan. The offer you submit must be something you can reasonably repay and usually as a lump sum. Both your lender and the SBA must agree to the offer in compromise.

The SBA will be willing to release the mortgage/lien so that the owner can be allowed to sell or refinance the property under the proper circumstances. However, cooperation is required. Commitment on the borrower's behalf is also necessary. The borrower must not receive any of the sales or refinance consideration.

GENERAL REQUIREMENTS (For All Loan Types): A detailed letter from the borrower(s) and/or guarantors (if any) signed and dated explaining the reasons for requesting that SBA release its lien on collateral. Explain why the SBA is not to be paid in full as a result of this transaction.

If you closed your business and have outstanding debt on a loan through the EIDL program of less than $25,000, there is little (if anything) the SBA can do to recover what you owe. Bankruptcy likely will not be necessary, but you should speak with a lawyer.